Price Watch™ provides real-time price assessments and price forecasts for Sodium percarbonate across top trading regions:

| Sodium percarbonate Regional Coverage | Sodium percarbonate Grade and Country Coverage | Sodium percarbonate Pricing Data Coverage Explanation |

| Asia Sodium percarbonate Pricing Analysis | Sodium percarbonate Coated (Active Oxygen_min.13%) FOB at Shanghai, China | Weekly Price Update on Sodium percarbonate Real-Time Export Prices from Shanghai, China to Global Market |

| Sodium percarbonate Coated (Active Oxygen_min.13%) CIF Prices at JNPT, India, Importing from China | Weekly Price Update on Sodium percarbonate Real-Time Import Prices at JNPT, India from China | |

| Sodium percarbonate Coated (Active Oxygen_min.13%) CIF Prices at Busan, South Korea, Importing from China | Weekly Price Update on Sodium percarbonate Real-Time Import Prices at Busan, South Korea from China | |

| Sodium percarbonate Coated (Active Oxygen_min.13%) CIF Prices at Klang, Malaysia, Importing from China | Weekly Price Update on Sodium percarbonate Real-Time Import Prices at Klang, Malaysia from China | |

| Sodium percarbonate Coated (Active Oxygen_min.13%) CIF Prices at Jakarta, Indonesia, Importing from China | Weekly Price Update on Sodium percarbonate Real-Time Import Prices at Jakarta, Indonesia from China | |

| Sodium percarbonate Coated (Active Oxygen_min.13%) CIF Prices at Haiphong, Vietnam, Importing from China | Weekly Price Update on Sodium percarbonate Real-Time Import Prices at Haiphong, Vietnam from China | |

| Sodium percarbonate Coated (Active Oxygen_min.13%) CIF Prices at Tokyo, Japan, Importing from China | Weekly Price Update on Sodium percarbonate Real-Time Import Prices at Tokyo, Japan from China |

Note: In assessments structured as CIF [Importing Port] (Exporting Country), the country mentioned in brackets indicates the primary origin of supply (exporting country), while the named port refers to the destination port in the importing country. Other Incoterms (FOB, FD, EXW, etc.) should be interpreted in accordance with standard international trade definitions.

Sodium Percarbonate Price Trend Q1 2026

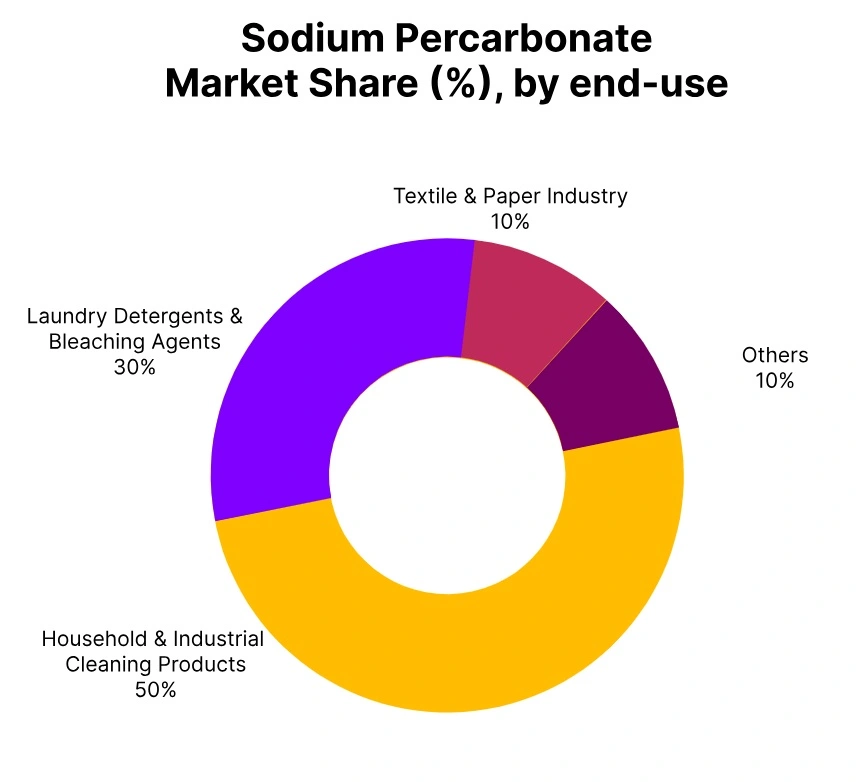

During the quarter ending March 2026, there has been significant price increments in the world market for sodium percarbonate owing to consistent demand from sectors like household cleaning agents, laundry detergents, and textiles.

There are considerable price increments in Asian markets including China, India, Malaysia, and South Korea. The price increments in these markets are due to the high level of demand for sodium percarbonate and its use in manufacturing industries. Some of the geopolitical factors that influenced the market included the Iran-Israel conflict.

This caused an increase in crude oil prices, which affected the cost of production. Consequently, there is price increments in many regions amid continued cautious purchasing patterns. On the other hand, price increments in some markets such as Japan and Vietnam is not so extensive as they are influenced by modest demand increments.

China: Sodium percarbonate Export prices FOB Shanghai, China; Grade- Coated (Active Oxygen_min.13%)

For the first quarter of 2026, the Sodium Percarbonate price in China has gone up by 5% as compared to the previous quarter because of stable consumption in major industries like cleaning agents, textile, and laundry.

