Strait of Hormuz shipping disruptions, surging styrene monomer costs, and elevated freight rates are driving a broad-based upward repricing of Expanded Polystyrene across Asia, Europe, and North America, with global EPS markets expected to fluctuate within a 5–6% range in the coming months

Strait of Hormuz tensions are increasingly influencing global EPS pricing trends, as disruptions in Gulf shipping routes are impacting feedstock flows and logistics. With crude oil prices rising sharply, styrene monomer costs have increased significantly, pushing up EPS production costs across all major regions. As a result, suppliers are aligning their offers with higher replacement-cost economics, creating a global upward pricing trend.

How Middle East Producers Are Managing Supply Disruption

In the Middle East, shipping constraints and logistical uncertainties continue to affect export movements of petrochemical products, including styrene and its derivatives. While some producers are facing delays due to restricted routes, others are actively rerouting cargoes to maintain supply continuity. Despite these challenges, overall production levels remain relatively stable, preventing severe supply shortages but still contributing to tighter availability in export markets.

Why Asian EPS Markets Are Tightening

Across Asia, including China, India, and Southeast Asia, tightening availability of styrene monomer and EPS cargoes is increasing competition among buyers. Export availability has reduced due to supply-side disruptions and higher upstream costs, leading buyers to shift towards contract-based procurement instead of relying on spot markets.

In India, EPS prices rebounded after a brief slowdown, supported by higher import replacement costs and elevated styrene prices due to Suez Canal disruptions from Qatar and Kuwait restricting Styrene supply. Meanwhile, Northeast Asian markets remain cautious amid high prices and uncertain downstream demand.

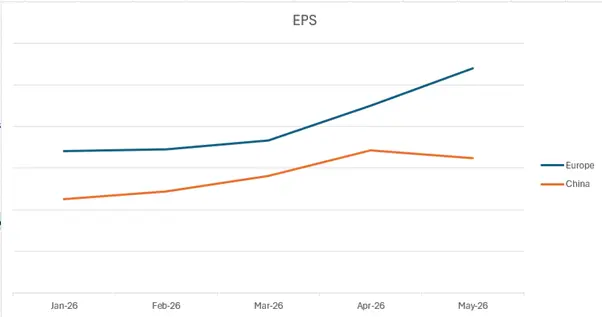

Why Europe and the USA Continue to See Firm Pricing Sentiment

In Europe and the USA, EPS markets are maintaining firm pricing sentiment due to a combination of higher feedstock costs, elevated freight rates, and dependency on imported material for certain grades. Concerns over supply disruptions linked to the Middle East are further supporting price levels, as buyers’ factor in potential risks in global supply chains.

What Rising Costs Mean for the EPS Value Chain

Increasing styrene monomer costs, higher crude-linked feedstock prices, and rising freight expenses are significantly impacting the overall EPS value chain. Manufacturers in packaging, insulation, and construction sectors are facing higher procurement costs, while also dealing with supply uncertainty and longer lead times. This is raising operational risks and reducing margin flexibility across downstream industries.

Source: Price-Watch™

EPS Market Outlook

The global EPS market is expected to fluctuate within a range of around 5–6% in the coming months, influenced by elevated feedstock costs, ongoing shipping disruptions, and tightening spot availability. Market direction will largely depend on crude oil trends, stability in Middle East supply routes, and styrene production dynamics. Growing reliance on long-term contracts, replacement-cost pricing, and continued volatility in logistics and upstream markets are expected to keep procurement risks elevated, with EPS markets across Asia, Europe, the USA, and the Middle East remaining highly sensitive to any supply chain or energy market disruptions.

At Price-Watch™, we provide real-time Expanded Polystyrene (EPS) pricing intelligence, feedstock tracking, freight monitoring, and regional trade flow analysis across global markets. From upstream styrene monomer and benzene movements to downstream packaging, construction, and insulation demand trends, our platform helps manufacturers, traders, and procurement teams respond faster, manage supply-side risks more effectively, and stay ahead of evolving market dynamics.