The US polypropylene market has entered a period of sharp price decompression. The aggressive US PP price trend reversals seen across May and June 2026 mark the unwinding of the Q1 geopolitical inflationary cycle.

What began as a conflict-induced surge in energy and monomer costs has transformed into a rapid market correction, resetting polypropylene prices in USA hubs.

The Backstory: From West Asia Panic to Crude Oil Collapse

During Q1 2026, severe cost-push inflation gripped the North American petrochemical sector. Escales in West Asia and fears of a Strait of Hormuz blockade triggered a panic-buying frenzy, pushing North American propylene prices up.

As regional tensions eased in late May, the energy market sharply inverted:

- Brent Crude and WTI: Plummeted by more than $40 per barrel from their spring peaks, retreating into the low-$80s.

- Feedstocks: Naphtha and Natural Gas Liquids (NGLs) shed their speculative premiums; spot propane dropped.

This collapse eliminated the primary cost support sustaining elevated polypropylene prices in USA markets.

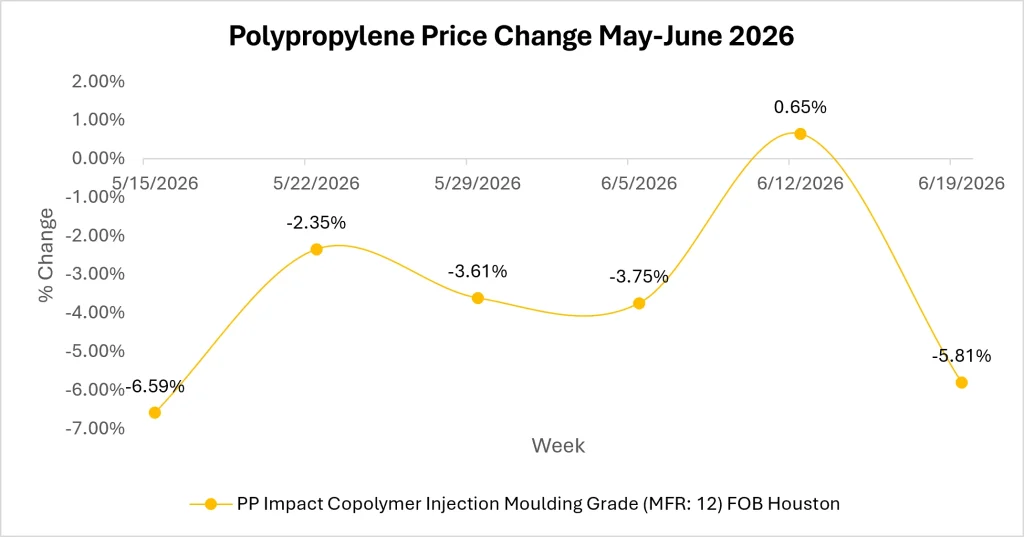

Source: Price Watch™ Polypropylene Prices

The June 12 False Bottom (+0.65%)

During the week ending June 12, prices temporarily recovered by 0.65%.

This brief rebound was not driven by fundamentals but rather by:

- A short-lived increase in export container bookings to Latin America.

- Early-season hurricane hedging by Gulf Coast traders.

- Tactical restocking by select buyers.

The recovery proved temporary as underlying market fundamentals remained bearish.

The June 19 Cliff (-5.81%)

The temporary rebound was completely erased during the week ending June 19, when prices plunged another 5.81%.

The decline was driven by:

- Continued weakness in crude oil and feedstock markets.

- Further declines in PGP pricing.

- Aggressive inventory liquidation by downstream processors.

- Reduced spot-market participation from automotive and packaging manufacturers.

Major consumers increasingly relied on previously purchased high-cost inventories rather than re-entering the market, intensifying downward pressure on spot resin prices.

Primary Market Catalysts & Recent Developments

- The PGP Feedstock Cascade

The collapse of Polymer Grade Propylene (PGP) remains the primary price depressor. June PGP calendar swaps settled near $0.38 per pound down from post-crisis peaks.

High refinery utilization and smooth Gulf Coast NGL fractionation triggered drop in cash production costs, forcing producers to aggressively slash resin quotes.

- Strategic Global Plant Turnarounds

Producers are managing the downward cycle through calculated maintenance rather than running into a severe oversupply trap:

- Zhongjing Petrochemical (China): Took its major PP unit off-stream in mid-June for turnaround maintenance.

- Jinneng Science & Technology (China): Restarted its large unit in early June, offsetting regional tightness.

- PetroChina Hohhot: Scheduled an extended maintenance shutdown for July 2026 to limit Q3 inventory buildup.

- The Indian Tariff Cliff and Regulatory Curbs

International arbitrage faced major disruptions due to South Asian regulatory shifts. India’s temporary 7.5% import duty waiver on polymers is officially set to expire on June 30, 2026, causing global buyers to turn highly cautious.

Concurrently, New Delhi restricted feedstock diversion by prioritizing domestic propane/butane for LPG fuel, squeezing Indian PP operating rates and forcing local producers like Reliance (RIL) to raise domestic prices.

- Downstream Buyer Boycotts vs. Specialized Premiums

After Q1 panic-purchasing, automotive molders and rigid packaging plants have adopted strict hand-to-mouth procurement, burning through expensive warehouse stocks.

However, specialized sectors show long-term structural resilience. While commodity homopolymers bleed, high-precision Mineral-Filled PP Compounds and sustainable initiatives, such as INEOS’s new rPP1025C grade (70% mechanically recycled post-consumer material) meeting European mandates, are maintaining firm premium pricing.

Polypropylene Market Outlook

The substantial -5.81% drop on June 19 confirms the post-crisis correction in the US polypropylene market is still active, though spot prices are closely approaching their ultimate production-cost floor.

Barring sudden, severe Gulf Coast hurricane disruptions or a renewed flare-up in international logistics corridors, the US PP price trend is heavily favored to transition into a stable, sideways trading pattern later this summer.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.