The global coal market in 2025 is navigating one of its most difficult periods in recent history. Forecasts predict an average price of about USD 100 per ton for the year, with a further 5% decline expected in 2026. This dramatic price fall is among the steepest in decades and is driven mainly by easing demand from Asia coupled with persistent global oversupply.

The once-steady surge in global coal demand has lost significant momentum. In 2024, coal consumption increased by less than 80 million metric tons (MMT), just one-third of the growth seen in the previous year.

This slowdown is especially visible in China, which is historically the world’s largest consumer, as it accelerates its renewable energy transition and limits coal-fired power expansion. Europe and North America continue to retreat from coal consumption altogether, hastened by aggressive climate policies and decarbonization efforts.

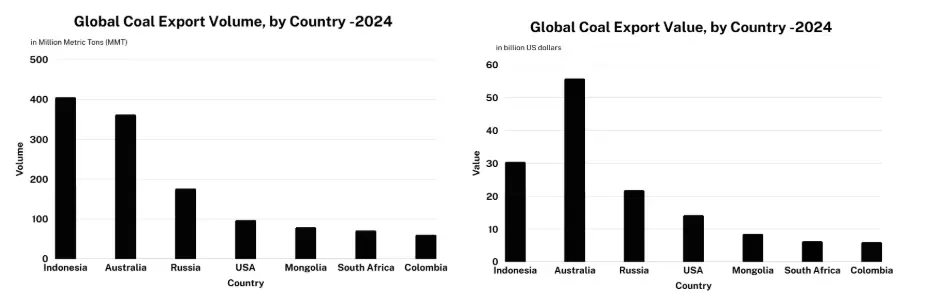

Despite the demand slowdown, global coal production had reached record highs fueled predominantly by Asian countries: China added around 40 MMT, India 80 MMT, and Indonesia approximately 30 MMT. This rise contrasts sharply with sharp production declines in the EU and US, creating a global oversupply that intensifies price pressure.

Asia’s Coal Demand Cools Except India

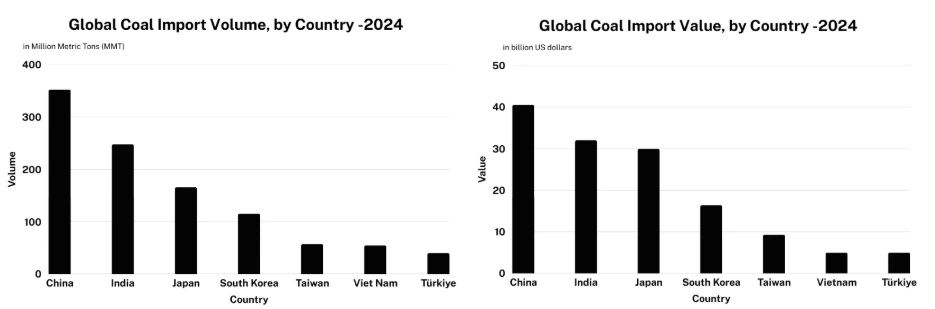

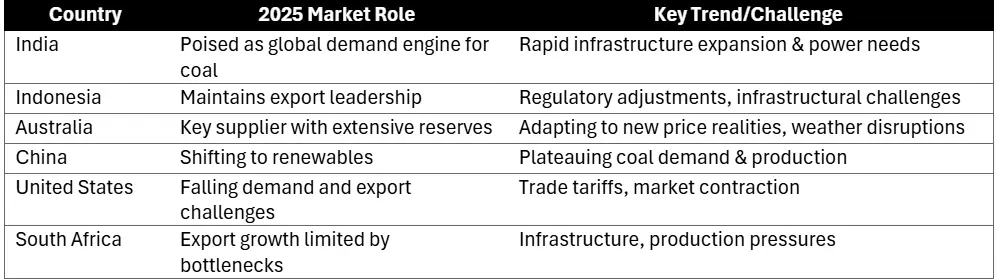

Asia accounts for nearly 80% of global coal consumption, remaining the core driver of market activity. While overall demand growth is slowing, India has emerged as the fastest-growing coal importer, reflecting its continued reliance on coal to meet rising energy needs and industrial demand. Despite a governmental push towards energy self-reliance and expanded domestic production, India’s power sector growth and infrastructure investments continue to fuel strong coal demand. India sources most of its coal imports from Indonesia, Australia, and South Africa, strategically balancing between domestic supply boosts and global purchases.

