Price Watch™ provides real-time price assessments and price forecasts for Graphite Pipe across top trading regions:

| Graphite Flakes Regional Coverage | Graphite Flakes Grade and Country Coverage | Graphite Flakes Pricing Data Coverage Explanation |

| Asia-Pacific Graphite Flakes Pricing Analysis | Graphite Flakes 94–95%, -100 Mesh FOB Prices at Shanghai Port, China | Weekly Price Update on Graphite Flakes Real-Time Export Prices from Shanghai Port, China to Global Markets |

| Graphite Flakes 94–95%, -100 Mesh CIF Prices at Busan, South Korea. Importing from China | Weekly Price Update on Graphite Flakes Real-Time Import Prices at Busan, South Korea, from China | |

| Graphite Flakes 94–95%, -100 Mesh CIF Prices at Nagoya, Japan. Importing from China | Weekly Price Update on Graphite Flakes Real-Time Import Prices at Nagoya, Japan, from China | |

| North America Graphite Flakes Pricing Analysis | Graphite Flakes 94–95%, -100 Mesh CIF Prices at Houston, USA. Importing from China | Weekly Price Update on Graphite Flakes Real-Time Import Prices at Houston, USA, from China |

Note: In assessments structured as CIF [Importing Port] (Exporting Country), the country mentioned in brackets indicates the primary origin of supply (exporting country), while the named port refers to the destination port in the importing country. Other Incoterms (FOB, FD, EXW, etc.) should be interpreted in accordance with standard international trade definitions.

Graphite Price Trend Q1 2026

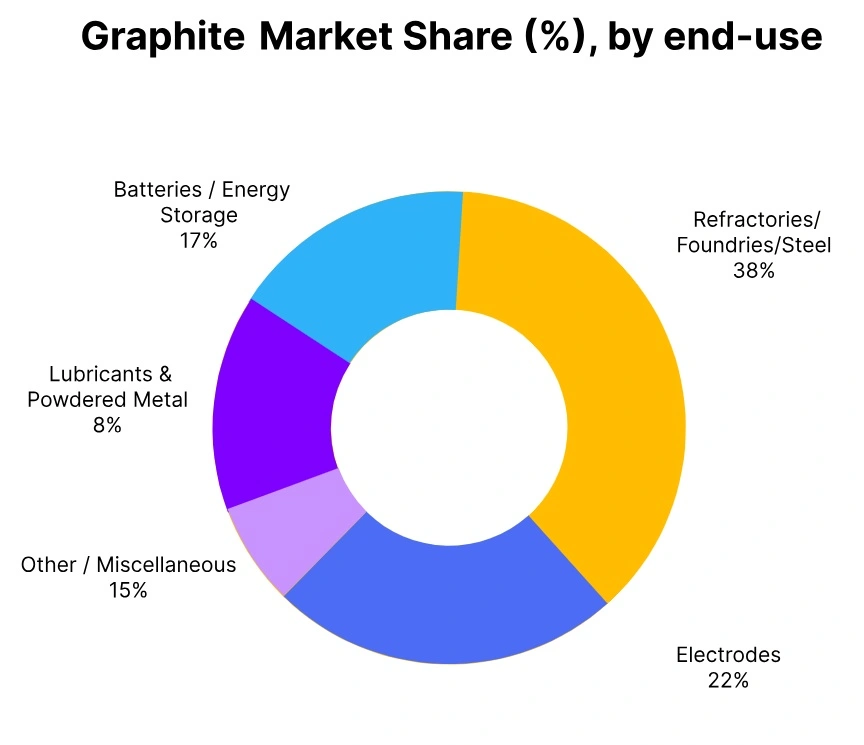

Global graphite prices have risen in Q1 2026, caused by significant increases in demand from batteries, electric vehicle (EV), and energy storage applications and ongoing stable industrial consumption. Significant price increases have been realized in China and South Korea, with further increases also occurring in the United States and Japan, driven by continued strong demand for battery anodes and continued strategic sourcing and disciplined inventory management.

March prices have not reflected the usual volatility, as a balanced market of domestic supply, stable downstream inventories, and discretion in restocking resulted in a stable overall market. In addition, the market exhibited an overall gradual upward trend for the quarter with overall market sentiment relatively bullish, but tempered by stable supply conditions.

China: Graphite Export prices FOB Shanghai, China; Grade- Flakes 94-95%,-100mesh

According to Price-Watch™ , in Q1 2026, Graphite prices in China increased by around 2.17% compared with Q4 2025, supported primarily by firm demand from the battery-grade graphite segment linked to expanding electric vehicle and energy storage production. The Graphite price trend in China remained moderately firm, as domestic battery manufacturers continued to maintain strong material procurement amid sustained growth in global battery capacity.

Additional support came from stable industrial demand and consistent purchasing activity across downstream sectors. Supply conditions, however, remained balanced due to steady domestic production levels and adequate inventories at processing plants, which helped limit excessive market volatility. In March 2026, Graphite prices in China remained largely unchanged month-on-month, reflecting stable spot transactions, balanced supply-demand dynamics, and cautious but steady market sentiment across the critical materials sector.

South Korea: Graphite Import prices CIF Busan, South Korea; Grade- Flakes 94-95%,-100mesh

As of the first quarter of 2026, the price of Graphite in South Korea has been up approximately 2.17% compared to the previous quarter, driven by increased demand from batteries manufactured from lithium-ion batteries. The Graphite price trend in South Korea continued to be moderately bullish as battery producers continue to work through their inventories to prepare for expected growth during 2026.

Both the battery and steel industries are starting to restore activity levels after a period of limited procurement that has resulted from the previous year; Along with the improvement of the overall sentiment in the marketplace as a result of planned capital expenditures by domestic producers in the form of new facilities to be built and long-term supply arrangements being entered into creating new buying opportunities in the marketplace, there are also improving expectations for demand.

On a month-to-month basis, In March of 2026 recorded a minimal price increase of 0.14% in relation to Graphite prices in South Korea being driven mostly from seasonal re-stocking and routine adjustments to orders by various downstream sectors.

Japan: Graphite Import prices CIF Nagoya, Japan; Grade- Flakes 94-95%,-100mesh

In Q1 2026, graphite prices trend in Japan increases by 1.58% compared to Q4 2025, reflecting strengthening demand from the battery and EV sectors, where graphite remains the dominant anode material. In March 2026, Graphite prices in Japan increased modestly by 0.14%, supported by strategic sourcing amid China-dominated production and cautious restocking, while reduced seasonal oversupply from 2025 helped stabilize the market.

Steady industrial demand in refractories, lubricants, and electronics also contributed to underlying strength, and early cycle restocking by buyers signalled a gradual shift from the conservative procurement behaviour seen in late 2025, resulting in a controlled upward trend heading into Q2 2026.

USA: Graphite Import prices CIF Houston, USA; Grade- Flakes 94-95%,-100mesh

In Q1 2026, USA graphite prices trend increases by 2.31% compared to Q4 2025, driven primarily by strong demand from the battery sector, particularly for electric vehicle and energy storage applications. In March 2026, Graphite prices in the US saw a modest 0.09% increase, supported by steady procurement and careful inventory management, while domestic supply initiatives and strategic efforts to secure critical mineral supply chains reinforced market confidence.

Broader commodity cost pressures from geopolitical and macroeconomic factors also contributed to price stability, allowing the market to sustain moderate upward momentum amid consistent downstream consumption.