Price-Watch™ provides real-time price assessments and price forecasts for EPDM Rubber across top trading regions:

| EPDM Rubber Regional Coverage | EPDM Rubber Grade and Country Coverage | EPDM Rubber Pricing Data Coverage Explanation |

| Asia EPDM Rubber Pricing Analysis | EPDM Rubber Medium diene ENB Content (4.5-5.7) FOB Prices at Busan Port, South Korea | Weekly Price Update on EPDM Rubber Real-Time Export Prices from Busan Port, South Korea to Global Markets |

| EPDM Rubber High diene ENB Content (7.9-8.1) FOB Prices at Busan Port, South Korea | Weekly Price Update on EPDM Rubber Real-Time Export Prices from Busan Port, South Korea to Global Markets | |

| EPDM Rubber Medium Diene ENB Content (4.6-5) FOB Prices at Tokyo Port, Japan | Weekly Price Update on EPDM Rubber Real-Time Export Prices from Tokyo Port, Japan to Global Markets | |

| EPDM Rubber Medium diene ENB Content (4.5-5.7) CIF Prices at Shanghai, China from South Korea | Weekly Price Update on EPDM Rubber Real-Time Import Prices at Shanghai, China from South Korea | |

| EPDM Rubber High diene ENB Content (7.9-8.1) CIF Prices at Shanghai, China from South Korea | Weekly Price Update on EPDM Rubber Real-Time Import Prices at Shanghai, China from South Korea | |

| EPDM Rubber Medium diene ENB Content (4.5-5.7) CIF Prices at Nhava Sheva Port, India from South Korea | Weekly Price Update on EPDM Rubber Real-Time Import Prices at Nhava Sheva Port, India from South Korea | |

| EPDM Rubber High diene ENB Content (7.9-8.1) CIF Prices at Nhava Sheva Port, India from South Korea | Weekly Price Update on EPDM Rubber Real-Time Import Prices at Nhava Sheva Port, India from South Korea | |

| EPDM Rubber Medium Diene ENB Content (4.6-5) CIF Prices at Nhava Sheva Port, India from Japan | Weekly Price Update on EPDM Rubber Real-Time Import Prices at Nhava Sheva Port, India from Japan | |

| EPDM Rubber Medium diene ENB Content (4.5-5.7) Ex-Mumbai Domestic Prices, West India | Weekly Price Update on EPDM Rubber Domestic Prices at Mumbai, West India | |

| EPDM Rubber High diene ENB Content (7.9-8.1) Ex-Mumbai Domestic Prices, West India | Weekly Price Update on EPDM Rubber Domestic Prices at Mumbai, West India | |

| EPDM Rubber Medium diene ENB Content (4.5-5.7) CIF Prices at Laem Chabang Port, Thailand from South Korea | Weekly Price Update on EPDM Rubber Real-Time Import Prices at Laem Chabang Port, Thailand from South Korea | |

| EPDM Rubber High diene ENB Content (7.9-8.1) CIF Prices at Laem Chabang Port, Thailand from South Korea | Weekly Price Update on EPDM Rubber Real-Time Import Prices at Laem Chabang Port, Thailand from South Korea | |

| EPDM Rubber Medium Diene ENB Content (4.6-5) CIF Prices at Laem Chabang Port, Thailand from Japan | Weekly Price Update on EPDM Rubber Real-Time Import Prices at Laem Chabang Port, Thailand from Japan | |

| North America EPDM Rubber Pricing Analysis | EPDM Rubber Medium Diene ENB Content (4.7) FOB Prices at Houston Port, USA | Weekly Price Update on EPDM Rubber Real-Time Export Prices from Houston Port, USA to Global Markets |

| Europe EPDM Rubber Pricing Analysis | EPDM Rubber Medium diene Oil Extended; ENB Content (4.1-4.3) FOB Prices at Rotterdam Port, Netherlands | Weekly Price Update on EPDM Rubber Real-Time Export Prices from Rotterdam Port, Netherlands to Global Markets |

Note: In assessments structured as CIF [Importing Port] (Exporting Country), the country mentioned in brackets indicates the primary origin of supply (exporting country), while the named port refers to the destination port in the importing country. Other Incoterms (FOB, FD, EXW, etc.) should be interpreted in accordance with standard international trade definitions.