China, the largest consumer in global coal market, is now experiencing a notable plateau in demand as its energy transition gains pace. Renewables buildouts and sluggish power consumption growth are restraining the need for coal-fired energy generation. Chinese consumption and production are stabilizing or declining, signaling a major shift in global coal dynamics.

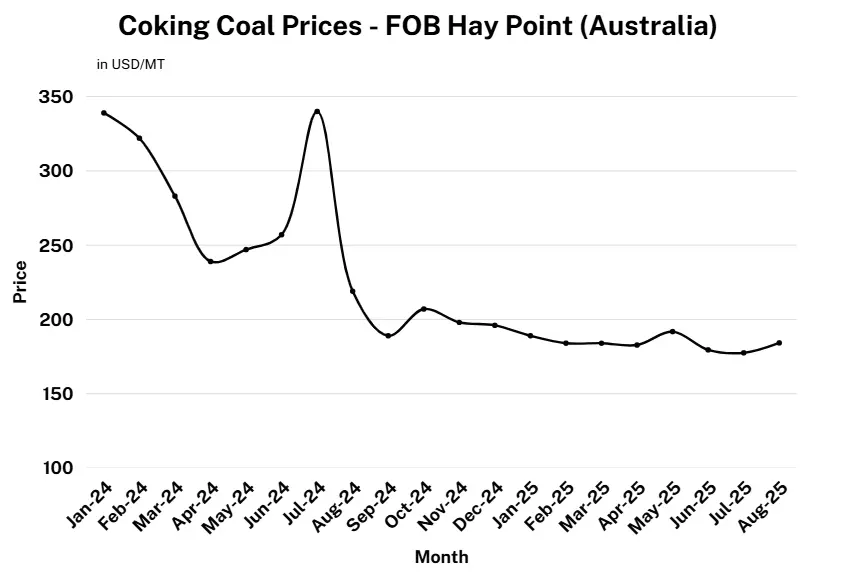

Indonesia and Australia remain the top exporters globally, responsible for major volumes of coal trade. However, Australia’s coal prices, which peaked at over USD 250 per ton during the early pandemic recovery phase, have since adjusted sharply in this market rebalancing. Prices for Australian coal have declined alongside global trends due to excess supply and moderated Chinese demand, though they remain a key price benchmark for global thermal coal markets.

Geopolitical Tensions and Logistics Challenges in Coal Trade

Coal market volatility increased in 2025, fueled by multiple disruptions in key supply regions. Indonesia has seen export volumes fluctuate and is currently grappling with infrastructure bottlenecks and regulatory shifts including restrictions on coal exports to conserve domestic resources.

Australia’s coal sector, while stable in production, continues to face challenges due to freight disruptions and geopolitical tensions.

In South Africa, rail bottlenecks and port congestions have sporadically constrained coal exports, briefly supporting prices during localized supply squeezes.

June 2025 witnessed a price surge on fears of supply disruptions, although these gains quickly faded as global fundamentals reasserted themselves. The U.S.-China tariff measures, while limiting trade flows from American coal producers, have contributed to market uncertainty and pushed buyers towards alternative suppliers in Asia and Africa.

Shifting Tides in Global Coal Trade

Across the world, coal exports reached new heights in 2024 primarily due to strong Asian import demand, despite the oversupply environment. Australia, Indonesia, and Mongolia continued to ramp up shipments, benefitting from their large, low-cost reserves and well-developed infrastructure. Conversely, traditional exporters such as South Africa and the US saw production declines amidst infrastructural limitations, regulatory challenges, as well as diminished international competitiveness.

