Price Watch™ provides real-time price assessments and price forecasts for Expandable Polystyrene (EPS) across top trading regions:

| Expandable Polystyrene (EPS) Regional Coverage | Expandable Polystyrene (EPS) Grade and Country Coverage | Expandable Polystyrene (EPS) Pricing Data Coverage Explanation |

| Asia-Pacific Expandable Polystyrene (EPS) Pricing Analysis | EPS General Grade (Bead Size: 0.5–1.25) FOB Prices at Shanghai Port, China | Weekly Price Update on Expandable Polystyrene (EPS) Real-Time Export Prices from Shanghai Port, China to Global Markets |

| EPS General Grade (Bead Size: 0.5–1.25) CIF Prices at Bangkok Port, Thailand, Importing from China | Weekly Price Update on Expandable Polystyrene (EPS) Real-Time Import Prices at Bangkok Port, Thailand from China | |

| EPS High Expansion (Bead Size: 0.5–1) Ex-Mumbai Domestic Prices, India | Weekly Price Update on Expandable Polystyrene (EPS) Real-Time Domestic Prices in Ex-Mumbai, India | |

| Europe Expandable Polystyrene (EPS) Pricing Analysis | EPS General Grade (Bead Size: 0.5–1.10) FD Amsterdam Domestic Prices, Netherlands | Weekly Price Update on Expandable Polystyrene (EPS) Real-Time Domestic Prices in Amsterdam Port, Netherlands |

| EPS General Grade (Bead Size: 0.5–1.10) FD Hamburg Domestic Prices, Germany | Weekly Price Update on Expandable Polystyrene (EPS) Real-Time Domestic Prices in Hamburg Port, Germany | |

| Middle East & Africa Expandable Polystyrene (EPS) Pricing Analysis | EPS General Grade (Bead Size: 0.5–1.25) CIF Prices at Jebel Ali Port, United Arab Emirates, Importing from China | Weekly Price Update on Expandable Polystyrene (EPS) Real-Time Import Prices at Jebel Ali Port, United Arab Emirates from China |

| EPS General Grade (Bead Size: 0.5–1.25) CIF Prices at Jeddah Port, Saudi Arabia, Importing from China | Weekly Price Update on Expandable Polystyrene (EPS) Real-Time Import Prices at Jeddah Port, Saudi Arabia from China |

EPS Price Forecasts & Market Foresight Q3 2026

Outlook: Strongly Bearish

Confidence: High

EPS prices are expected to remain in a correction phase globally during Q3 2026, influenced by softer Styrene and Benzene cost support, comfortable supply availability, and need-based procurement trends. Europe may witness a relatively sharper adjustment in the early part of the quarter due to ample inventories and slow recovery in construction and packaging demand, with prices stabilizing toward the end of the quarter.

Asia is likely to see subdued demand, particularly in India during the monsoon season, alongside competitive regional offers and steady import availability. North America may follow a more balanced trend, with stable supply-demand fundamentals limiting sharp declines while maintaining a slightly downward pricing trajectory.

Global EPS Market Overview by Region (July–September 2026)

| Country | Grade/ Incoterm | Outlook |

| Netherlands | General Grade (Bead Size: 0.5-1.10) FD Amsterdam | Strongly Bearish |

| China | General Grade (Bead Size: 0.5-1.25) FOB Shanghai | Strongly Bearish |

| Saudi Arabia | General Grade (Bead Size: 0.5-1.25) CIF Jeddah (China) | Strongly Bearish |

| India | High Expansion (Bead Size: 0.5-1) Ex-Mumbai | Strongly Bearish |

| Thailand | General Grade (Bead Size: 0.5-1.25) CIF Bangkok (China) | Strongly Bearish |

| Germany | General Grade (Bead Size: 0.5-1.10) FD Hamburg, | Strongly Bearish |

| United Arab Emirates | General Grade (Bead Size: 0.5-1.25) CIF Jebel Ali (China) | Strongly Bearish |

*EPS Forecast represents an analytical assessment based on information available at the time of publication. Actual market prices may vary due to unforeseen operational, regulatory, geopolitical, or economic developments.

Explore the Complete Price Watch™ EPS Forecast

Access comprehensive EPS market intelligence, including a 3-Month Rolling Forecast, 12-Month Price Forecast, forward price curves, country-wise market outlooks, procurement insights, and monthly forecast updates.

Explore Price Watch™ EPS Forecasts

What’s Included

The 3-Month Forecast (Updated Monthly)

It reflects changes in Styrene feedstock costs, energy prices, producer operating rates, plant outages, inventory levels, trade flows, freight rates, regional demand, and geopolitical developments affecting the global EPS market.

The 12-Month Forecast (Published Annually)

It provides a strategic outlook based on expected capacity additions, supply-demand balances, feedstock economics, macroeconomic conditions, industrial production trends, trade policies, seasonal demand patterns, and long-term supply chain developments, supporting procurement, budgeting, and strategic planning.

