Gold came under sustained selling pressure this week, with spot prices settling near $4154 per ounce on Friday down 1.28% on the session and part of a broader correction that has seen the metal shed more than $200 in a matter of days. The decline, while sharp, has been orderly in character, reflecting measured position adjustment rather than distressed liquidation.

Three forces drove the move in combination: a decisive hawkish pivot from the Federal Reserve, softening physical demand signals out of China, and a partial unwinding of the geopolitical risk premium that had kept prices elevated through rising oil markets.

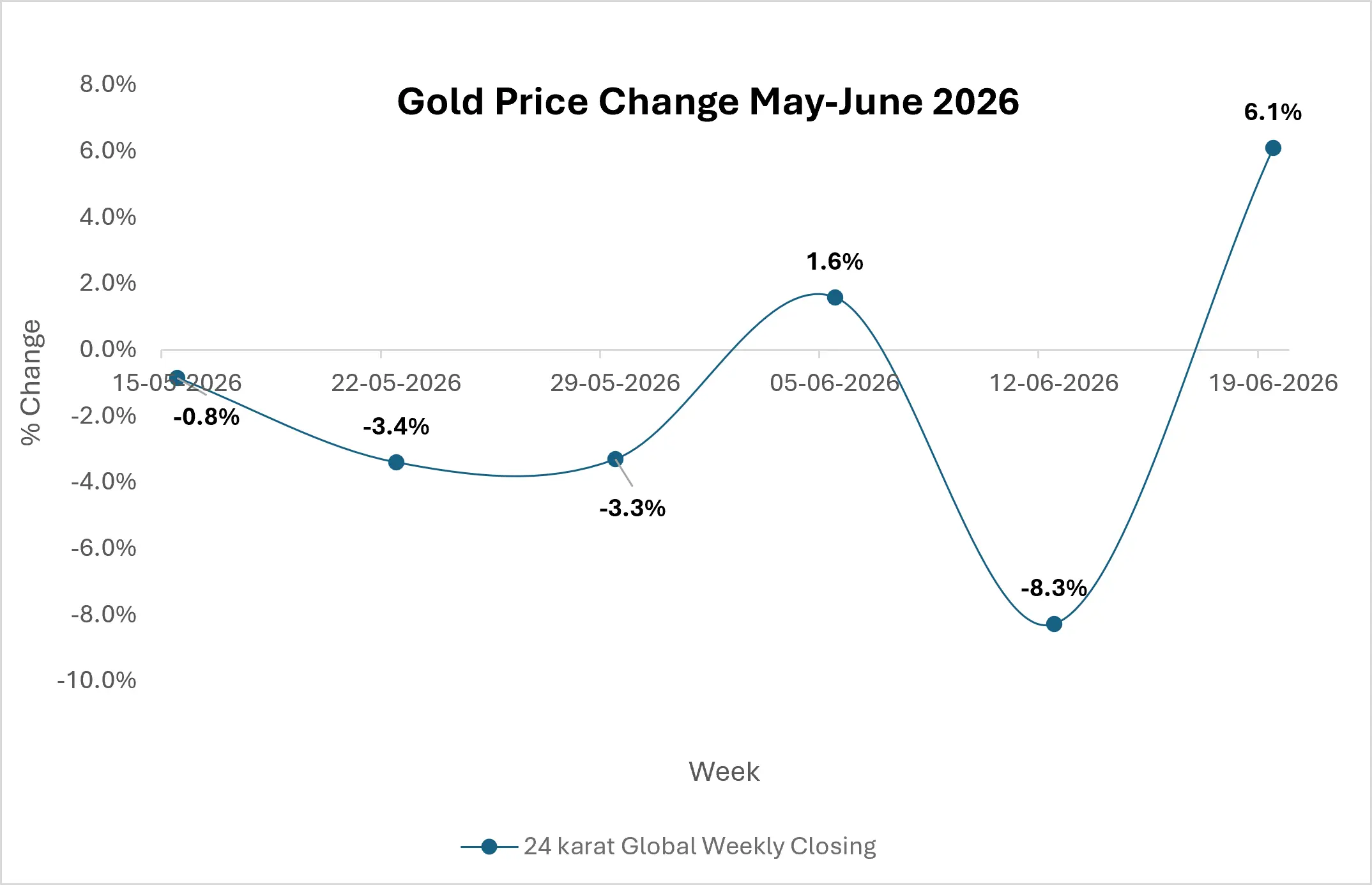

Source: Price Watch™ Gold Prices

Federal Reserve Repricing Reawakens the Opportunity-Cost Debate

The dominant driver of gold’s weakness this week was Wednesday’s Federal Open Market Committee decision and the market reaction that followed. The Fed held its target range steady at 3.50%–3.75%, but the tone of Chair Kevin Warsh’s press conference marked an unambiguous shift in policy bias from a neutral stance toward one where rate increases are back on the table.

