Price Watch™ provides real-time price assessments and price forecasts for Neopentyl Glycol (NPG) across top trading regions:

| Neopentyl Glycol (NPG) Regional Coverage | Neopentyl Glycol (NPG) Grade and Country Coverage | Neopentyl Glycol (NPG) Pricing Data Coverage Explanation |

|

Asia-Pacific Neopentyl Glycol (NPG) Pricing Analysis |

Neopentyl Glycol Flakes (99.5% min purity) FOB Prices at Shanghai Port, China | Weekly Price Update on Neopentyl Glycol Flakes Real-Time Export Prices from Shanghai Port, China to Global Markets |

| Neopentyl Glycol Flakes (99.2% min purity) FOB Prices at Busan Port, South Korea | Weekly Price Update on Neopentyl Glycol Flakes Real-Time Export Prices from Busan Port, South Korea to Global Markets

|

|

| Neopentyl Glycol Flakes (99.2% min purity) CIF Prices at JNPT Port, West India, Imported from South Korea | Weekly Price Update on Neopentyl Glycol Flakes Real-Time Import Prices at JNPT Port, West India from South Korea | |

| Neopentyl Glycol Flakes (99.2% min purity) CIF Prices at Jakarta Port, Indonesia, Imported from South Korea | Weekly Price Update on Neopentyl Glycol Flakes Real-Time Import Prices at Jakarta Port, Indonesia from South Korea | |

| Neopentyl Glycol Flakes (99.5% min purity) CIF at JNPT Port West India, Imported from China | Weekly Price Update on Neopentyl Glycol Flakes Real-Time Import Prices at JNPT Port, West India from China

|

|

| Neopentyl Glycol Flakes (99.2% min purity) Ex-Mumbai Domestic Prices, West India | Weekly Price Update of Neopentyl Glycol Flakes Real-Time Domestic Prices in Mumbai, West India | |

| North America Neopentyl Glycol (NPG)

Pricing Analysis

|

Neopentyl Glycol Flakes (99% min purity) FOB Prices at Houston Port, USA | Weekly Price Update on Neopentyl Glycol Flakes Real-Time Export Prices from Houston Port, USA to Global Markets |

| South America Neopentyl Glycol (NPG)

Pricing Analysis

|

Neopentyl Glycol Flakes (99.5% min purity) CIF Prices at Santos Port, Brazil, Imported from China | Weekly Price Update on Neopentyl Glycol Flakes Real-Time Import Prices at Santos Port, Brazil from China |

| Neopentyl Glycol Flakes (99.2% min purity) CIF Prices at Santos Port, Brazil, Imported from South Korea | Weekly Price Update on Neopentyl Glycol Flakes Real-Time Import Prices at Santos Port, Brazil from South Korea | |

| Europe Neopentyl Glycol (NPG)

Pricing Analysis

|

Neopentyl Glycol Flakes (99.2% min purity) CIF Prices at Mersin Port, Turkey, Imported from South Korea | Weekly Price Update on Neopentyl Glycol Flakes Real-Time Import Prices at Mersin Port, Turkey from South Korea

|

Neopentyl Glycol Price Forecasts & Market Foresight Q3 2026

Outlook: Strongly Bearish

Confidence: High

During Q3 2026, Neopentyl Glycol prices are expected to decline across the Asian market due to comfortable supply availability, weaker formaldehyde feedstock costs, and subdued seasonal demand amid monsoon-related slowdowns. In contrast, the USA market is anticipated to witness a modest increase, supported by balanced domestic supply, steady procurement from downstream coatings and resin manufacturers, and improving buying activity.

Overall, regional market trends are expected to remain mixed, with Asia under correction while North America maintains comparatively firmer fundamentals.

Global Neopentyl Glycol Market Overview by Region (July–September 2026)

| Country | Grade/ Incoterm | Outlook |

| China | Flakes (99.5% min purity) FOB Shanghai | Mildly Bearish to Strongly Bearish |

| South Korea | Flakes (99.2% min purity) FOB Busan | Mildly Bearish to Strongly Bearish |

| USA | Flakes (99% min purity) FOB Houston | Stable to Bearish |

| India | Flakes (99.2% min purity) CIF JNPT_South Korea | Mildly Bearish to Bearish |

| Indonesia | Flakes (99.2% min purity) CIF Jakarta_South Korea | Mildly Bearish to Strongly Bearish |

| India | Flakes (99.5% min purity) CIF JNPT_China | Mildly Bearish to Strongly Bearish |

| Turkey | Flakes (99.2% min purity) CIF Mersin_South Korea | Mildly Bearish to Strongly Bearish |

| Brazil | Flakes (99.5% min purity) CIF Santos_China | Mildly Bearish to Strongly Bearish |

| Brazil | Flakes (99.2% min purity) CIF Santos_South Korea | Mildly Bearish to Strongly Bearish |

| India | Flakes (99.2% min purity) Ex-Mumbai | Mildly Bearish to Strongly Bearish |

