Price Watch™ provides real-time price assessments and price forecasts for Vinyl Acetate Monomer (VAM) across top trading regions:

| Vinyl Acetate Monomer (VAM) Regional Coverage | Vinyl Acetate Monomer (VAM) Grade and Country Coverage | Vinyl Acetate Monomer (VAM) Pricing Data Coverage Explanation |

| Asia Vinyl Acetate Monomer (VAM) Pricing Analysis | Vinyl Acetate Monomer (VAM) Industrial Grade (99.9%) FOB Prices at Port of Singapore, Singapore | Weekly Price Update on Vinyl Acetate Monomer (VAM) Real-Time Export Prices from Port of Singapore, Singapore to Global Markets |

| Vinyl Acetate Monomer (VAM) Industrial Grade (99.9%) FOB Prices at Busan Port, South Korea | Weekly Price Update on Vinyl Acetate Monomer (VAM) Real-Time Export Prices from Busan Port, South Korea to Global Markets | |

| Vinyl Acetate Monomer (VAM) Industrial Grade (99.9%) FOB Prices at Shanghai Port, China | Weekly Price Update on Vinyl Acetate Monomer (VAM) Real-Time Export Prices from Shanghai Port, China to Global Markets | |

| North America Vinyl Acetate Monomer (VAM) Pricing Analysis | Vinyl Acetate Monomer (VAM) Industrial Grade (99.9%) FOB Prices at Los Angeles Port, USA | Weekly Price Update on Vinyl Acetate Monomer (VAM) Real-Time Export Prices from Los Angeles Port, USA to Global Markets |

| Vinyl Acetate Monomer (VAM) Industrial Grade (99.9%) CIF Prices at Manzanillo Port, Mexico, Importing from USA | Weekly Price Update on Vinyl Acetate Monomer (VAM) Real-Time Import Prices at Manzanillo Port, Mexico from USA | |

| Middle East Vinyl Acetate Monomer (VAM) Pricing Analysis | Vinyl Acetate Monomer (VAM) Industrial Grade (99.9%) FOB Prices at Jubail Port, Saudi Arabia | Weekly Price Update on Vinyl Acetate Monomer (VAM) Real-Time Export Prices from Jubail Port, Saudi Arabia to Global Markets |

Note: In assessments structured as CIF [Importing Port] (Exporting Country), the country mentioned in brackets indicates the primary origin of supply (exporting country), while the named port refers to the destination port in the importing country. Other Incoterms (FOB, FD, EXW, etc.) should be interpreted in accordance with standard international trade definitions.

Vinyl Acetate Monomer Price Trend Q1 2026

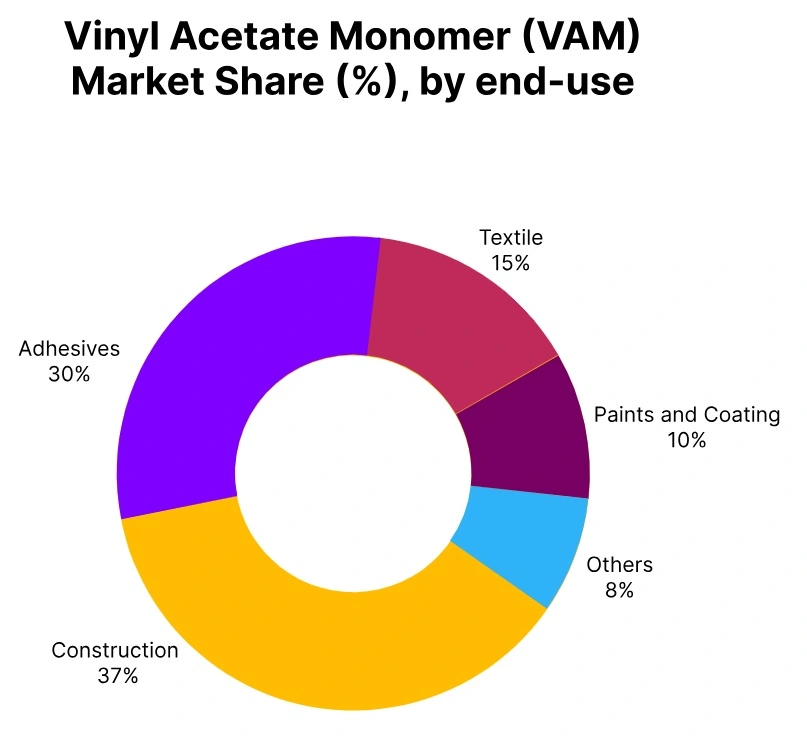

The vinyl acetate monomer price trend has remained on the increase in all major countries in the world during the first quarter of 2026. This has been caused by the high level of demand for products from the sectors such as constructions, adhesives, textiles, paints, and coatings from various countries including China, India, USA, Saudi Arabia, South Korea, Singapore, and Mexico.

The reasons behind market instability include factors like limited supply, high feedstock prices, as well as logistics. Other issues related to export and geopolitics concerning the conflict between Iran-Israel-America war and disruption close to the strait of Hormuz have also influenced market stability.

These have been monitored and considered in influencing the market prices. The global market has therefore had a trend characterized by tight supply, demand, and consumption.

China: Vinyl Acetate Monomer Export Prices FOB Shanghai, China; Grade- (99.9% min) Industrial

During the first quarter of 2026, the Vinyl Acetate Monomer price in China has seen an impressive growth of 22.95% relative to the previous quarter due to growing demand in the fields of construction, adhesive, textiles, paint, and coating industries amid supply chain challenges. The vinyl acetate monomer price trend in China have been quite bullish owing to low domestic output volumes and promising export prospects.

