The global nickel supply chain is shaped by several structural forces. Production is heavily concentrated in a few key laterite mining regions, while sulfide ore grades in mature mining basins continue to decline. At the same time, Indonesia has rapidly expanded its processing capacity, and demand from stainless steel and electric vehicle battery supply chains is accelerating.

Because of these dynamics, disruptions at even a single large nickel mine or processing hub can quickly affect global nickel supply and refined metal markets.

The Nickel Mines GIO Tracker provides detailed operational intelligence at the individual mine level across major nickel-producing regions. It monitors installed mining capacity (Ktpa), operational status, curtailments, care-and-maintenance suspensions, restart timelines, seasonal shutdowns, geopolitical risks, ore grade changes, and the complete history of disruptions since 2015.

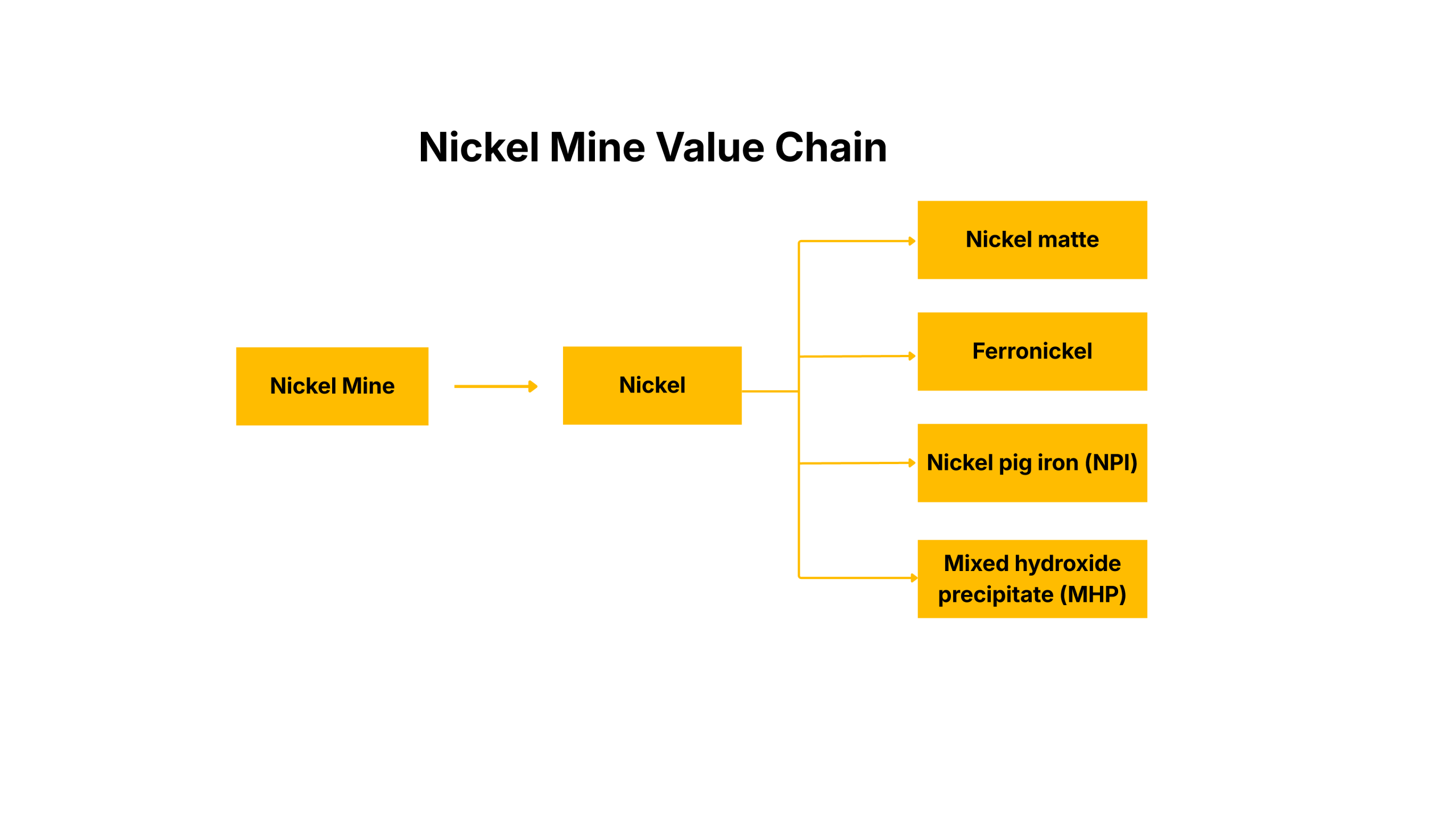

Nickel plays a vital role in the global industrial metals ecosystem. Approximately 65–70% of global nickel demand is driven by stainless steel production. However, demand from lithium-ion batteries used in electric vehicles and energy storage systems is growing rapidly.

Nickel is also widely used in:

Disruptions at the mine level, whether caused by underground flooding, geotechnical challenges, laterite ore depletion, export restrictions, ESG compliance issues, or logistics disruptions, can quickly ripple through downstream markets.

Mine disruptions can influence:

In tight feedstock markets, even short-term disruptions at large laterite operations or major sulphide deposits can shift the global nickel balance and trigger rapid price movements.

Systematic monitoring at the mine level makes it possible to identify emerging supply risks long before they appear in official production statistics or exchange inventory data.

Global nickel mine production is geographically concentrated in a handful of major regions and a relatively small number of mining companies control a large share of global nickel supply.

In recent years, several structural trends have reshaped the industry:

The Nickel Mines GIO Tracker helps identify these operational developments early. By monitoring outages, grade declines, weather disruptions, maintenance shutdowns, care-and-maintenance suspensions, restart schedules, and geopolitical risks, the platform enables users to anticipate supply constraints before they affect nickel prices or downstream manufacturing costs.

