The global lithium supply chain is shaped by geographically concentrated resources, rapidly expanding electric vehicle demand, evolving battery chemistry requirements, and the structural complexity of extracting lithium from two distinct resource types: hard-rock spodumene deposits and lithium-rich brine reservoirs. Because lithium supply is highly concentrated in a limited number of producing regions, operational disruptions at a single large operation can quickly influence global lithium chemical markets and battery supply chains.

Lithium production depends on stable extraction operations, reliable evaporation or processing infrastructure, secure access to water resources, regulatory certainty, and efficient logistics for transporting lithium concentrate or brine-derived chemicals to refining facilities. When any of these chain links weaken, due to drought conditions affecting brine evaporation ponds, mining equipment failures, price-driven curtailments, regulatory intervention, water-usage restrictions, energy shortages, or logistics disruptions, supply shortages can quickly ripple across the battery materials market.

Lithium supply disruptions rarely remain localized. When lithium extraction is reduced, downstream refiners experience feedstock shortages, lithium carbonate and lithium hydroxide prices react, and battery supply chains adjust procurement strategies.

The Lithium Supply GIO Tracker provides detailed asset-level operational intelligence across global lithium extraction operations, including both hard-rock lithium mines and brine production facilities. The platform monitors installed extraction capacity, operating status, curtailments, care-and-maintenance events, restart timelines, evaporation pond disruptions, regulatory risks, water-availability constraints, grade variability, and the full history of operational disruptions at the facility level.

Lithium plays a central role in the global energy transition and battery supply chain, serving as the primary input for lithium-ion batteries used in electric vehicles, grid-scale energy storage, consumer electronics, and renewable energy systems.

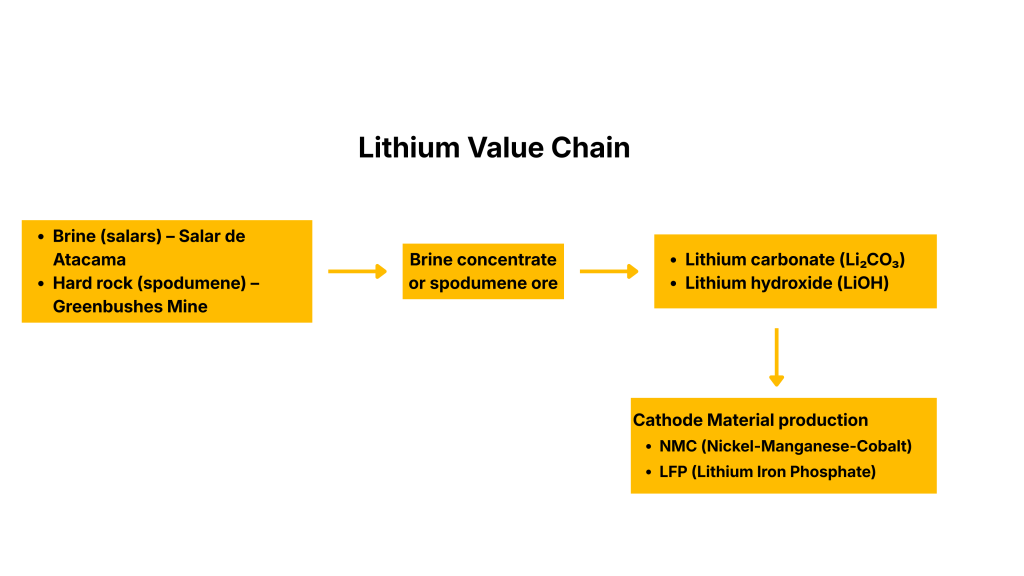

Lithium extracted from hard-rock deposits is typically converted into spodumene concentrate, while lithium recovered from brine reservoirs is processed through solar evaporation and chemical treatment to produce lithium carbonate. These intermediate products are refined into battery-grade lithium carbonate or lithium hydroxide, which serve as key feedstocks for cathode material production.

Disruptions at lithium extraction operations, caused by evaporation pond constraints, water shortages, environmental permitting issues, geotechnical challenges, price-driven curtailments, or export restrictions, can propagate rapidly through the downstream supply chain.

