The global Copper Smelter market is shaped by Andean mine concentration, capital-intensive concentrator and smelter infrastructure, and supply chains that transmit mine-level disruptions into immediate LME price reactions across downstream fabrication and manufacturing markets.

GIO Tracker delivers daily asset-level intelligence on Copper Smelter facilities covering mine production capacity, concentrator throughput, smelter operational status, feedstock dependency, and outage history across all major producing regions. From individual concentrator utilisation rates to total copper production loss by cause, every data point is captured at the facility level and updated every day. Access the operational intelligence, disruption signals, and LME price impact data needed to stay ahead of copper supply shifts before they reach the market.

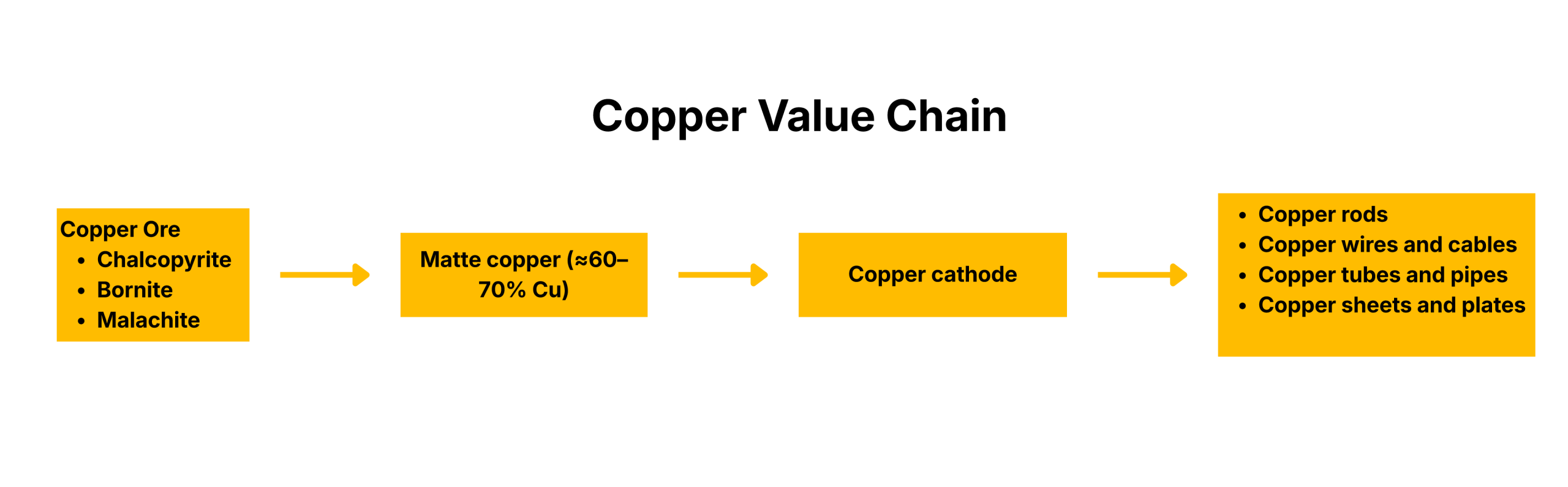

Copper Smelter sits at the foundation of electrical infrastructure, renewable energy systems, and industrial manufacturing, serving as the conductive backbone from which the broader metals and energy transition economy derives its operational capacity. As the primary output of the mine-to-cathode production chain, copper directly influences electrical wire and cable markets, EV battery and motor component availability, power generation and grid infrastructure construction costs, and industrial machinery and plumbing product supply chains.

Its production is inherently capital-intensive and geographically constrained to a small number of porphyry copper deposit clusters, meaning that capacity losses at the mine or concentrator stage are rarely absorbed quickly and tend to propagate through the value chain with outsized force. Supply disruptions at the Copper Smelter stage transmit rapidly across concentrate markets, smelter utilisation, and cathode availability, altering TC/RC benchmark dynamics, tightening physical premium markets, and inflating downstream fabricator input costs in ways that persist well beyond the initial outage.

Copper supply is Andean-concentrated, concentrator-limited, and slow to replace when disrupted. When major mine or smelter capacity goes offline, LME price and physical premium reactions are nonlinear. Get GIO Tracker for early warning on Copper Smelter supply shocks across the metals and energy transition value chain.

Put GIO Tracker to work across your portfolio to surface those stress points early, quantify at mine-level how concentrator outages, labor strikes, and environmental shutdowns will ripple through copper concentrate markets, smelter TC/RC dynamics, and downstream cathode availability, and turn hidden operational risk into visible, actionable signals before it cascades across the Copper Smelter value chain.

Global Overview

Global Copper Smelter mine production reached approximately 22 MMTPA in 2024, concentrated in Chile and Peru porphyry deposits (~38% combined), with additional production from the Democratic Republic of Congo, China, Indonesia, and the United States.

GIO Tracker provides mine-level and smelter-level visibility across 200+ facilities, focusing on operational status classification (operational, temporary shutdown, permanent shutdown) and capturing underlying causes of shutdowns, including maintenance, power constraints, environmental regulations, and unplanned disruptions to assess supply risks in LME-traded cathode and physical premium markets.

The Global Copper Smelter GIO Tracker delivers structured operational intelligence across major producing regions. Built on historical tracking since 2015, it monitors mines, concentrators, smelters, and refineries with a specific focus on status changes and disruption drivers, enabling identification of supply-side risks and short-term market imbalances impacting global copper pricing and trade flows.

Tracks 80+ smelters across the region, monitoring operational status shifts, temporary shutdown events, and permanent closures, along with key disruption drivers such as power shortages, coal availability, hydropower seasonality, and environmental inspections impacting regional and global copper balances.

Provides visibility across smelters in the United States and Canada, focusing on status tracking (operational, temporary shutdown, permanent shutdown) and identifying causes such as energy cost volatility, maintenance shutdowns, and structural closures.

Tracks 20+ smelters across Europe, focusing on shutdown tracking and operational status changes under high energy costs and tightening environmental regulations, with emphasis on power-driven curtailments, emissions compliance, and permanent capacity rationalization.

Covers key smelters operating with long-term energy supply agreements, focusing on operational continuity, shutdown events, and disruption causes affecting export-oriented production and seaborne copper availability.

Covers smelters across the region with a focus on status tracking and shutdown causes, including hydropower dependency, grid reliability, and maintenance-related disruptions influencing export availability.

Asia Pacific

Europe

South America

China

India

Japan

Philippines

Germany

Russia

Bulgaria

Spain

Chile

Peru

Asia Pacific

Europe

South America

China

India

Japan

Philippines

Germany

Russia

Bulgaria

Spain

Chile

Peru