Global Overview

Global nickel mine production currently exceeds 3.5 million tonnes per year, distributed across more than 30 producing countries. Supply growth in recent years has been dominated by Indonesian laterite projects, while traditional sulfide mining regions continue to play a key role in supplying high-grade nickel concentrate.

The Nickel Mines GIO Tracker provides structured asset-level intelligence across major nickel mines worldwide. Built on disruption analysis since 2015, the platform tracks operating status, capacity changes, ore grade variability, care-and-maintenance events, restarts, force majeure declarations, and quantified production losses across major producing regions.

The tool systematically tracks mine-level developments, providing early warning signals that may impact:

Tracks + mines across the region, monitoring operational, regulatory, and seasonal disruptions affecting the world’s largest nickel supply base.

Provides integrated visibility across major nickel mining regions in North America, where sulfide deposits represent a critical source of high-grade nickel concentrate used in refined nickel and battery material production. The region’s mines are typically underground operations with long reserve lives and strong integration with domestic refining facilities.

Europe’s nickel production is concentrated in a limited number of sulfide deposits, primarily in Russia and Finland.

Nickel mining activity in Middle East & Africa is concentrated in a small number of large laterite projects.

South America hosts several large laterite nickel deposits, primarily located in Brazil and Colombia, where nickel production is integrated with ferronickel and intermediate processing facilities supplying global stainless-steel markets.

Asia Pacific

Europe

North America

South America

Middle East & Africa

Australia

China

Russia

Indonesia

Papua New Guinea

Philippines

Finland

Russia

Canada

USA

Brazil

Colombia

Canada

Cuba

Venezuela

Madagascar

Morocco

South Africa

Zimbabwe

Asia Pacific

Europe

North America

South America

Middle East & Africa

Australia

China

Indonesia

Papua New Guinea

Philippines

Finland

Russia

Canada

USA

Brazil

Colombia

Cuba

Venezuela

Madagascar

Morocco

South Africa

Zimbabwe