Coal markets in North America and Europe continue to be in freefall, driven by strong government incentives for renewable energy adoption and strict climate regulations. This structural demand erosion contrasts starkly with Asia’s persistence, although slowing consumption growth, highlighting global market regionalization.

India’s coal imports dropped by 7.9% in FY 2024-25 to 243.3 MMT as government policies prioritized domestic production and aimed to reduce import dependence. Furthermore, coal imports remain significant due to gaps in domestic coking and high-grade thermal coal supplies. In March 2025, monthly imports spiked more than 25% month-on-month to 23.2 MMT fueled by a significant recovery in non-coking coal and anthracite shipments as coal prices dipped, and power plants replenished stocks ahead of the summer demand peak.

Duty, Taxation, and Policy Reforms

On September 3, 2025, India’s Ministry of Finance announced a revision to the tax regime on coal, increasing the Goods and Services Tax (GST) from 5% to 18%. This change comes alongside the elimination of the INR 400/metric ton (approx. USD 4.54/mt) compensation cess, which was previously levied in addition to GST.

According to the ministry, the GST Council has recommended merging the cess into the revised GST rate, stating that “there is no additional burden” on consumers. Hence, the net tax burden on domestic coal has reduced, even though the GST alone is higher, because the fixed cess was relatively high and non-creditable by businesses. However, these reforms will be applicable from 25 September 2025 onwards.

The Indian government’s reform initiatives are reshaping the sector. Open commercial coal mining, 100% foreign direct investment (FDI) in mining, and expedited environmental clearances aim to boost domestic production and reduce import dependence. Up to 50% of output from captive mines is now permitted for commercial sale, encouraging private sector investment and innovation.

Tariffs and trade barriers continue to shape global coal flows. Ongoing U.S.-China trade tensions have placed American coal exports under pressure, forcing a shift in demand toward alternative suppliers. Meanwhile, infrastructure challenges including rail disruptions in South Africa and port congestion in Indonesia and Australia are adding further uncertainty to supply chains and driving price volatility in global markets.

Supply-Demand Dynamics: Oversupply Meets Slow Growth

The coal supply-demand balance in 2025 is characterized by lingering oversupply and moderated growth. While Asian nations continue to drive both production and consumption, the pace of demand growth is slowing overall. China’s rapid renewable energy expansion and weak power demand keep growth subdued, while India’s coal demand surges but is partly offset by a stronger domestic production push.

This oversupply environment, driven by record production from key miners and exporters, fuels price sensitivity to geopolitical events and weather disruptions. Although increased supply flexibility from major exporters like Indonesia and Australia tempers volatility, market fundamentals favor a continued softer pricing environment.

Coal’s Waning Yet Persistent Role

While coal’s share in the global power mix is shrinking rapidly across developed economies committed to decarbonization, its role remains foundational in Asia especially in India. Here, coal continues to power growth, anchored by its affordability, energy security benefits, and the gradual pace of renewable expansion. Despite ambitious climate targets and evolving policies, coal is far from vanishing; instead, it persists as the backbone of energy systems navigating complex transitions.

Geopolitical tensions, extreme weather events, and uneven progress in clean energy deployment are fueling ongoing price volatility and supply uncertainties. Through this decade, coal will remain a critical, if contested, player as Asia balances the urgent demands of economic growth with the imperative for a greener future.

Sources: –

https://coal.nic.in/sites/default/files/2025-05/PIB2131632.pdf

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2163555

https://www.trademap.org/

https://asian-power.com/news/no-major-shift-seen-global-coal-demand-in-2025-2026

What’s driving coal’s price decline in 2025?

https://discoveryalert.com.au/news/coal-resilience-2024-global-consumption-record/

https://worldpopulationreview.com/country-rankings/coal-consumption-by-country

https://www.worldcoal.com/