The global Polyethylene Terephthalate (PET) Resin market has entered one of its most sustained downward cycles in recent years, with bottle-grade resin prices declining for six consecutive weeks across major export hubs including China, South Korea, and Europe.

What began as a correction in crude oil prices has gradually filtered through the polyester value chain, reducing feedstock costs and reinforcing a market already facing abundant supply.

For procurement teams, the significance lies not just in the magnitude of the decline, but in its consistency. With prices softening across multiple regions simultaneously, buyers are reassessing purchasing strategies as market fundamentals increasingly favor consumers over producers.

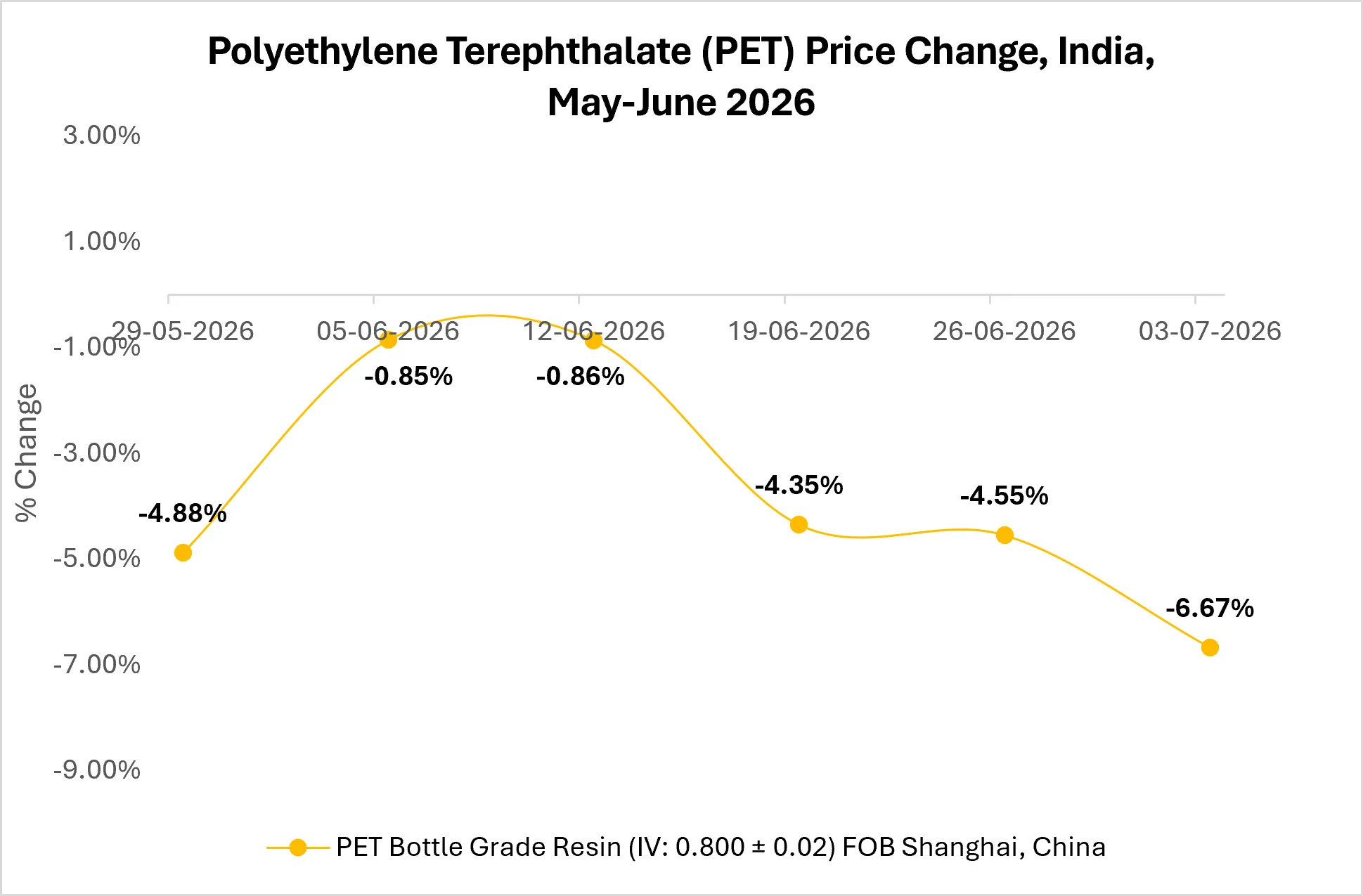

China PET Resin Market Drives Global Pricing

China continues to set the tone for the global PET Resin market. Declining crude oil prices translated into lower Purified Terephthalic Acid (PTA) and Monoethylene Glycol (MEG) costs, reducing production expenses throughout June.