Warsh’s emphasis on price stability and his apparent departure from the kind of extensive forward guidance that markets had grown reliant upon drove the hawkish interpretation. The immediate consequence for gold is a reinvigorated opportunity-cost argument: as real yields rise, the relative attractiveness of holding gold diminishes in the eyes of rate-sensitive investors.

However, this framing deserves scrutiny. A more disciplined, credibility-focused Federal Reserve that reduces policy-driven volatility does not automatically translate into a structurally bearish environment for gold. The more consequential long-term variables persistent fiscal deficits, rising government debt, and the inherent limits of monetary policy in addressing structural imbalances remain firmly in place.

Warsh’s inflation focus addresses the cyclical dimension of the problem; it does little to alter America’s deteriorating fiscal trajectory, which is increasingly the more important variable for long-duration gold holders.

Softer Chinese Physical Demand Removes the Spot Price Floor

A quieter but equally significant contributor to this week’s decline was the softening of physical demand signals from China. Premiums in the Chinese physical gold market which had served as a consistent and reliable backstop for spot prices have eased noticeably, indicating that local buyers are stepping back at current price levels.

This matters because physical demand from major consuming markets provides a floor beneath paper-market selling. When that floor compresses, gold becomes more exposed to macro-driven moves, particularly in an environment where rate expectations are already moving against it. The combination of softer Chinese premiums and a hawkish Fed removed two sources of support simultaneously, amplifying the downside move.

Without a clear metal-specific catalyst to replace that physical bid whether in the form of renewed central bank buying, a resurgence of retail demand, or a shift back in the macroeconomic outlook gold faces a period where price action is likely to remain dominated by rate dynamics and positioning flows rather than fundamental demand.

Geopolitical Risk Premium Deflates, But Tensions Remain Unresolved

The third factor weighing on gold this week has been the partial normalization of conditions in the Strait of Hormuz following the U.S.-Iran memorandum. Commercial shipping traffic through the strait has begun to resume, pulling Brent crude back toward $79.50 per barrel and WTI toward approximately $75.85.

Easing oil prices reduce near-term inflation expectations, directly weakening one specific rationale for owning gold as an inflation hedge.

The situation, however, is far from fully resolved. Navigation risks persist, a backlog of stranded vessels remains, and mine-related disruptions continue. The strait is open enough to reduce the immediate supply shock, but not sufficiently clear to erase the geopolitical premium entirely.

For gold, this creates an uncomfortable middle position: the inflationary impulse from energy markets has softened enough to reduce demand from inflation-focused buyers, yet unresolved geopolitical uncertainty prevents safe-haven inflows from disappearing altogether.

The tight correlation between gold and oil prices that emerged at the height of the Hormuz tensions now appears to be in the early stages of breaking down. That is not necessarily a negative development for gold over the medium term.

When gold trades in lockstep with energy prices, it loses its independent character as a portfolio diversifier. A return to gold pricing on its own fundamentals real interest rates, monetary credibility, and fiscal sustainability would restore the clarity that longer-term investors rely upon.

With U.S. cash markets closed Friday for Juneteenth, trading was thin and directional conviction low. The more important test comes next week. June flash manufacturing and services PMI figures are scheduled for Tuesday morning, followed by a dense Thursday data slate encompassing May PCE inflation, weekly jobless claims, final first-quarter GDP, durable goods orders, and personal income and spending figures.

Any upside surprises in inflation or growth data would likely reinforce the Fed’s hawkish posture, extend the dollar’s recent strength, and sustain the pressure on gold. A softer set of readings, particularly on PCE inflation, could begin to temper rate hike expectations and provide the metal with some near-term relief.

Positioning currently leans toward de-risking rather than outright bearish conviction, which means the market retains the capacity to recover quickly if the data narrative shifts.

Gold market Outlook

Gold’s decline this week reflects a specific and identifiable confluence of forces: a Federal Reserve that has pivoted firmly toward a hawkish bias, weakening physical demand from China that has removed the spot price floor, and a partial easing of the energy-market risk premium that had underpinned inflation-hedge buying.

The correction, though sharp at over $200, has been orderly a feature of deliberate position management rather than structural liquidation. The near-term direction will be shaped by incoming economic data and the market’s evolving read on the Fed’s rate path.

The longer-term case for gold, however, continues to rest on foundations that this week’s events have not materially altered: an unsustainable fiscal trajectory, a debt burden that monetary tightening alone cannot resolve, and the enduring role of gold in preserving purchasing power through periods of policy uncertainty.

Those factors do not disappear because the Fed has turned hawkish if anything, they argue for maintaining exposure through volatility.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.