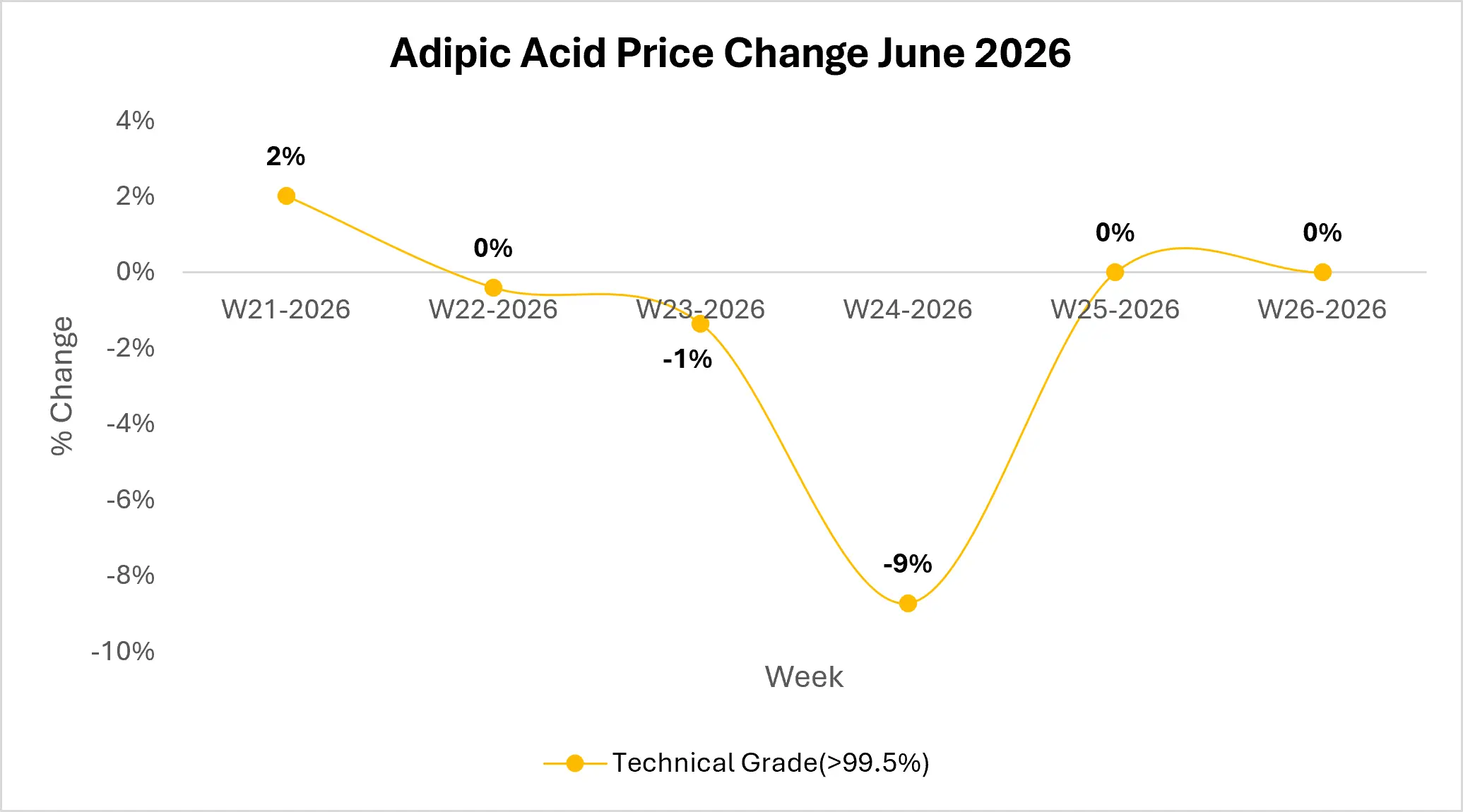

A single week erased nearly a month of pricing stability. After holding largely unchanged for weeks, China’s FOB adipic acid market dropped sharply by 9% in W24, making it the most significant movement in the past six weeks and raising fresh questions about export competitiveness across Asia.

China Adipic Acid Market Faces Export Pressure

The correction will likely reflect a combination of persistent domestic supply pile and weak downstream nylon 6,6 demand rather than a collapse in production costs.

Market monitoring during late June has indicated that Chinese adipic acid producers continued operating while demand from engineering plastics and textile sectors remained sluggish, encouraging exporters to lower offers to maintain overseas sales.

At the same time, plant operating rates across China have largely remained stable, limiting any meaningful supply tightening that could support prices.

Source: Price Watch™ Adipic Acid Prices

South Korea Adipic Acid Market Defies Regional Weakness

South Korea’s adipic acid export market will likely stand out not because of a supply disruption, but because prices will continue rising even as China’s export market weakens.

After a 3% decline in W21, FOB South Korea prices are expected to rebound with consecutive gains of 6% in W23 and 5% in W24, before stabilizing through W25 and W26 of 2026. That divergence could become one of the most closely watched signals in the Asian adipic acid market.

An additional development that could reshape regional trade is the European Union’s definitive anti-dumping duties on Chinese adipic acid, announced in early May.

Over the coming months, Chinese suppliers may increasingly redirect export volumes toward Southeast Asia, India, and other regional destinations, intensifying competition with other Asian exporters that traditionally benefit from stable contractual business.

Adipic Acid Market Outlook

- Chinese exporters may continue prioritizing volume over margins if domestic demand fails to recover.

- South Korean suppliers could face growing pricing pressure as redirected Chinese cargoes compete more aggressively in Asian markets.

The next pricing cycle may depend less on feedstock costs and more on whether downstream nylon producers begin rebuilding inventories before additional Chinese export volumes enter regional markets.

If Chinese operating rates remain elevated while export destinations become increasingly competitive, will South Korean suppliers be forced to adjust pricing strategies to defend market share?

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.