*Neopentyl Glycol Forecast represents an analytical assessment based on information available at the time of publication. Actual market prices may vary due to unforeseen operational, regulatory, geopolitical, or economic developments.

Explore the Complete Price Watch™ Neopentyl Glycol Forecast

Access comprehensive Neopentyl Glycol market intelligence, including a 3-Month Rolling Forecast, 12-Month Price Forecast, forward price curves, country-wise market outlooks, procurement insights, and monthly forecast updates.

Explore Price Watch™ Neopentyl Glycol Forecasts

What’s Included

The 3-Month Forecast (Updated Monthly)

It reflects changes in Isobutyraldehyde and formaldehyde feedstock costs, energy prices, producer operating rates, plant outages, inventory levels, trade flows, freight rates, regional demand, and geopolitical developments affecting the global Neopentyl Glycol market.

The 12-Month Forecast (Published Annually)

It provides a strategic outlook based on expected capacity additions, supply-demand balances, feedstock economics, macroeconomic conditions, industrial production trends, trade policies, seasonal demand patterns, and long-term supply chain developments, supporting procurement, budgeting, and strategic planning.

Our Proprietary Hybrid Forecasting Model Evaluates:

- Feedstock & production economics

- Plant operating rates & outages

- Inventory and supply-demand balance

- Regional trade flows & freight

- Import-export dynamics

- Macroeconomic & geopolitical developments

Track Neopentyl Glycol Supply Disruptions in Real Time

As geopolitical risks continue to reshape global supply chains, stay ahead of the events that drive price movements by monitoring plant shutdowns, maintenance turnarounds, force majeure events, logistics bottlenecks, trade restrictions, and operational disruptions before they impact Neopentyl Glycol markets.

