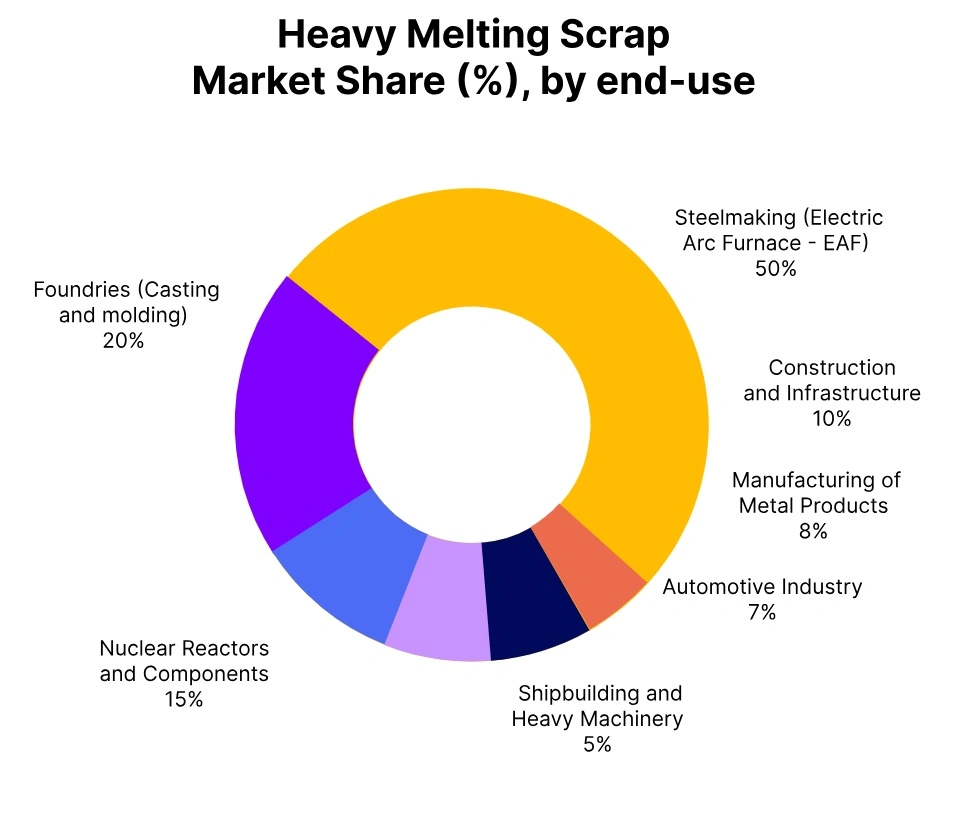

Price-Watch’s most active coverage of Heavy Melting Scrap price assessment:

- 1&2 (80:20) FOB Rotterdam, Netherlands

- 1&2 (80:20) Del Chicago, USA

- 1&2 (80:20) EX Iskenderun, Turkey

Heavy Melt Scrap Price Trend Q3 2025

As of Q3 2025, Heavy Melting Scrap (HMS) prices on the global market have been on a downward trend, influenced by a weak demand environment created by steelmakers, an oversupply of scrap, and competition from alternative raw materials such as DRI and billet. Significant price declines month on month noted in Turkey and the EU, where the price drop for Turkish import scrap has been about 2.2% in September.

The rise in freight costs, currency volatility, and weak construction activity have exerted additional pressure on scrap prices. Unless there is a solid recovery in demand or a dislocation of supply, Heavy Melting Scrap prices are likely to remain under downward pressure until the end of the quarter.

USA: Heavy Melt Scrap Domestically Traded Heavy Melt Scrap price, DEL Alabama, the US, Grade- 1&2 (80:20).

According to PriceWatch, in Q3 2025, the heavy melt scrap (HMS) price trend in U.S. market experienced a 1.78% decrease in prices compared to Q2, driven by softer demand from steel mills, tighter margins, and stable to slightly oversupplied scrap availability. The heavy melt scrap (HMS) price trend showed a mild but steady decline, reflecting cautious buying behaviour and limited export opportunities.

While supply remained relatively consistent, slowing downstream steel production and minimal export demand weighed on pricing. Regional dynamics and mill inventories influenced localized variations, but overall, the market remained stable with no sharp volatility, suggesting a correction rather than a downturn.

The 2.11% decrease in Heavy Melt scrap prices in the USA during September 2025 can be attributed to weaker demand from domestic steel mills amid slower construction activity. Additionally, increased scrap supply from demolition projects may have further pressured prices downward.

Netherlands: Heavy Melt Scrap Export prices FOB Rotterdam, Netherlands, Grade- 1&2 (80:20).

The heavy melt scrap price trend in the Netherlands for Q3 2025 indicated a 2.25% decrease from Q2. The decline has been tied to sustained weak demand for heavy melt scrap in the steel sector, as well as high levels of inventories and limited amounts of exporting, especially to Turkey. Heavy melt scrap inventories continue to grow, with high collection rates from the supply side, resulting in an oversupply within the local market, which weighs heavily on the scrap price.

Additionally, because Dutch merchants are major players in international scrap exports, an overall decline in demand for heavy melt scrap globally directly affects the Netherlands prices. Unless there is higher demand or stimulus policies, there has been a caution to notate a bearish attitude in the heavy melt scrap market as Q4 begins.

Heavy Melt Scrap prices in the Netherlands declined by 0.51% in September 2025, the factors leading to this decrease have been tied to the lack of demand from steel mills in the Netherlands due to slowing construction activity. Furthermore, the increased supply of heavy melt scrap from the domestic recycling sector contributed to the downward pressure on prices.

Turkey: Heavy Melt Scrap Domestically Traded Heavy Melt Scrap price, Ex-Iskenderun, Turkey, Grade- 1&2 (80:20).

In Q3 2025, the heavy melt scrap price trend in Turkey has shown a moderate decline of approximately 2.27% compared to Q2, driven by continued weak domestic steel demand, oversupply in the scrap market, and competition from billet imports. Despite this downward pressure, prices are unlikely to fall sharply as sellers resist deep cuts and mills maintain cautious buying amid subdued rebar and construction activity.

Overall, the market outlook remains soft but stable, with limited downside risk unless there is a sudden shift in steel demand or external factors impacting supply and cost dynamics. The 0.95% decrease in Heavy Melt scrap prices in Turkey in September 2025 can be attributed to weakened demand from local steel mills amid slowing construction activity and increased availability of cheaper scrap imports. Additionally, global economic uncertainty and currency fluctuations may have exerted downward pressure on scrap metal pricing.