The unbeached kraftliner market on a free-delivered Hamburg basis is regaining its footing after a turbulent spring.

Weeks of soft, demand-led drift across Germany and the wider Western European packaging belt where subdued industrial output and cautious corrugated-box buying met ample regional supply gave way in late May to a sharp, cost-driven rebound that reset price floors almost overnight.

With major European producers pushing kraftliner increases, escalating Northern Bleached Softwood Kraft (NBSK) and Bleached Hardwood Kraft Pulp (BHKP) prices, and an energy market jolted by renewed Middle East tensions, the question for converters delivering into Hamburg is no longer whether prices have bottomed out, but how firmly the new floor will hold.

Beneath the headline weakness, demand for premium virgin-fiber liner, the high-burst outer facing that recycled test liner cannot fully replicate has proved more resilient than the soft patch suggested.

Unbleached Kraftliner Market Before the Rebound

Before the late-May turn, FD Hamburg kraftliner had been grinding lower for much of the period. German and Western European downstream demand stayed lackluster as weak manufacturing activity, soft consumer-goods volumes and a hesitant industrial economy weighed on corrugated-box order books.

Buyers, conscious of comfortable mill inventories and steady supply, purchased close to immediate need and resisted forward commitments.

Across global markets, NBSK and BHKP pulp benchmarks have softened, trimming the virgin-fiber cost base and giving mills little reason to defend quotations.

Notably, while Spanish and Italian producers had already begun lifting unbleached kraftliner prices, Germany and France lagged the move leaving FD Hamburg realizations easing modestly into a spring low even as the regional cost picture quietly turned.

By the trough, the delivered market looked oversold relative to the cost pressures building beneath it, setting the stage for an abrupt repricing.

Unbleached Kraftliner Market After the Recovery

So, what changed? In short, cost-push pressure overwhelmed soft demand. Major European producers moved decisively, implementing kraftliner increases that effectively reset regional pricing floors. The drivers were structural rather than demand led.

As a pure virgin-fiber grade, unbleached kraftliner tracks pulp rather than recovered paper, and both of its key benchmarks turned higher: NBSK and BHKP costs escalated sharply, while rising international woodchip and pulpwood premiums and elevated electricity costs during periods of grid pressure pushed manufacturing expenses higher across the European mill base.

Layered on top, the Israel–Iran conflict reshaped global energy markets with Brent crude vaulting past US$110 a barrel and Strait of Hormuz transit collapsing at the peak of the crisis feeding directly into the natural-gas and electricity bills that European kraftliner mills cannot escape.

Supply, meanwhile, had quietly tightened: Mondi’s closure of its Bulgarian mill marked a structural reduction in regional capacity, leaving fewer tonnes to absorb the demand that did materialize.

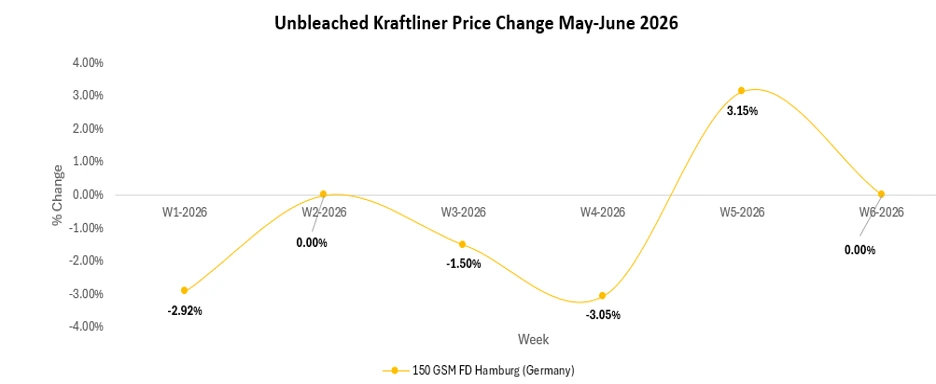

The result was the sharp single-week jump visible in the chart, a cost-led reset rather than a demand surge.

Source: Price Watch™ Unbleached Kraftliner

Holding the Line: The Market Finds Its Footing

Where does the FD Hamburg kraftliner market stand now? After the rebound, prices have flattened rather than retraced a telling sign.

Converters appear to be accepting the new floor, covering requirements at the reset levels rather than holding out for a pullback.

Demand, while far from booming, is holding firm: e-commerce parcel growth and the premium placed on high-burst virgin liner for retail-ready and shelf-display packaging continue to underpin offtake that recycled grades struggle to serve.

With the cost increases now largely absorbed and supply discipline intact, the delivered Hamburg market has settled into an uneasy equilibrium neither chasing higher nor giving back the gains.

Unbleached Kraftliner Market Outlook

So, what lies ahead for Germany’s delivered kraftliner market? The near-term direction hinges on costs more than volumes.

Should energy markets stay elevated on continued Middle East uncertainty, and should NBSK and BHKP costs hold their ground, the reset floor looks defensible and further selective increases cannot be ruled out.

Conversely, any easing of the energy shock or a softening of pulp benchmarks would test producers’ resolve, particularly if German industrial demand stays subdued.

Structural capacity discipline underscored by Mondi’s Bulgarian closure and broader European rationalization tilts the balance toward firmness, but cautious buyer behavior and weak macro fundamentals cap the upside.

Continued monitoring of NBSK and BHKP pulp parity, virgin pulpwood and wood-chip costs, European energy prices and German manufacturing output will be critical as the market navigates this cost-led phase.

Mills with captive energy, integrated fiber supply and disciplined inventory management are best positioned to defend margins through the transition.

Subscribe to Price Watch™ today to get weekly updates and stay informed on FD Hamburg unbleached kraftliner price movements.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.