Extraction disruptions can affect:

Because the lithium supply chain remains relatively concentrated, even short-term curtailments at large brine operations or major hard-rock mines can tighten global markets, particularly when restart timelines remain uncertain.

Systematic asset-level operational monitoring provides early visibility of supply chain risk before it becomes visible in lithium chemical prices, contract negotiations, or battery material inventories.

Global lithium production is geographically concentrated across a limited number of regions, particularly Australia, Chile, Argentina, China, and emerging African producers. A small number of large operations account for a significant share of global lithium supply.

Hard-rock lithium mines dominate production in Australia and China, while brine extraction in South America’s Lithium Triangle, Chile and Argentina, represents a major share of global lithium resources.

Weather variability affecting evaporation ponds, water resource constraints in arid regions, energy supply reliability, and tightening environmental regulations are increasingly influencing lithium supply trends.

The Lithium Supply GIO Tracker provides early warning of these operational challenges.

By systematically monitoring mine disruptions, evaporation pond performance, water availability, maintenance shutdowns, care-and-maintenance events, restart timelines, regulatory developments, and geopolitical risk, the platform enables clients to anticipate supply shortages before they impact lithium chemical markets or battery production.

Global Overview

Global lithium production has expanded rapidly over the past decade, reaching more than 1 million tonnes of lithium carbonate equivalent (LCE) annually as electric vehicle demand accelerates. Supply is derived from both hard-rock mining operations and brine extraction projects, spread across fewer than 30 producing countries.

Lithium supply remains highly sensitive to disruptions at large operations, particularly when lithium prices decline sharply or regulatory approvals delay new projects.

The Lithium Supply GIO Tracker provides structured asset-level intelligence across the world’s major lithium extraction facilities.

Based on historical disruption analysis since 2015, the platform tracks operational status, capacity expansions, grade variability, care-and-maintenance events, restart schedules, evaporation pond constraints, regulatory developments, and quantified production losses across all major lithium-producing regions.

The tool systematically monitors extraction developments, providing early warning signals that could influence:

Tracks + lithium extraction operations across the region, monitoring operational performance, project expansions, and disruptions across both hard-rock mines and emerging lithium brine projects.

Recent disruptions have been driven by lithium price volatility, processing bottlenecks, weather-related interruptions, and environmental compliance requirements.

Major operations include Greenbushes, Pilgangoora, Mount Marion, and Wodgina, which collectively represent a substantial share of global spodumene concentrate supply.

The tracker captures operational risks such as mine expansions, processing plant outages, grade variability, logistics disruptions, and price-driven curtailments shaping global lithium concentrate availability.

Provides integrated visibility across major Lithium mining regions in North America, where sulfide deposits represent a critical source of high-grade Lithium concentrate used in refined Lithium and battery material production. The region’s mines are typically underground operations with long reserve lives and strong integration with domestic refining facilities.

The tracker monitors underground mining disruptions, labor negotiations, power supply reliability, maintenance shutdowns, and environmental compliance developments that influence regional Lithium concentrate availability and downstream refining activity.

Europe’s Lithium production is concentrated in a limited number of sulfide deposits, primarily in Russia and Finland.

Lithium mining activity in Middle East & Africa is concentrated in a small number of large laterite projects.

South America hosts several large laterite Lithium deposits, primarily located in Brazil and Colombia, where Lithium production is integrated with ferroLithium and intermediate processing facilities supplying global stainless steel markets.

Asia Pacific

Europe

South America

Middle East & Africa

Australia

China

Hungary

France

Germany

UK

Serbia

Czech Republic

Austria

Spain

USA

Canada

Mexico

Bolivia

Argentina

Chile

Peru

Brazil

Israel

Brazil

Namibia

Ghana

Democratic Republic of the Congo

Mali

Zimbabwe

Asia Pacific

Europe

South America

Middle East & Africa

Australia

China

Hungary

France

Germany

UK

Serbia

Czech Republic

Austria

Portugal

Spain

USA

Mexico

Canada

Bolivia

Argentina

Chile

Peru

Brazil

Israel

Namibia

Ghana

Democratic Republic of the Congo

Mali

Zimbabwe