Our Proprietary Hybrid Forecasting Model Evaluates:

- Feedstock & production economics

- Plant operating rates & outages

- Inventory and supply-demand balance

- Regional trade flows & freight

- Import-export dynamics

- Macroeconomic & geopolitical developments

Track EPS Supply Disruptions in Real Time

As geopolitical risks continue to reshape global supply chains, stay ahead of the events that drive price movements by monitoring plant shutdowns, maintenance turnarounds, force majeure events, logistics bottlenecks, trade restrictions, and operational disruptions before they impact EPS markets.

Access the Price Watch™ GIO Tracker

EPS Price Trend Q2 2026

In Q2 2026, the global Expandable Polystyrene (EPS) prices have been increasing significantly as the US-Iran conflict has escalated and the Strait of Hormuz has faced closure, disrupting the supply of styrene and related feedstocks. Crude oil prices have been rising sharply during April and May, which has been pushing production costs higher across major regions.

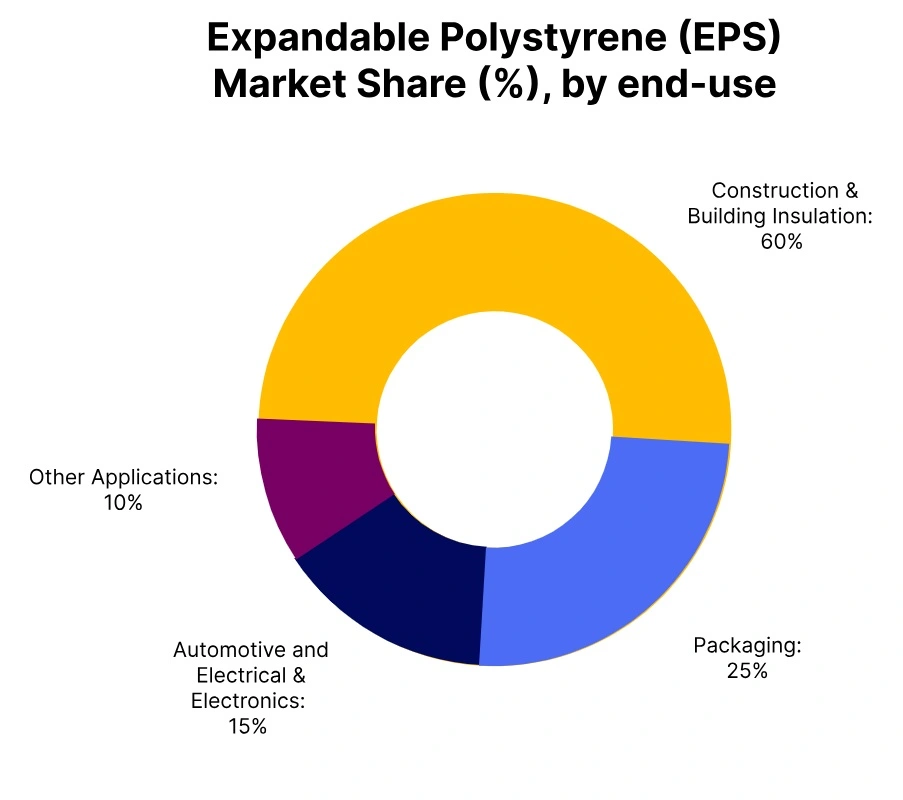

Demand from construction, insulation, and packaging sectors has been remaining firm, which has been supporting the upward price trend. Supply chains have been tightening due to logistics disruptions and higher freight costs. The EPS Price Chart has been reflecting this strong upward movement, while the EPS Price Index has been indicating slight stabilization toward the end of Q2 2026.

Germany: EPS Domestically Traded prices FD Hamburg, Germany; Grade – General Grade (Bead Size: 0.5-1.10)

In Q2 2026, Expandable Polystyrene (EPS) prices in Germany have increased by 43%. The US-Iran conflict and the closure of the Strait of Hormuz have restricted feedstock imports, which has been increasing production costs across the domestic market.

Demand from construction and insulation sectors has been remaining strong, which has been supporting higher price levels. Energy costs and operating expenses have been elevated during the quarter. Supply availability has been constrained due to limited raw material inflow. Market participants have been facing tight supply conditions.

The Expandable Polystyrene (EPS) Price Trend in Germany has been showing a strong upward movement during Q2 2026, Following the mid-June US-Iran ceasefire, Chinese offer prices and freight costs have started easing. In June 2026, EPS prices in Germany corrected by 2%, supported by softer Styrene feedstock values and improving shipping conditions.

Netherlands: EPS Domestically Traded prices FD Amsterdam, Netherlands; Grade – General Grade (Bead Size: 0.5–1.10)

In Q2 2026, Expandable Polystyrene (EPS) prices in Netherlands have increased by 42%. The US-Iran conflict and the closure of the Strait of Hormuz have restricted feedstock availability, which has been increasing production costs across the region.

Demand from packaging and construction sectors has been remaining steady, which has been supporting price levels. Supply conditions have been tight due to disruptions in raw material flow. Logistics constraints have been adding further pressure on availability. Market sentiment has been firm during the quarter.