At the same time, expanding production capacity and the restart of previously idle facilities added further supply to an already well-supplied market.

Source: Price Watch™ Polyethylene Terephthalate (PET) Prices

The combination of easing feedstock costs and rising availability resulted in increasingly competitive export offers, with Shanghai recording the sharpest weekly decline among major exporting regions.

Despite the approach of the traditional beverage packaging season, downstream demand has remained insufficient to absorb additional supply, limiting producers’ ability to defend prices.

Global PET Resin Markets Follow China’s Lead

Regional markets have broadly mirrored China’s pricing direction, although at varying speeds. South Korea and Europe have experienced similar downward trends as weaker feedstock costs and subdued demand weighed on market sentiment.

Source: Price Watch™

India has remained comparatively more stable, with domestic demand and currency movements helping moderate the pace of decline. Nevertheless, global pricing continues to exert influence on procurement decisions, particularly as import parity becomes increasingly attractive.

The synchronized decline across key producing regions reflects a market driven by common upstream fundamentals rather than localized supply disruptions.

Feedstock Costs Reshape PET Resin Procurement

The latest correction has been driven primarily by developments in global energy markets. Crude oil prices retreated as geopolitical concerns surrounding the Strait of Hormuz eased, shipping conditions improved, and expectations of higher OPEC+ production reduced fears of supply shortages.

Lower energy prices quickly filtered into PTA and MEG markets, with MEG recording the steepest decline among PET feedstocks. As production costs eased, manufacturers responded with more competitive pricing, reinforcing the downward trend across the polyester value chain.

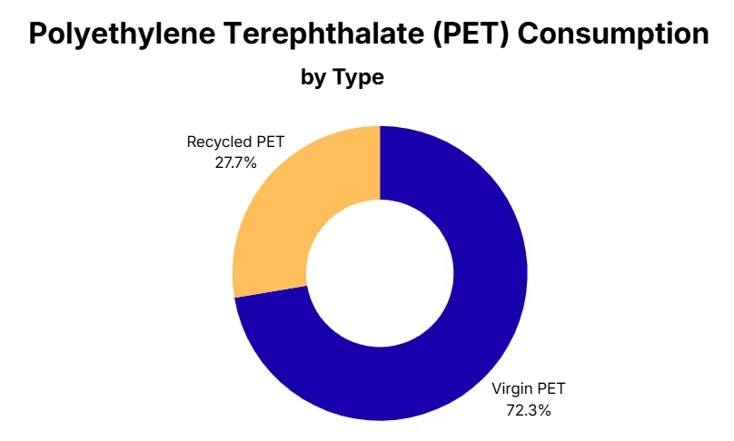

At the same time, virgin PET continues to account for the majority of global packaging demand, meaning declining virgin resin prices are widening the cost advantage over recycled PET and creating new opportunities for procurement teams to review sourcing strategies.

PET Resin Market Outlook

Looking ahead, the near-term outlook remains cautiously bearish. Stable-to-lower crude oil prices, expanding Chinese production capacity, and comfortable supply levels are expected to keep pressure on PET Resin prices through the coming months.

Although seasonal demand from beverage and food packaging could provide some support, it is unlikely to offset the combined impact of abundant supply and lower feedstock costs in the short term.

For buyers, the current market offers favorable procurement conditions, but the key variables remain China’s operating rates, additional capacity additions, PTA and MEG pricing, and future OPEC+ production decisions.

Together, these factors will determine whether the recent correction represents the market’s floor or the beginning of a more prolonged period of softer PET Resin prices.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.