Anyone involved in buying or trading cerium metal knows that trying to analyze the Western rare earth market without deeply dissecting China’s domestic landscape is like trying to check the weather by looking at the floor.

Because China controls the overwhelming majority of the world’s rare earth mining and separation capacity, the week-by-week price movements inside major Chinese industrial hubs immediately dictate the operational boundaries for European warehouse ports in Rotterdam and trading desks in Busan.

After a highly volatile run in late May followed by extended periods of dead silence, the Chinese domestic market has shown its true underlying resilience.

But before brushing this off as standard seasonal noise, remember the big picture: industrial manufacturing simply cannot produce automotive catalytic converters, precision optical glass, or advanced metallurgical alloys without cerium. The underlying global need for this metal remains rock solid.

With Chinese domestic prices stubbornly holding a firm line despite localized buying standoffs, international procurement teams are receiving a clear signal: the recent price freezes are not a sign of a weak market, but a strategic standoff where suppliers hold the winning cards. Here is how local Chinese data from Graph and global supply bottlenecks are clashing to drive the market right now.

China’s Rare Earth Supply Structure Supports Cerium Prices

To understand where the global market is headed, we must look directly at the week-by-week trend of the Chinese domestic market. For much of June, downstream Chinese factories tried to force raw material prices down by executing a prolonged “buyers’ strike”burning through their stored warehouse inventory rather than buying new metal.

