The global acetone market is defined by a concentrated production base, capital-intensive infrastructure, and supply chains that are highly susceptible to disruptions.

The GIO Tracker offers daily, asset-level insights into acetone facilities, tracking key factors such as capacity, feedstock dependencies, production processes, operational status, and historical outage data across major production regions. Acetone, a vital raw material to produce acetoneic resins, solvents, and plastics, is significantly influenced by fluctuations in propylene and benzene prices. Despite environmental concerns regarding acetone’s volatility, long-term demand remains strong, particularly due to growth in industries such as automotive, construction, and cosmetics, alongside ongoing initiatives to adopt more sustainable production methods and enhance operational efficiency.

Acetone serves as a critical chemical in various industrial processes, acting as both a solvent and an intermediate in the production of essential products like plastics, pharmaceuticals, and synthetic fibers. As a key output of the petrochemical industry, acetone directly influences a wide range of downstream markets, including coatings, adhesives, and cleaning agents, shaping the cost structure and availability of these products. Its production is highly reliant on petrochemical feedstocks, making it vulnerable to fluctuations in raw material supply and energy costs. Disruptions in acetone production, whether due to supply chain issues or refinery outages, can rapidly ripple across industries, inflating production costs for downstream manufacturers, altering trade flows, and affecting the availability of critical chemicals in ways that can persist long after the initial disruption.

The acetone supply chain is defined by high concentration, significant capital investment, and limited operational flexibility. When production capacity is disrupted, price fluctuations can behave nonlinearly, impacting multiple downstream sectors.

By implementing GIO Tracker, early warning signals for nonlinear acetone supply disruptions across the petrochemical value chain can be captured.

Utilizing GIO Tracker across your portfolio allows for the identification of emerging stress points, quantification of the impact of plant-level outages, and assessment of how these disruptions will affect downstream industries such as coatings, adhesives, pharmaceuticals, and the production of methyl methacrylate (MMA). This enables the transformation of latent operational risks into visible, actionable insights, facilitating proactive risk management before disruptions cascade through the acetone market and its critical end-use sectors.

Global Overview

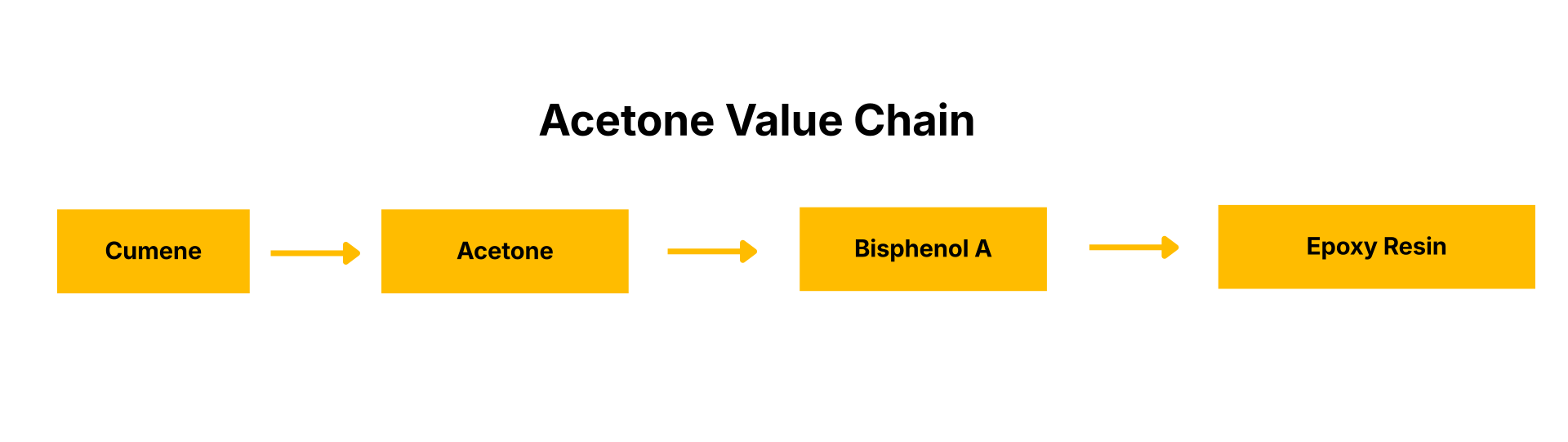

Global Acetone production reached 7M tons in 2025, increased 5% from 2024, dominant region like Asia Pacific (China: ~5M tons; South Korea: ~1M ton). The acetone industry plays a pivotal role in various downstream sectors, including BPA production, epoxy resins, and nylon fibers. Acetone is a key raw material in the production of Bisphenol A (BPA), which is used in making polycarbonate plastics and epoxy resins for applications in automotive, electronics, and coatings.

Additionally, acetone is essential in the production of epoxy resins, which are widely used in adhesives, coatings, and electrical insulation. Furthermore, it contributes to the production of nylon fibers, which are vital for textiles, automotive parts, and industrial applications.

The Global Acetone GIO Tracker offers invaluable insights into disruptions in acetone supply, allowing stakeholders in these downstream industries to proactively address risks and ensure smooth production processes, minimizing the impact of supply chain challenges in these critical markets.

Monitors over 30 acetone production facilities across the region, providing essential insights into disruptions such as environmental shutdowns, power rationing, and seismic risks that could affect production and strain both regional and global acetone supply chains. By tracking these risks, the system delivers early warnings, enabling stakeholders to proactively address potential supply disruptions and effectively manage operational challenges within the highly concentrated and interconnected acetone market.

The North America Acetone Plant Tracking monitors 5+ acetone production facilities, providing insights into production trends, feedstock availability, and operational status. This helps industries like BPA production, epoxy resins, and nylon fibers anticipate disruptions and track capacity shifts, ensuring better decision-making and stable supply chains in acetone-dependent sectors.

Monitors 5+ acetone production facilities in the region, this system delivers critical insights into feedstock shortages, regulatory changes, and capacity expansions, highlighting potential disruptions in acetone production. Early risk detection helps stakeholders take proactive actions to manage supply chain interruptions and operational challenges in the consolidated acetone market.

Monitors around 2 plants across the region, providing essential insights into disruptions like refinery maintenance, logistical challenges, and regulatory changes that can affect production and limit both regional and global butadiene flows.

Asia Pacific

North America

Europe

Middle East & Africa

China

India

South Korea

Taiwan

Thailand

Singapore

Japan

Germany

Finland

Spain

Belgium

Italy

Poland

USA

Saudi Arabia

Asia Pacific

Europe

North America

Middle East & Africa

China

India

Taiwan

South Korea

Japan

Singapore

Thailand

Germany

Finland

Italy

Spain

Poland

Belgium

USA

Saudi Arabia