Ethylene Propylene Diene Monomer (EPDM) Rubber Price Trend Q1 2026

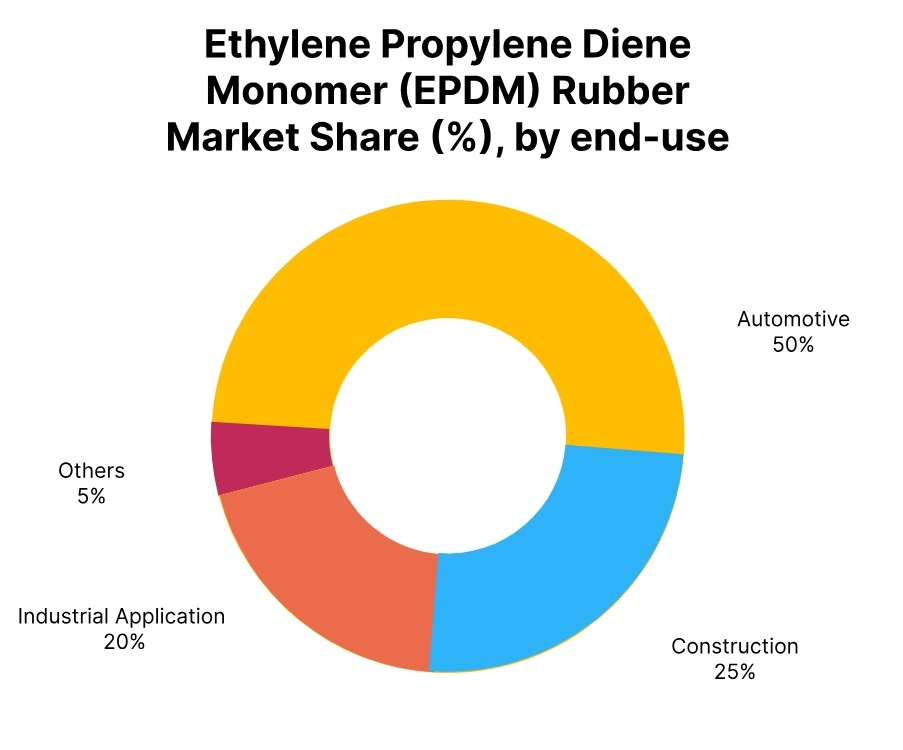

EPDM rubber price trends have been stable globally except for Japan during Q1 2026 in all key markets, with an increasing price trend observed only in Japan. For instance, markets such as South Korea and Indonesia have seen no change in prices despite challenges in terms of supplies in APAC due to sustained demand from automotive and construction segments.

On the other hand, in Japan, there has been a minor increase in prices owing to reduced supplies in the market. In the US and Europe, prices of EPDM rubber have seen an upward trend, with an increase of about 8% to 9% respectively.

This increase in prices is due to tight supplies, especially in the ethylene market, along with increased cost of raw materials. Moreover, geopolitical concerns such as the conflict in the Middle East have raised logistics costs, causing price hikes.

South Korea: EPDM Rubber Export prices FOB Busan, South Korea; Grade- Medium diene; ENB Content (4.5-5.7)

The epdm rubber price trends in South Korea for the first quarter of 2026 have been relatively stable due to the existing oversupply that started in the last quarter of 2025. Nonetheless, the consistent demand from the automotive industry and manufacturing sectors has helped maintain stable prices. In March 2026, EPDM prices in South Korea saw a rise of about 8%.

The EPDM prices in South Korea growth has been fuelled by the Middle East tension and the shutdown of the Strait of Hormuz, resulting in South Korean petrochemical facilities declaring force majeure, which has disrupted the naphtha supply.

Furthermore, several Crackers have reduced their production to avoid plant closures. Increased crude oil prices, the scarcity of feedstocks (ethylene and propylene), and high refining margins have further pushed up prices, and increased demand from India and Thailand, which have no local production capabilities, has escalated the price surge in South Korea.

USA: EPDM Rubber Export prices FOB Houston, USA; Grade- Medium Diene; ENB Content (4.7)

For the first quarter of 2026, the epdm rubber price trends in the US have risen by about 0.9%. This rise in the EPDM prices is mainly due to constant demand for automotive and industrial sectors coupled with disturbances in the Middle East conflict. Despite this, there has been minimal price increases since the market has managed to maintain balance despite challenges.

Increased cost pressure in terms of production costs due to increased crude oil prices has contributed towards rising prices. In March 2026, EPDM rubber price in the US is about 7% increase. EPDM rubber price in the US rise has been attributed to various critical issues that are impacting the market conditions.

Firstly, the closure of the Strait of Hormuz where Qatar has decided to shut down operations in Ras Laffan has interrupted about 20% of global LNG flows resulting into a fuel crisis in addition to feedstocks shortages (ethylene and propylene) coupled with high production costs. This has resulted in an increased gasoline prices due to geopolitical tensions in the region.