Access the Price Watch™ GIO Tracker

Neopentyl Glycol Price Trend Q2 2026

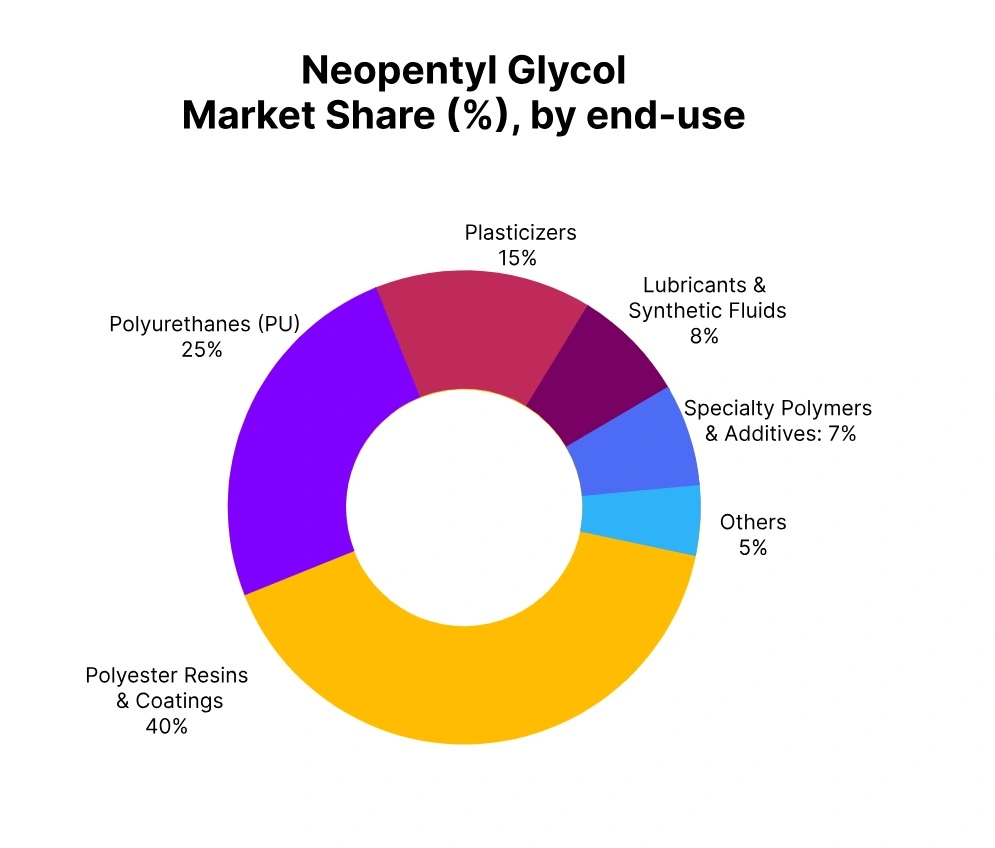

During Q2 2026, Neopentyl Glycol prices in the global market remained on a firm upward trajectory, supported by persistent geopolitical tensions between Iran and the USA, which disrupted trade flows and tightened raw material availability across key regions. Rising formaldehyde feedstock prices increased production costs, while healthy demand from downstream powder coatings, automotive coatings, construction, resins, lubricants, and plasticizer industries further reinforced market sentiment.

Disciplined supplier pricing, balanced inventories, and steady procurement activity sustained higher offers throughout the quarter. The Neopentyl Glycol price trend in the global market reflected resilient supply-demand fundamentals despite ongoing logistical challenges.

The Neopentyl Glycol Price Chart highlighted the sustained upward movement, while the Neopentyl Glycol Price Index indicated firm market conditions driven by elevated feedstock costs, constrained supply, and consistent downstream demand during Q2 2026.

Indonesia: Neopentyl Glycol Imported prices CIF Jakarta (South Korea), Indonesia, Grade- Flakes (99.2% min purity)

During Q2 2026, Neopentyl Glycol prices in Indonesia remained on a firm upward trajectory, closely following the strengthening South Korea FOB trend, which supported higher import offers and reinforced positive market sentiment. Rising formaldehyde feedstock prices increased upstream production costs, while healthy demand from downstream powder coatings, automotive coatings, construction, resins, lubricants, and plasticizer industries sustained steady procurement activity.

Disciplined supplier pricing, balanced import availability, and consistent trading further supported the market through most of the quarter. However, in June 2026, Neopentyl Glycol prices in Indonesia declined by around 3% as supply availability improved, formaldehyde feedstock prices softened, and buyers adopted cautious procurement strategies.

The Neopentyl Glycol price trend in Indonesia reflected this late-quarter correction, while the Neopentyl Glycol Price Chart and Neopentyl Glycol Price Index indicated easing market conditions toward the end of Q2 2026.

Brazil: Neopentyl Glycol Imported prices CIF Santos (China), Brazil, Grade- Flakes (99.5% min purity)

During Q2 2026, Neopentyl Glycol prices in Brazil remained on a firm upward trajectory, closely following the strengthening China FOB trend, which supported higher import offers and reinforced positive market sentiment. Rising formaldehyde feedstock prices increased upstream production costs, while healthy demand from downstream powder coatings, automotive coatings, construction, resins, lubricants, and plasticizer industries sustained steady procurement activity.

Disciplined supplier pricing, balanced import availability, and consistent trading further supported the market through most of the quarter. However, in June 2026, Neopentyl Glycol prices in Brazil declined by around 0.3% as supply availability improved, formaldehyde feedstock prices softened, and buyers adopted cautious procurement strategies.

The Neopentyl Glycol price trend in Brazil reflected this late-quarter correction, while the Neopentyl Glycol Price Chart and Neopentyl Glycol Price Index indicated easing market conditions toward the end of Q2 2026.

Turkey: Neopentyl Glycol Imported prices CIF Mersin (South Korea), Turkey, Grade- Flakes (99.2% min purity)

During Q2 2026, Neopentyl Glycol prices in Turkey remained on a firm upward trajectory, closely following the strengthening South Korea FOB trend, which supported higher import offers and reinforced positive market sentiment. Rising formaldehyde feedstock prices increased upstream production costs, while healthy demand from downstream powder coatings, automotive coatings, construction, resins, lubricants, and plasticizer industries sustained steady procurement activity.

Disciplined supplier pricing, balanced import availability, and consistent trading further supported the market through most of the quarter. However, in June 2026, Neopentyl Glycol prices in Turkey declined by around 3.5% as supply availability improved, formaldehyde feedstock prices softened, and buyers adopted cautious procurement strategies.