Regarding the month-over-month price changes, it can be noted that in China Vinyl Acetate Monomer price in March 2026 grew by a whopping 43%, due to rising feedstock prices and logistics challenges.

In addition to that, geopolitical conflicts (Iran-Israel-America war) have caused shipping disruptions around the Strait of Hormuz and, hence, influenced the cost of transportation and energy resources. The export and political situation are being actively monitored by market players in anticipation of the next quarter developments.

India: Vinyl Acetate Monomer Import prices CIF JNPT, India; Grade- (99.9% min) Industrial Grade

According to Price-Watch™ , in Q1 2026, Vinyl Acetate Monomer price in India has risen 39.75% from the preceding quarter, owing to sluggish shipments into India from Saudi Arabia and good regional demand from the construction, adhesives, textile, paints, and coatings industries. Vinyl acetate monomer price trend in India remained strong on the back of high raw material prices, low stocks, and high end-use in coatings production.

On a month-to-month basis, in India Vinyl Acetate Monomer in March 2026 has shot up by 73%, as consumption rose and supplies became tighter. There have also been similar developments for the India Ex Kandla, with prices having jumped 51% above their levels from the preceding quarter and 96% above their prices from the preceding month.

These sharp price-increases have been direct reflection of geopolitical uncertainties surrounding the ongoing Iran-Israel-USA war situation coupled with logistical delays close to the Strait of Hormuz.

USA: Vinyl Acetate Monomer Export Prices FOB Los Angeles, USA; Grade- (99.9% min) Industrial Grade

For the first quarter of 2026, there has been a rise of 14% in Vinyl Acetate Monomer price in the United States compared to the last quarter quarter. This has been due to high demand for the product from various sectors such as construction, adhesives, textiles, paints, and coatings sector despite the scarcity of raw materials.

Vinyl acetate monomer price trend in the USA has been quite steady due to consistent export volumes despite uncertain times in the market. Month on month, in the USA Vinyl Acetate Monomer price in March 2026 has risen by 23.8% compared to February 2026.

Geopolitical conflict, mainly between the countries involved in the Iran-Israel war and their association with the United States has affected market expectations. The risk involved with shipping close to the Strait of Hormuz has further raised the price of energy and commodities.

Saudi Arabia: Vinyl Acetate Monomer Export Prices FOB Jubail, Saudi Arabia; Grade- (99.9% min) Industrial Grade

In Q1 2026, the Vinyl Acetate Monomer price in Saudi Arabia has increased by 33.5 % compared to the previous quarter, supported by strong demand from construction, adhesives, textile, paints and coating sectors and ongoing supply constraints in the domestic and export markets. The vinyl acetate monomer price trend in Saudi Arabia has remained robust, driven by higher feedstock costs and limited production flexibility.

Month-over-month, in Saudi Arabia Vinyl Acetate Monomer price in March 2026 surged by 43 % compared to the previous month, reflecting tighter inventories and elevated export demand. Geopolitical tensions involving Israel, the US, and Iran, along with temporary disruptions near the Strait of Hormuz, have further intensified shipping risks and energy prices, supporting firm market pricing throughout the quarter.

South Korea: Vinyl Acetate Monomer Export Prices FOB Busan, South Korea; Grade- (99.9% min) Industrial Grade

In Q1 2026, the Vinyl Acetate Monomer price in South Korea has increased by 24.01 % compared to the previous quarter, supported by strong demand from construction, adhesives, textile, paints and coating industries and constrained domestic production. The Vinyl Acetate Monomer price trend in South Korea has remained firm, reflecting tighter supply and higher raw material costs.

Month-over-month, in South Korea Vinyl Acetate Monomer price in March 2026 has surged by 42 % compared to the previous month, driven by escalating energy prices and logistical challenges. Geopolitical tensions involving Israel, the US, and Iran, along with temporary disruptions near the Strait of Hormuz, have further elevated shipping risks and export costs. Continued monitoring of these factors has guided market expectations for the quarter.

Singapore: Vinyl Acetate Monomer Export Prices FOB Port of Singapore, Singapore; Grade- (99.9% min) Industrial Grade

In Q1 2026, the Vinyl Acetate Monomer price in Singapore has increased by 18.43 % compared to the previous quarter, reflecting sustained demand from construction, adhesives, textile, paints and coating industries and tighter regional supply. The Vinyl Acetate Monomer price trend in Singapore has strengthened due to elevated feedstock costs, logistic bottlenecks, and cautious production adjustments by local exporters.

Month-over-month, In Singapore Vinyl Acetate Monomer price in March 2026 has risen sharply by 43 % compared to the previous month, underpinned by robust export demand and limited inventories.

Market developments have been influenced by geopolitical tensions involving Israel, the US, and Iran, alongside temporary closures near the Strait of Hormuz, which have heightened shipping risks and energy cost pressures, sustaining firm pricing through the quarter.

Mexico: Vinyl Acetate Monomer Import prices CIF Manzanillo, USA; Grade- (99.9% min) Industrial Grade

In Q1 2026, the Vinyl Acetate Monomer price in Mexico has increased by 13.45 % compared to the previous quarter, supported by steady imports from the USA and strong demand from construction, adhesives, textile, paints and coating sectors.

The Vinyl Acetate Monomer price trend in Mexico has remained firm due to higher raw material costs and logistical adjustments affecting imported volumes. Month-over-month, in Mexico Vinyl Acetate Monomer price in March 2026 has risen by 23 % compared to the previous month, reflecting limited supply and robust consumption.

Market dynamics have been influenced by geopolitical tensions involving Israel, the US, and Iran, along with temporary closures near the Strait of Hormuz, which have elevated shipping risks and energy costs, sustaining strong import pricing throughout the quarter.