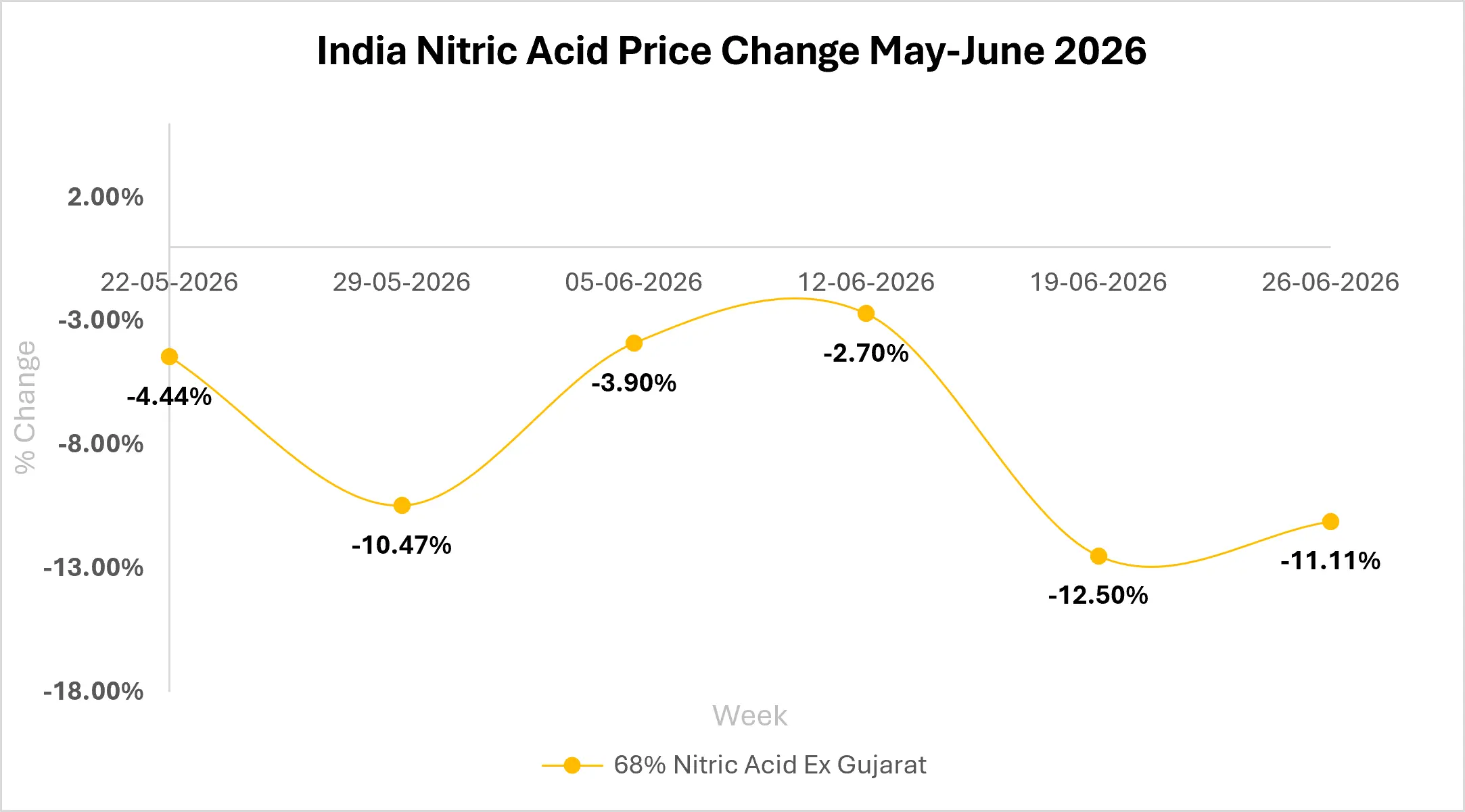

Nitric acid prices in India remained largely stable during the first week of May, offering little indication of the sharp correction that was about to unfold. That stability proved short-lived, as the market entered a sustained downward trend from mid-May onward.

India Nitric Acid Prices Continue to Fall

From 15 May, prices declined every single week without interruption, falling by 5.3%, followed by 4.4%, and then a steep 10.5% drop in the week of 29 May alone.

By 26 June, the market had recorded a cumulative decline of more than 41%, marking nine consecutive weeks of price decreases without a single weekly recovery.

Source: Price Watch™ Nitric Acid Prices

Lower Ammonia Costs Remove Price Support

The May plateau was propped up by an ammonia cost spike tied to US-Israel-Iran tensions earlier in the year. As that conflict de-escalated, global ammonia and energy costs eased, and Indian nitric acid producers, who lean heavily on imported ammonia and concentrated-grade feedstock lost the cost cushion that had kept prices elevated.

The correction did not need a new shock; it simply needed the old one to fade, and the -5.3% and -4.4% weeks that followed were the market re-pricing that absence.

Chinese Imports Intensify Market Competition

With ammonia costs no longer providing support, Chinese exporters returned through late May and June with aggressive, discounted offers on weak and concentrated grade material.

India remains import-dependent for a meaningful share of its nitric acid needs, so every fresh Chinese cargo reset the domestic benchmark lower culminating in the single sharpest weekly fall of the cycle, -12.5% in the week of 19 June.

Sellers who tried to hold their price simply stopped getting enquiries.

A 41% Drop Sounds Like Good News, So Why Are Some Buyers Worse Off?

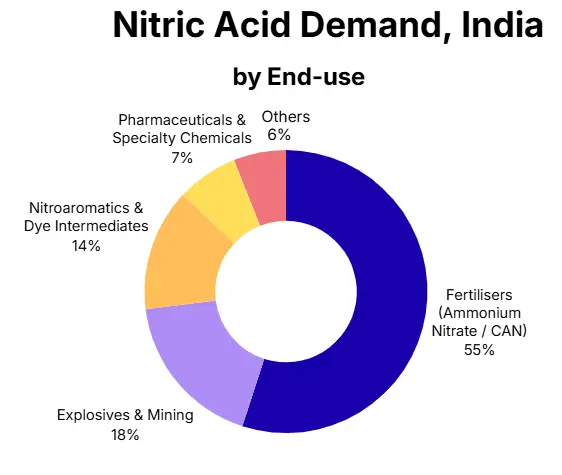

A correction this size does not land evenly. Ammonium nitrate and fertiliser producers who locked in May-level contracts now sit on costly inventory against a far cheaper spot market, a margin squeeze on the buy side, not the sell side.

Explosives and nitroaromatics converters are the clear near-term winners, picking up feedstock at the cheapest relative levels in over two months. Domestic manufacturers face the harder call: match falling Chinese import pricing, or cede volume to protect margin.

Nitric Acid Market Outlook

Over the next one to three months, expect the pace of decline to slow rather than reverse sharply. Chinese export intensity shows no sign of easing, and kharif-linked fertiliser demand has not yet built enough momentum to absorb the current oversupply.

Weekly declines should narrow toward low single digits as the cheapest import offers get absorbed into the market, but a genuine reversal needs either a fresh ammonia or freight disruption, or an early, aggressive restocking cycle, neither of which is visible yet.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.