Netherlands: EPDM Rubber Export prices FOB Rotterdam, Netherlands; Grade- Medium Diene; Oil Extended; ENB Content (4.1-4.3)

The epdm rubber price trend in the Netherlands during the first quarter of 2026 has risen by about 0.7%. The rise has been influenced by constant demand from the automotive industry and the industrial sector coupled with global logistics issues. Although there has been an increase in prices, the effects have been relatively minor since prices have remained relatively stable.

In March 2026, epdm rubber price in the Netherlands have skyrocketed by roughly 9%. The EPDM price in the Netherlands main reason behind the price hike has been attributed to the Iran crisis that may lead to energy supply disruptions and inflation in Europe.

The shutting down of the Strait of Hormuz and continuous Qatar liquefied natural gas (LNG) production has created risks of shortages of oil and gas in Europe. Shortage of naphtha and natural gas used in producing ethylene has led to the rising price of ethylene, thus affecting the price of EPDM rubber production.

Japan: EPDM Rubber Export prices FOB Tokyo, Japan; Grade- Medium Diene; ENB Content (4.6-5)

In Q1 2026, the epdm price trend in Japan has increased by around 0.6%. This rise has been driven by steady demand from the automotive and industrial sectors, along with some ongoing supply chain disruptions. EPDM rubber price in Japan has remained relatively moderate, with the market maintaining a balance despite external challenges.

In March 2026, EPDM rubber prices in Japan have surged by around 7%. This significant rise has been largely driven by the closure of the Strait of Hormuz amid the ongoing conflict, which has disrupted naphtha supplies, crucial for Ethylene production.

Japan relies on the Middle East for approximately 95% of its oil supply, and the reduction in naphtha cracking has caused a major feedstock (ethylene and propylene) shortage, driving up production costs.

Rising crude oil prices, tightening feedstock availability, elevated refining margins, and supply chain disruptions have all added substantial upward pressure on EPDM prices across Asia, significantly contributing to the price surge in March 2026.

China: EPDM Rubber Import prices CIF Shanghai (South Korea), China; Grade- Medium diene; ENB Content (4.5-5.7)

In Q1 2026, the epdm rubber price trend in China has remained stable. EPDM rubber price in China stability has been largely influenced by steady demand and the ongoing oversupply situation in the ethylene market, which has kept prices relatively unchanged despite external market pressures.

The import flows from South Korea have maintained a consistent level, preventing any significant price fluctuations in the Chinese market. In March 2026, EPDM prices in China have increased by around 8%. This rise has been driven by the ongoing Middle East conflict, which has disrupted naphtha supplies and led to reduced operating rates at South Korean petrochemical plants.

The closure of the Strait of Hormuz has exacerbated the feedstock shortage, driving up the cost of production. Additionally, rising crude oil prices, tightening feedstock availability, and supply chain disruptions across Asia have led to significant upward pressure on prices, resulting in a notable increase in China’s EPDM market.

India: EPDM Rubber Domestically traded prices Ex-Mumbai, India; Grade- Medium Diene; ENB Content (4.5-5.7)

In Q1 2026, EPDM rubber prices in India have increased by around 0.9%. EPDM price trend in India rise has been driven by ongoing supply challenges caused by the Middle East conflict and the closure of the Strait of Hormuz, which have disrupted naphtha supplies. The reduction in naphtha cracking has led to an ethylene shortage, pushing up ethylene prices and increasing EPDM production costs across APAC.

Additionally, supply uncertainties and feedstock (ethylene and propylene) shortages in Asia have forced manufacturers to halt price quotations and delay shipments, further reducing stock availability in India. In March 2026, EPDM rubber prices in India have surged by around 8%.

The increase has been driven by these ongoing disruptions and rising global energy costs. The weakening of the Indian rupee has also made imports more challenging. As a result, the constrained supply and higher production costs have led to a significant rise in EPDM prices in the domestic market.

Thailand: EPDM Rubber Import prices CIF Laem Chabang (South Korea), Thailand; Grade- Medium diene; ENB Content (4.5-5.7)

In Q1 2026, the EPDM rubber price trend in Thailand has remained stable. EPDM rubber price in Thailand stability has been influenced by consistent demand from key industries, including automotive and construction, as well as the ongoing oversupply situation in the ethylene market.

Despite some external market challenges, prices have not experienced significant fluctuations, and the import flows from South Korea have kept the market steady. In March 2026, EPDM prices in Thailand have increased by around 7%. This rise has been driven by disruptions in the Middle East, which have caused significant supply issues, including the closure of the Strait of Hormuz.

This has affected naphtha availability, leading to a shortage of key feedstocks for EPDM production. Additionally, rising crude oil prices, tightening feedstock availability, and supply chain disruptions across Asia have exerted upward pressure on prices, causing a noticeable increase in the Thai market.