The Neopentyl Glycol price trend in Turkey reflected this late-quarter correction, while the Neopentyl Glycol Price Chart and Neopentyl Glycol Price Index indicated easing market conditions toward the end of Q2 2026.

China: Neopentyl Glycol Export prices FOB Shanghai, China, Grade- Flakes (99.5% min purity)

In Q2 2026, Neopentyl Glycol prices in China stayed stable for the majority of the quarter, bolstered by geopolitical tensions from the Iran–USA conflict, which disturbed global trade routes and enhanced optimistic market sentiment. Increasing prices for formaldehyde feedstock raised production costs, yet strong demand from downstream sectors like powder coatings, automotive coatings, construction, resins, lubricants, and plasticizer industries maintained consistent purchasing.

Disciplined supplier pricing and well-balanced inventories continued to bolster the market in the initial phase of the quarter. In June 2026, Neopentyl Glycol prices in China fell by 5% due to better supply conditions, a decrease in formaldehyde feedstock prices, and improved product availability, which prompted cautious purchasing behavior.

The Neopentyl Glycol price trend in China mirrored this adjustment, whereas the Neopentyl Glycol Price Chart and Neopentyl Glycol Price Index showed softer market conditions as Q2 2026 concluded.

South Korea: Neopentyl Glycol Export prices FOB Busan, South Korea, Grade- Flakes (99.2% min purity)

In Q2 2026, Neopentyl Glycol prices in South Korea remained stable for most of the quarter, bolstered by geopolitical tensions from the Iran–USA conflict, which hindered regional trade and enhanced export market sentiment. Increasing formaldehyde feedstock prices raised production expenses, whereas strong demand from downstream powder coatings, automotive coatings, construction, resins, lubricants, and plasticizer sectors maintained consistent purchasing.

Supplier pricing discipline, balanced stock levels, and strong export inquiries strengthened the market in the early part of the quarter. In June 2026, Neopentyl Glycol prices in South Korea dropped by 3.5% due to improved supply conditions, lower formaldehyde feedstock prices, and increased product availability, leading to more cautious purchasing.

The Neopentyl Glycol price trend in South Korea mirrored this adjustment, as the Neopentyl Glycol Price Chart and Neopentyl Glycol Price Index showed a softening of market conditions as Q2 2026 came to a close.

USA: Neopentyl Glycol Export prices FOB Houston, USA, Grade- Flakes (99% min purity)

In Q2 2026, Neopentyl Glycol prices in the USA continued to rise steadily, bolstered by geopolitical tensions stemming from the Iran–USA conflict, which affected supply chains and restricted material availability along essential trade routes. Increasing formaldehyde feedstock prices raised production expenses, while strong demand from downstream powder coatings, automotive coatings, construction, resins, lubricants, and plasticizer sectors bolstered favorable market sentiment.

Regulated supplier pricing, balanced stock levels, and consistent purchasing actions also bolstered the market during the quarter. In June 2026, Neopentyl Glycol prices in the USA rose by 3.9% due to high feedstock costs and ongoing supply issues bolstering supplier offers.

The Neopentyl Glycol price trend in the USA has been bullish during Q2 2026, with the Neopentyl Glycol Price Chart and Neopentyl Glycol Price Index demonstrating strong market conditions due to increased production expenses, limited supply, and robust downstream demand.

India: Neopentyl Glycol Imported prices CIF JNPT (South Korea), India, Grade- Flakes (99.2% min purity)

In Q2 2026, Neopentyl Glycol prices in India maintained a strong upward trend, closely aligning with the rising FOB trend in South Korea, which bolstered increased import offers and enhanced optimistic market sentiment. Increasing formaldehyde feedstock prices drove up upstream production costs, while strong demand from downstream sectors like powder coatings, automotive coatings, construction, resins, lubricants, and plasticizers maintained consistent procurement activity.

Controlled supplier pricing, steady import availability, and robust trading activity additionally bolstered the market during the quarter. In June 2026, Neopentyl Glycol prices in India rose by 3.9% as robust FOB offers from South Korea and high feedstock expenses prompted suppliers to keep higher rates. The Neopentyl Glycol price trend in India is optimistic throughout Q2 2026.

The Neopentyl Glycol Price Chart showed a continued upward trend, whereas the Neopentyl Glycol Price Index revealed stable market conditions influenced by robust South Korea FOB trends, increased feedstock expenses, and strong downstream demand.