The Sodium Percarbonate price trend in China has shown a stable yet firm situation due to continued consumption and manufacturing activities. There has been little to no problem in terms of supply; however, purchasing practices on the part of buyers have been conservative.

In China, Sodium Percarbonate prices in March 2026, they have gone up by 10% from February because of geopolitical instability in the form of tension between Israel and Iran. The Sodium Percarbonate price trend in China has been affected due to rising crude oil prices as the cost of production has been higher and price increase supported. The price trend has been positive due to stable supply and high demand.

Indonesia: Sodium percarbonate Import prices CIF Jakarta, Indonesia; Grade- Coated (Active Oxygen_min.13%)

During the first quarter of 2026, the Sodium Percarbonate price in Indonesia coming from China has gone up by 4% compared to the previous quarter due to consistent demand from industries that rely on this chemical.

The Sodium Percarbonate price trend in Indonesia has been quite favorable, thanks to a robust manufacturing sector, which has maintained healthy production and consumption levels despite cautious procurement practices. In Indonesia, Sodium Percarbonate price in March 2026 has jumped by 10% in comparison to February, following tension between Israel and Iran.

The cost trend of Sodium Percarbonate in Indonesia has been impacted by the surge in crude oil prices, making manufacturing costly and leading to price hikes. The market trend has been favorable since there has been high demand and high manufacturing costs, which have outweighed low restocking efforts, while the supply trend has been stable.

Malaysia: Sodium percarbonate Import prices CIF Klang, Malaysia; Grade- Coated (Active Oxygen_min.13%)

The Sodium Percarbonate price in Malaysia, sourced from China, has appreciated by 5% in Q1 2026 due to constant demand from important markets such as textiles and cleaning applications. The Sodium Percarbonate price trend in Malaysia has been positive on the backdrop of constant consumption and a strong manufacturing base that has helped keep prices up despite cautious purchasing behavior from consumers.

In Malaysia, Sodium Percarbonate prices in March 2026 have increased by 9% compared to February on account of geopolitical tensions such as those between Iran and Israel. The trend in Malaysia regarding the prices of Sodium Percarbonate has been impacted by the increase in crude oil prices, making the production process more expensive and thereby allowing for modest price increments.

India: Sodium percarbonate Import prices CIF Nhava Sheva, India; Grade- Coated (Active Oxygen_min.13%)

In Q1 2026, sodium percarbonate prices in India (importing from China) increased by 8%, driven by strong demand from key sectors such as textiles and cleaning products. Industrial consumption remained steady, despite cautious procurement strategies, contributing to the upward price trend.

In India, sodium percarbonate prices in March 2026 surged by 15%, primarily influenced by rising crude oil prices due to geopolitical tensions, particularly the Iran-Israel conflict. This resulted in increased production costs.

The sodium percarbonate price trend in India reflected these global factors, with a significant price increase driven by supply chain disruptions and continued demand. The overall market in India saw a positive price movement, with steady industrial activity and geopolitical factors playing a key role in shaping the price dynamics.

South Korea: Sodium percarbonate Import prices CIF Busan, South Korea; Grade- Coated (Active Oxygen_min.13%)

In Q1 2026, sodium percarbonate prices in South Korea (importing from China) increased by 4%, supported by steady demand from key industries such as cleaning products and textiles. The market is buoyed by stable industrial activity, although cautious buying behavior continued to limit large-scale purchases.

In South Korea, sodium percarbonate prices in March 2026 rose by 10%, influenced by the geopolitical tensions, particularly the Iran-Israel conflict, which led to higher crude oil prices and impacted production costs. The sodium percarbonate price trend in South Korea mirrored these factors, reflecting stronger demand and higher raw material costs, with supply conditions remaining stable.

Vietnam: Sodium percarbonate Import prices CIF Haiphong, Vietnam; Grade- Coated (Active Oxygen_min.13%)

According to Price-Watch™, In Q1 2026, sodium percarbonate prices in Vietnam (importing from China) increased by 4%, driven by steady demand from sectors like cleaning products and textiles. Despite stable supply conditions, cautious buying behavior led to a moderate price rise.

In Vietnam, sodium percarbonate prices in March 2026 rose by 10%, influenced by geopolitical tensions, particularly the Iran-Israel conflict, which resulted in higher crude oil prices and impacted production costs.

The sodium percarbonate price trend in Vietnam mirrored similar trends in other Southeast Asian markets, with a combination of stable demand and higher raw material costs contributing to the price increases.

Japan: Sodium percarbonate Import prices CIF Tokyo, Japan; Grade- Coated (Active Oxygen_min.13%)

In Q1 2026, sodium percarbonate (imported from China) price increased 4% in Japan due to good steady demand from major sectors such as cleaning and textiles. Industrial activity has been stable, but buying cautiousness produced dampened procurement.

During March 2026 in Japan sodium percarbonate prices also increased 7%, due to geopolitical tensions, primarily the Iran-Israel war. Higher crude oil prices, which impacted production costs, contributed to the increase in price.

Sodium percarbonate price trends in Japan reflected the global trend with priced increasing due to pressure from production cost increases and stable demand. While there have been geopolitical challenges to the market, steady demand from the marketplace resulted in continuing price increase pressure.