The global polyvinyl chloride (PVC) market is characterized by a highly integrated production base, significant capital investments, and supply chains sensitive to fluctuations.

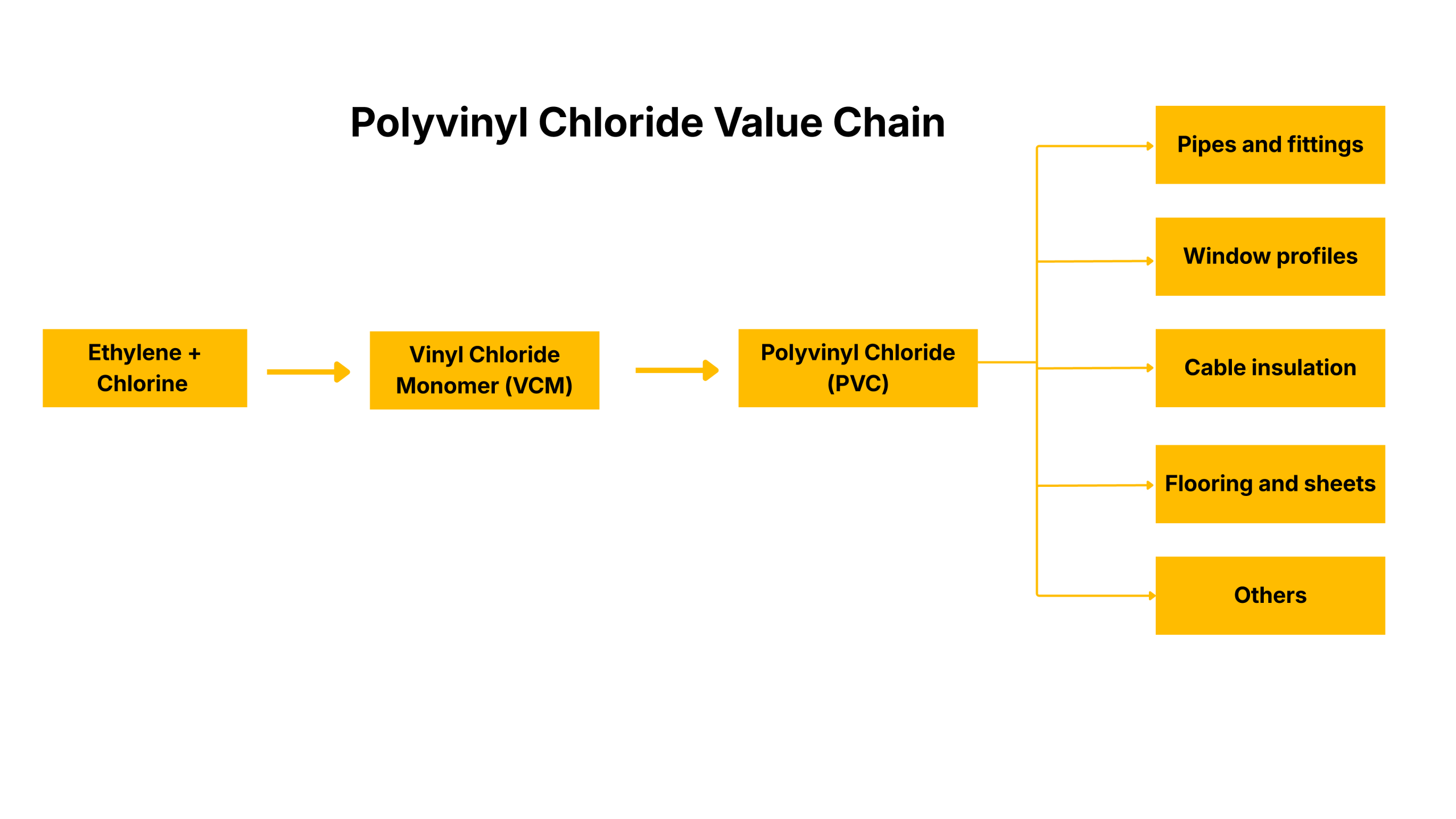

The GIO Tracker provides daily, asset-level insights into PVC facilities, monitoring production capacity, feedstock dependencies (primarily ethylene dichloride (EDC) and vinyl chloride monomer (VCM)), operational status, plant outages, and maintenance histories across major production regions. PVC is a critical feedstock in the production of pipes, profiles, flooring, cables, and films, and is significantly impacted by shifts in the prices of crude oil and petrochemical derivatives.

PVC production is influenced by fluctuations in crude oil prices, environmental concerns, and growing demand from industries such as automotive and construction. By assessing plant-level disruptions and supply chain impacts, the tracker helps stakeholders manage supply risks, optimize sourcing strategies, and maintain operational continuity in a volatile market.

