The recent decline in petrochemical prices should not be viewed simply as a correction in crude oil. Instead, it reflects the gradual unwinding of a geopolitical risk premium that dominated global chemical markets during the first half of 2026.

While the Iran–Israel–USA conflict initially disrupted supply chains and inflated logistics costs across the Middle East, the market has since transitioned into a new phase one where procurement strategies, contract negotiations, and inventory management are becoming more influential than geopolitical headlines.

Between March and May 2026, uncertainty surrounding shipping through the Strait of Hormuz significantly altered global trade flows.

Higher marine insurance costs, vessel rerouting, and longer transit times increased the landed cost of petrochemical products worldwide.

Import-dependent markets across Asia and Europe experienced rising prices despite relatively stable downstream demand, as buyers competed for limited prompt cargoes while suppliers factored logistics uncertainty into contract offers.

Since June, however, the market structure has changed considerably. The gradual normalization of vessel movement through the Strait of Hormuz, coupled with lower freight charges and weakening crude oil prices, has reduced production and transportation costs across the petrochemical value chain.

This has triggered broad price corrections in several chemical categories, particularly plasticizers, industrial solvents, and selected dye intermediates.

Price Correction Is Broadening Across Chemical Segments

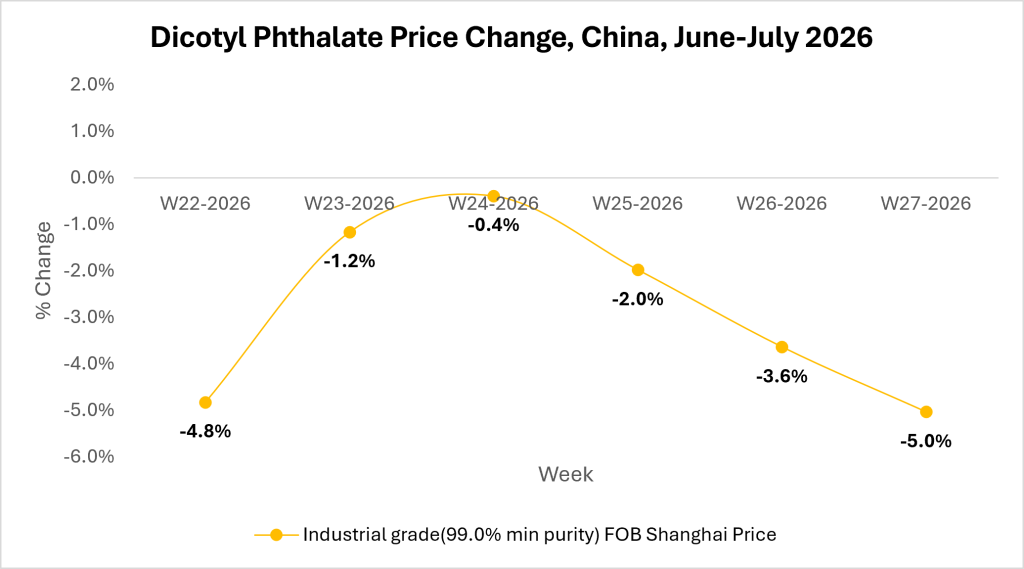

The correction is no longer limited to feedstock economics. Plasticizers such as Dioctyl Phthalate (DOP), Trimethylol propane (TMP), and 2-Ethylhexanol (2-EH) have all experienced downward price pressure as logistics costs eased and downstream demand remained subdued.

Industrial solvents including MIBK and n-Hexane have followed a similar trajectory, with domestic producers implementing successive price reductions amid adequate inventories and weak consumption from coatings, adhesives, pharmaceuticals, and manufacturing sectors.

Source: Price Watch™ DOP Prices

Meanwhile, H-Acid prices have stabilized after declining earlier in the May. Rather than aggressive inventory building, buyers are increasingly purchasing on a need-to basis, reflecting improved confidence in product availability and shorter replenishment cycles.

The result is a synchronized correction across multiple chemical categories rather than isolated price declines.

An overlooked factor behind the current market correction is the shift in corporate procurement strategies.

During the peak of supply uncertainty, manufacturers accumulated higher inventories to safeguard production.

As logistics improved and supply chains stabilized, those inventories reduced the urgency for fresh purchases.

Instead of replenishing stocks, buyers have prioritized working capital optimization, delaying purchases until immediate production requirements arise.

Crude oil markets also shifted into a softer phase during the latter part of the second quarter, providing significant relief to the petrochemical value chain.

West Texas Intermediate (WTI) crude traded below USD 69 per barrel, hovering near its lowest level since late February, as supply concerns eased following the normalization of energy shipments through the Strait of Hormuz.

Market sentiment weakened further after OPEC+ approved another incremental production increase of approximately 188,000 barrels per day, led by Saudi Arabia and Russia, reflecting growing confidence in regional stability and the group’s commitment to meeting global demand.

Tanker traffic through the Strait of Hormuz showed clear signs of recovery, reducing logistics disruptions and easing freight costs for energy and petrochemical cargoes.

Petrochemical Market Outlook

The petrochemical market is entering a phase where structural indicators may outweigh geopolitical developments.

Lower crude oil prices and improving logistics are creating a favourable cost environment, but sustained price declines will ultimately depend on downstream demand recovery and producers’ willingness to adjust operating rates.

Consensus across the industry suggests that the extraordinary logistics premium built into petrochemical pricing is gradually fading.

However, the market has not yet entered a surplus environment, and isolated supply constraints could continue supporting selected product categories.

Currently Petrochemical market softer crude oil prices, easing freight costs, declining plasticizer and solvent prices, stable dye intermediate markets, and cautious procurement activity across major importing regions.

The market has largely shifted from managing supply disruptions to balancing inventories and protecting margins.

As freight rates normalize and crude oil weakens, will Petrochemical prices will follow a downward trajectory, or will producers defend margins through higher price trend. Stay updated with Price Watch™ for more information.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.