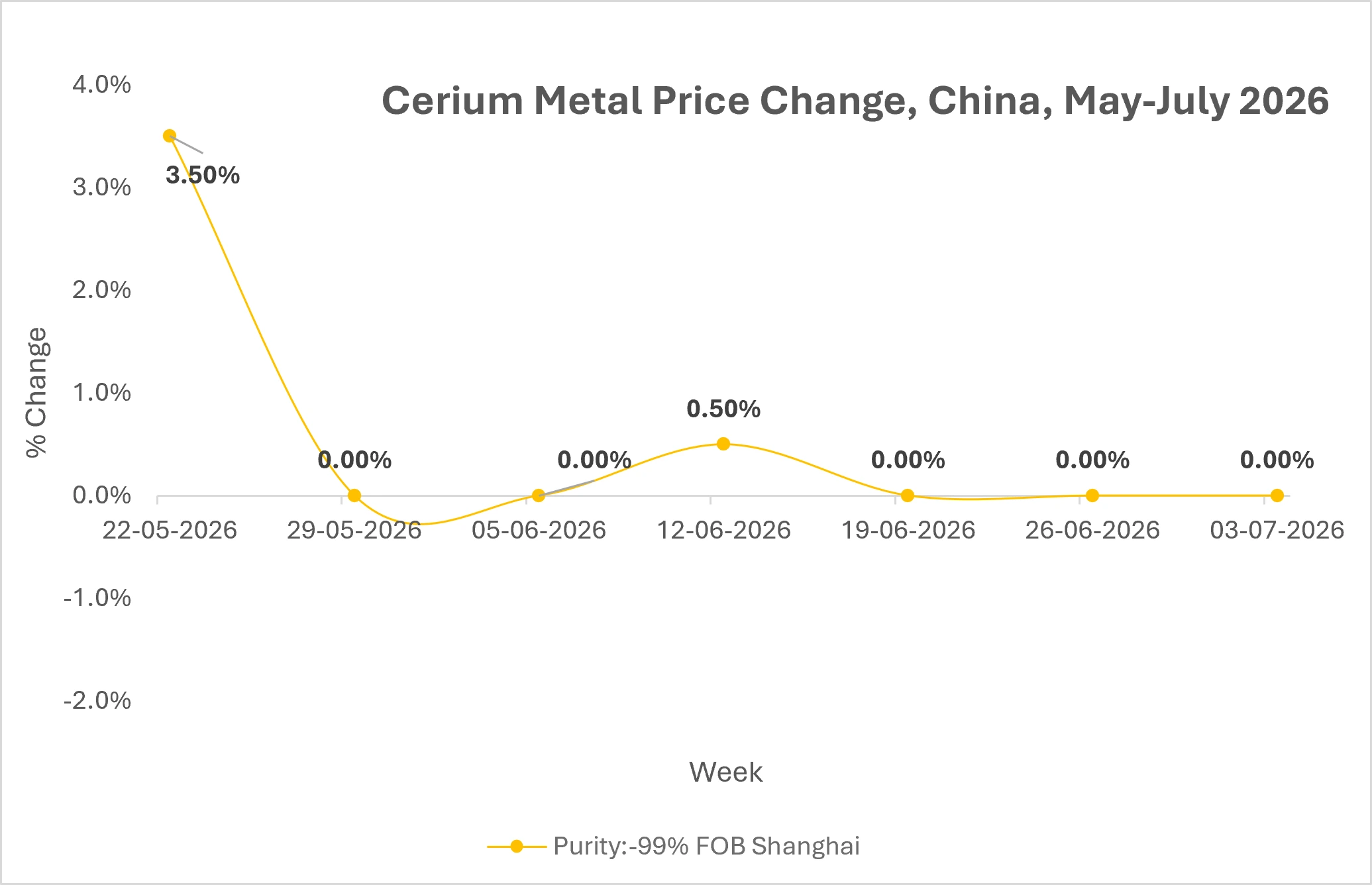

Look at the exact week-by-week performance of the Chinese domestic market trend shown in

Source: Price Watch™ Cerium Metal

After sitting completely frozen at a 0% change for two straight weeks following the initial 3.50% spike, the Chinese domestic market snapped back to life mid-month with a 0.50% jump, pushing local tender prices upward.

Even though the market settled into another 0% flatline for three consecutive weeks leading into early July, these readings serve as a massive wake-up call for the rest of the world.

It proves that major Chinese factories are hitting the absolute bottom of their storage piles.

Facing steady production schedules, they have periodically had to rush back into the market and issue fresh buy orders. Because upstream Chinese suppliers defended their price floor during the freeze, the factories had zero leverage to demand a discount; they simply had to pay the asking price.

Inside the Chinese Supply Architecture

While the sudden domestic buying spurts provided the spark, the structural issues keeping global prices propped up are happening across China’s tightly managed supply chains. Downstream mills tried to starve suppliers out by pausing their orders, but the domestic suppliers held the ultimate trump card:

- Strict Government Mining Quotas: Unlike base metals, Chinese rare earth production operates under strict state-mandated mining and separation quotas. Upstream producers cannot simply overproduce to chase short-term volume, which completely eliminates the risk of surplus inventory leaking onto the market.

- Elevated Production Costs: Domestic processing and environmental compliance costs inside China remain exceptionally high. Suppliers watched the flatline weeks in graph without panicking because they knew replacement costs for raw cerium oxide were too high to justify discounting.

- The Domestic High-Tech Floor: China’s own consumption of high-grade rare earths for clean energy infrastructure, electric vehicle catalysts, and precision smartphone glass optics is putting a hard floor under demand, independent of Western purchasing trends.

The Bottom Line for the Global Industry

For international procurement teams, the latest data from graph combined with tight Chinese supply control provides a clear reality check: the price floor was tested repeatedly, and it held.

This is a market running on exceptionally disciplined raw materials. Buyers tried to wait the market out, but the physical reality of the Chinese concentrate shortage gave the suppliers the winning hand.

Cerium Market Outlook

Looking ahead, expect global cerium metal prices anchored heavily by domestic Chinese tenders to remain strong with a clear defensive posture against price drops. We are not going to see prices retreat to old lows because the baseline demand from heavy industrial technology is just too powerful.

Downstream buyers who spent June sitting on their hands hoping the consecutive 0.00% flatlines in China would turn into a massive global price drop will have to rethink their procurement budgets. Upstream raw material suppliers are entering July feeling very confident, fully aware that fresh ore is hard to come by anywhere in the world.

If major factories keep issuing large bulk tenders over the coming weeks to restock their empty warehouses, the firm baseline established during these flatline weeks could easily ignite a wider, global summer rally. For the immediate future, industrial buyers everywhere should prepare for a firm, stubborn market where price dips are exceptionally rare and fiercely defended.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.