PVC plays a crucial role across industries such as construction, automotive, healthcare, and consumer goods. It is essential in producing pipes, flooring, automotive parts, medical devices, and packaging. As a capital-intensive product reliant on petrochemical feedstocks, disruptions in PVC production, such as feedstock shortages or plant outages, can have significant downstream effects. These disruptions can lead to tight supply, increased costs, and delays, particularly in construction and automotive sectors. Additionally, environmental concerns about PVC’s carcinogenic properties are driving the adoption of more sustainable production methods, potentially reshaping its downstream impact in the future.

PVC supply is highly concentrated, capital-intensive, and vulnerable to disruptions. When production capacity is impacted, price fluctuations can be unpredictable and significant.

Deploy GIO Tracker across your operations to spot emerging stress points, assess how plant-level disruptions will impact PVC production for pipes, flooring, profiles, and medical devices, and convert hidden operational risks into clear, actionable insights before they ripple through downstream markets.

Use GIO Tracker to receive early alerts on potential PVC supply shocks affecting critical sectors such as construction, automotive, and healthcare. Stay proactive against changes in feedstock availability and evolving environmental regulations to ensure stability within the PVC value chain.

Global Overview

Global PVC production reached 35+ million tonnes in 2025, PVC production remained almost stable from 2024, dominant regions like Asia (China: ~20M+ tpa; South Korea: ~1M tpa).

The Global PVC GIO Tracker provides real-time, plant-level operational intelligence focused on the downstream effects of PVC production. By monitoring over 125 facilities globally, particularly in dominant regions like Asia-Pacific (China: ~20M tpa; South Korea: ~2M tpa), and integrating data on capacity, utilization, and disruption signals, the tracker identifies vulnerabilities in PVC supply chains that impact key downstream industries.

These include construction, automotive, healthcare, and consumer goods, where disruptions in PVC production can directly affect the availability and cost of critical materials. The tracker allows for early detection of emerging supply risks, helping stakeholders forecast potential disruptions and proactively adjust strategies to minimize their impact across the value chain.

The Asia Pacific PVC Plant Tracker monitors 70+ plants across the region, offering critical insights into operational risks such as shutdowns, power rationing, and seismic risks that could disrupt PVC production and impact both regional and global PVC flows. By tracking these factors, the system provides early warnings, helping stakeholders anticipate potential supply disruptions and manage operational challenges in the highly concentrated and interconnected PVC market. This allows companies to take proactive measures to mitigate risks and ensure a steady supply of PVC for downstream industries, including construction, automotive, and plastics manufacturing.

North America PVC Plant Tracking monitors over 15 plants across the region, providing critical insights into disruptions such as refinery maintenance, logistical challenges, and policy changes that can affect production and tighten both regional and global PVC flows. This system offers early warnings, enabling stakeholders to anticipate supply disruptions and make informed decisions in a complex and interconnected PVC market.

Tracks over 20 plants across the region, offering vital insights into disruptions such as refinery maintenance, logistical issues, and regulatory changes that can impact production and constrain both regional and global PVC flows.

Monitors 5+ plants across the region, providing essential insights into disruptions like refinery maintenance, logistical challenges, and regulatory changes that can affect production and limit both regional and global PVC flows.

Tracks 5+ facilities region-wide, delivering critical visibility into refinery outages, logistics bottlenecks, and regulatory impacts affecting local/global PVC supply flows.

Asia Pacific

North America

South America

Europe

Middle East & Africa

China

India

Pakistan

South Korea

Taiwan

Thailand

Bangladesh

Japan

Vietnam

Malaysia

Indonesia

Philippines

Uzbekistan

Germany

France

Finland

Spain

Belgium

Poland

Czech Republic

Norway

Sweden

UK

Hungary

Portugal

Netherlands

Ukraine

Russia

Turkey

USA

Mexico

Brazil

Argentina

Colombia

Venezuela

Iran

Saudi Arabia

Egypt

Morocco

South Africa

Asia Pacific

Europe

North America

South America America

Middle East & Africa

China

Taiwan

Japan

South Korea

India

Bangladesh

Pakistan

Vietnam

Indonesia

Thailand

Malaysia

Philippines

Uzbekistan

Germany

Netherlands

Belgium

France

Norway

Spain

Sweden

UK

Hungary

Czech Republic

Portugal

Poland

Turkey

Russia

Ukraine

Finland

USA

Mexico

Brazil

Colombia

Argentina

Venezuela

Saudi Arabia

Iran

Egypt

South Africa

Morocco