The Expandable Polystyrene (EPS) Price Trend in Netherlands has been increasing steadily throughout Q2 2026, Following the mid-June US-Iran ceasefire, Chinese offer prices and freight costs have started easing. In June 2026, EPS prices in the Netherlands corrected by 2%, supported by softer Styrene feedstock values and improving shipping conditions.

UAE: EPS Imported prices CIF Jebel Ali, UAE from China; Grade – General Grade (Bead Size: 0.5–1.25)

In Q2 2026, Expandable Polystyrene (EPS) prices in United Arab Emirates have increased by 22%. The US-Iran conflict and the closure of the Strait of Hormuz have restricted regional trade flows, which has been increasing import costs into the country.

Dependence on Chinese supply has been influencing domestic pricing trends. Demand from construction and packaging sectors has been remaining stable, supporting the market. Freight rates and logistics challenges have been affecting supply availability. Market conditions have been moderately tight during the quarter.

The Expandable Polystyrene (EPS) Price Trend in United Arab Emirates has been showing a gradual increase throughout Q2 2026. Following the mid-June US-Iran ceasefire, Chinese offer prices and freight costs have started easing. In June 2026, EPS prices in UAE corrected by 5%, as import costs from China began to normalise, supported by softer Styrene feedstock values and improving shipping conditions.

China: EPS Export prices FOB Shanghai, China; Grade – General Grade (Bead Size: 0.5–1.25)

In Q2 2026, Expandable Polystyrene (EPS) prices in China have increased by 16%. The US-Iran conflict and the closure of the Strait of Hormuz have restricted feedstock supply, which has been impacting production costs and export dynamics.

Domestic demand has been moderate, which has been limiting sharper price increases. Supply availability has been relatively stable due to consistent operating rates. Export activity has been influenced by global logistics disruptions. Market sentiment has been balanced during the quarter.

The Expandable Polystyrene (EPS) Price Trend in China has been showing a modest increase during Q2 2026, Following the mid-June US-Iran ceasefire, Chinese offer prices and freight costs have started easing. In June 2026, EPS prices in China corrected by 9%, supported by softer Styrene feedstock values and improving shipping conditions.

Saudi Arabia: EPS Imported prices CIF Jeddah, Saudi Arabia from China; Grade – General Grade (Bead Size: 0.5–1.25)

In Q2 2026, Expandable Polystyrene (EPS) prices in Saudi Arabia have increased by 18%. The US-Iran conflict and the closure of the Strait of Hormuz have restricted regional supply chains, which has been increasing import costs.

Dependence on Asian imports has been shaping pricing trends. Demand from construction and insulation sectors has been remaining steady, supporting the market. Logistics disruptions have been affecting supply availability. Market conditions have been moderately tight throughout the quarter.

The Expandable Polystyrene (EPS) Price Trend in Saudi Arabia has been showing a gradual upward movement during Q2 2026. Following the mid-June US-Iran ceasefire, Chinese offer prices and freight costs have started easing. In June 2026, EPS prices in Saudi Arabia corrected by 4%, as import costs from China began to normalise, supported by softer Styrene feedstock values and improving shipping conditions.

Thailand: EPS Imported prices CIF Bangkok, Thailand from China; Grade – General Grade (Bead Size: 0.5–1.25)

In Q2 2026, Expandable Polystyrene (EPS) prices in Thailand have increased by 16%. The US-Iran conflict and the closure of the Strait of Hormuz have restricted global trade flows, which has been increasing import costs.

Demand from packaging and construction sectors has been remaining stable, which has been supporting price levels. Supply availability has been affected by logistics challenges and higher freight rates. Market participants have been observing steady procurement activity. Overall conditions have been balanced but firm.

The Expandable Polystyrene (EPS) Price Trend in Thailand has been showing a steady increase during Q2 2026, Following the mid-June US-Iran ceasefire, Chinese offer prices and freight costs have started easing. In June 2026, EPS prices in Thailand corrected by 9%, as import costs from China began to normalise, supported by softer Styrene feedstock values and improving shipping conditions.

India: EPS Domestically Traded prices Ex-Mumbai, India; Grade – High Expansion (Bead Size: 0.5–1)

In Q2 2026, Expandable Polystyrene (EPS) prices in India have increased by 54%. The US-Iran conflict and the closure of the Strait of Hormuz have restricted import supply of feedstock, which has been increasing domestic production costs.

Demand from construction, insulation, and packaging sectors has been remaining strong, supporting higher prices. Supply conditions have been tight due to dependence on imported raw materials. Market activity has been steady with firm buying interest. Inventory levels have been constrained during the quarter.

The Expandable Polystyrene (EPS) Price Trend in India has been showing a strong upward movement throughout Q2 2026, Following the mid-June US-Iran ceasefire, Chinese offer prices and freight costs have started easing. In June 2026, EPS prices in India corrected by 9%, supported by softer Styrene feedstock values and improving shipping conditions.