For most of 2026, acetic anhydride pricing has not been driven by production economics, but by geography. The Strait of Hormuz crisis transformed freight from a background cost into the market’s primary pricing force, pushing effective landed costs for China-origin CIF cargoes up by nearly 33% even as FOB China values themselves remained relatively stable.

What followed has been a rare market distortion where logistics, insurance premiums, and vessel rerouting began reshaping global trade flows faster than supply-demand fundamentals. As ships diverted around the Cape of Good Hope and war-risk costs surged, freight volatility effectively rewrote the pricing structure of the acetic anhydride market.

The chart below captures how FOB China prices evolved between November 2025 and April 2026, culminating in a sharp April spike as the crisis intensified.

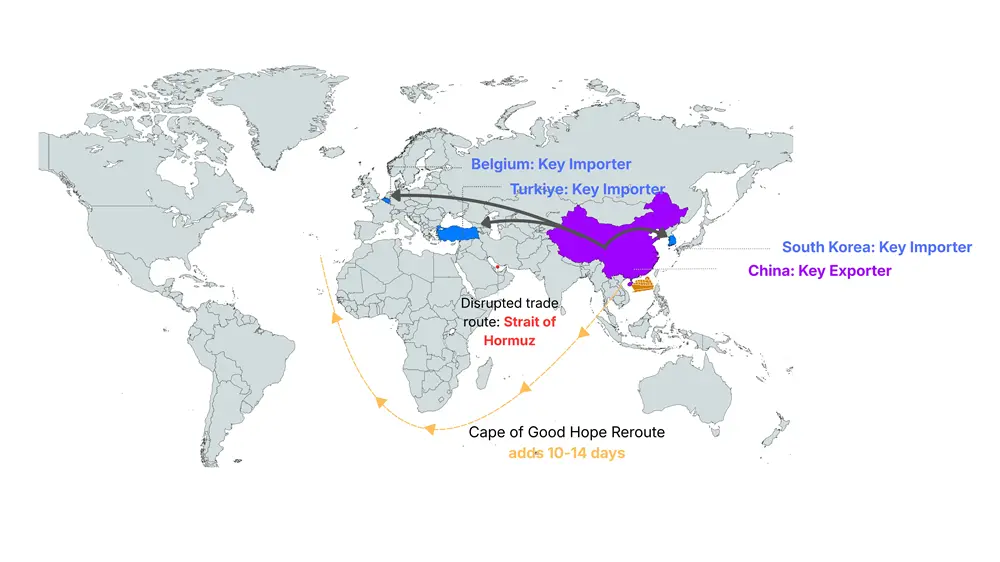

CHINA → CIF TRADE ROUTE MAP

The map below illustrates key acetic anhydride trade lanes from China to CIF destinations in Belgium, South Korea, and Turkey, passing through the Strait of Hormuz. The orange dashed line shows the alternative Cape of Good Hope reroute activated during the 2026 crisis, adding 10–14 days per voyage.

The global acetic anhydride market moved through a prolonged phase of volatility during the second half of 2025. FOB China prices largely remained trapped within a narrow band, bottoming out in August before gradually recovering toward December.

At the core of the imbalance was a persistent tug-of-war between oversupply from China’s coal-to-acetyls producers and uneven downstream buying activity across pharmaceuticals, cellulose acetate, and dye intermediates. Chinese coal-based producers continued to enjoy a structural 15–25% cost advantage over naphtha– and methanol-based competitors, allowing production rates to remain elevated despite weak margins.

At the same time, softer acetic acid feedstock prices, a key input for ketene-route production, further intensified pricing pressure across the chain. The result was a cautious, range-bound market sentiment across major CIF destinations including Belgium, South Korea, and Turkey.

By early 2026, however, the market dynamic shifted dramatically. The escalating US-Israel conflict involving Iran triggered one of the most severe maritime disruptions in recent years, fundamentally altering global freight economics.

Tanker movement through the Strait of Hormuz, a corridor responsible for nearly a quarter of global seaborne oil trade, collapsed by almost 70% within weeks and later approached near standstill conditions. Freight rates from the Far East to North Europe and Mediterranean corridors surged by 31% and 30%, respectively, in barely over a month.

Simultaneously, war-risk insurance premiums quadrupled, adding nearly $250,000 per voyage, while Cape of Good Hope rerouting extended transit times by an additional 10–14 days. Collectively, these pressures drove an estimated 33% increase in effective landed costs for China-origin CIF acetic anhydride cargoes at the April peak, even as underlying FOB China values remained comparatively stable.

Fragile Stability Amid Hormuz Uncertainty

Despite intensifying supply-side disruptions, resilient demand from the pharmaceutical and agrochemical sectors continued to provide a crucial support base for acetic anhydride prices across major CIF markets, limiting the extent of downside pressure.

Yet, the market remains far from stable. With the Strait of Hormuz ceasefire still fragile and maritime risks unresolved, the trajectory of the global acetic anhydride market in 2026 is now increasingly dependent on three decisive factors:

- The pace at which shipping traffic normalizes through the Hormuz corridor

- Operating rates among Chinese producers

- Fluctuations in upstream acetic acid feedstock costs

A meaningful shift in any one of these variables could quickly reshape global supply-demand balances and trigger renewed pricing volatility.

In an environment where geopolitics, freight economics, and feedstock movements can alter market sentiment almost overnight, relying on delayed averages or static forecasts is no longer sufficient.

At Price-Watch™, we deliver real-time acetic anhydride pricing intelligence, freight monitoring, feedstock tracking, and regional trade flow analysis across global markets. From Chinese plant operating trends and CIF arbitrage spreads to upstream acetic acid movements, our intelligence platform enables procurement teams, traders, and manufacturers to react faster, manage exposure more effectively, and identify market turning points before they begin impacting margins.