Price Watch™ provides real-time price assessments and price forecasts for Hot Rolled Coil (HRC) across top trading regions :

| Hot Rolled Coil (HRC) Regional Coverage | Hot Rolled Coil (HRC) Grade and Country Coverage | Hot Rolled Coil (HRC) Pricing Data Coverage Explanation |

| Asia-Pacific Hot Rolled Coil (HRC) Pricing Analysis | HRC IS 2062 2.5–8 mm Ex-Mumbai, India | Weekly Price Update on Hot Rolled Coil Real-Time Domestic Ex-Mumbai Prices in India |

| HRC SS400 2.75 mm FOB Prices at Shanghai Port, China | Weekly Price Update on Hot Rolled Coil Real-Time Export Prices from Shanghai Port, China to Global Markets | |

| North America Hot Rolled Coil (HRC) Pricing Analysis | HRC A1011 1.8 mm Ex-Alabama, USA | Weekly Price Update on Hot Rolled Coil Real-Time Domestic Ex-Alabama Prices in USA |

| Europe Hot Rolled Coil (HRC) Pricing Analysis | HRC S235JR 2–3 mm FD Prices at Sheffield, UK | Weekly Price Update on Hot Rolled Coil Real-Time FD Prices in Sheffield, UK |

Hot Rolled Coil (HRC) Price Trend Q1 2026

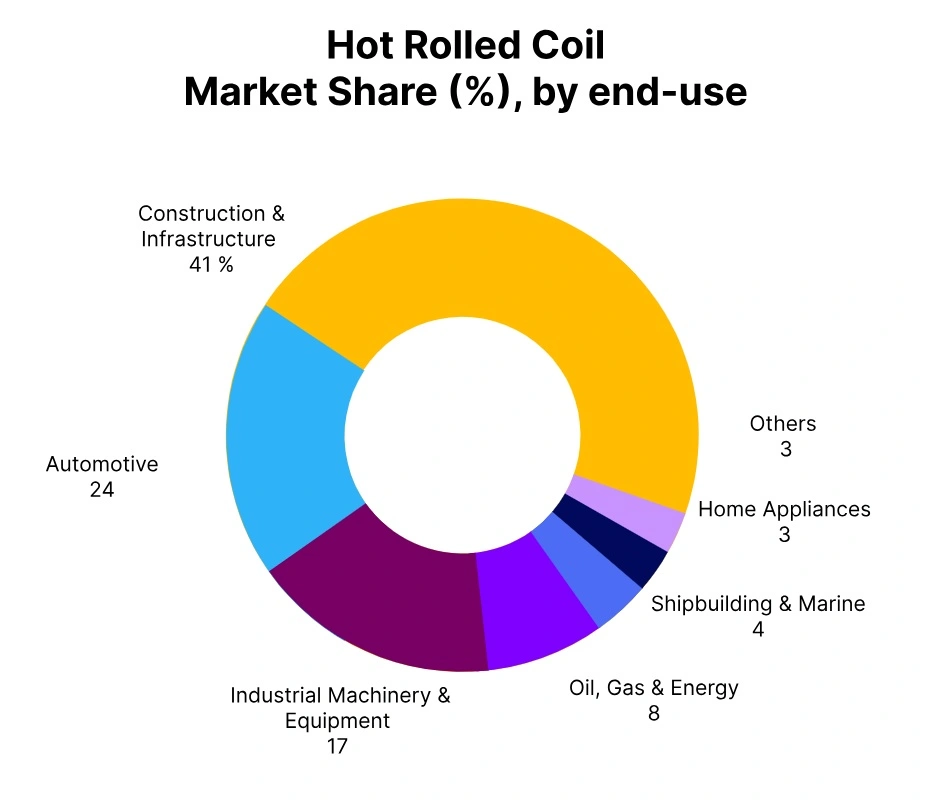

2026 Q1 Hot rolled coil (HRC) market remained generally stronger on the back of increasing global demand for steel from the construction, automotive, and infrastructure sectors; and tighter scrap and iron ore pricing with some regions than others (in terms of key inputs).

The USA experienced the largest gains due to domestic consumption and steel import restrictions, the same held for India and the United Kingdom with large increase to the extent of restocking and large project pipelines.

China remained behind the region with little upside due to constrained output combined with slow export numbers, resulting in an overall positive regionally divergent but positive quarterly results globally as to HRC market conditions.

Hot Rolled Coil (HRC) SS400 2.75mm FOB Shanghai, China

The hot rolled coil price trend in China edged up by 1.4% in Q1 2026, as modest infrastructure support measures and controlled mill restarts helped counterbalance ample inventories and cautious downstream demand from autos and appliances.

Export shipments faced persistent headwinds from rising global protectionism and weaker overseas inquiries, keeping the focus on domestic long-term contracts over volatile spot trading. Secondary markets saw some inventory digestion, but traders remained hesitant amid year-end financial pressures carrying over.

Auto and machinery sectors showed tentative improvement with policy nudges, though white goods demand stayed muted. Mills prioritized capacity utilization for key clients, limiting aggressive spot sales. In March 2026, Hot Rolled Coil prices in China increased 0.3% with balanced supply post-production adjustments.

Selective restocking from fabricators provided mild support amid cooling seasonal demand. Cautious trader activity and steady export barriers limited the gain, aligning with the quarter’s subdued trajectory.

Hot Rolled Coil (HRC) IS2062 2.5-8mm Ex-Mumbai, India

The hot rolled coil price trend in India advanced by 5.9% in Q1 2026, fuelled by vigorous infrastructure projects under government initiatives, real estate recovery, and healthy auto sector intakes tied to festive pre-sales.

Domestic mills gained leverage from reduced import pressure out of Southeast Asia and rising domestic scrap costs, enabling firmer pricing discipline across primary and secondary producers. Downstream processors ramped up coil purchases ahead of monsoon disruptions, tightening spot market dynamics and narrowing discounts.

Construction and pipe makers absorbed surplus into ongoing pipelines, while engineering demand provided steady backdrop support. Import duties held effective against cheaper arrivals, favoring local supply chains.

In March 2026, Hot Rolled Coil prices in India surged 4.6% as government-led tenders boosted volumes significantly. OEM and construction buying intensified, rapidly clearing processor stocks. Elevated input costs from global ore trends reinforced the robust monthly uptick with no signs of softening.

Hot Rolled Coil (HRC) A1011-1.8mm Ex-Alabama, USA

According Price Watch™, The hot rolled coil price trend in the USA surged by 12.7% in Q1 2026, driven by explosive demand from reshoring manufacturing initiatives, accelerating housing starts, and automotive production ramps post-supply chain normalization.

Section 232 tariffs and quota measures curbed uncoated imports effectively from vulnerable origins, allowing domestic mills to command premium realizations. Scrap premiums soared amid tight regional supplies, lifting base costs for both mini-mills and integrated producers alike.

Service centers restocked aggressively to meet surging pipeline needs from fabricators and OEMs, supporting elevated spot levels throughout. Construction and energy sector orders provided additional ballast against any volatility.

In March 2026, Hot Rolled Coil prices in the USA rose 3.4% as consumption momentum stayed strong nationwide. Reduced inventories at distributors spurred higher mill allocations to priority buyers. Tariff stability, firm end-markets in autos and infrastructure, and steady scrap inflows sustained the quarter’s powerful upward drive.

Hot Rolled Coil (HRC) S235JR 2-3mm FD Sheffield, UK

The hot rolled coil price trend in the UK rose by 7.2% in Q1 2026, bolstered by steady construction demand from renewed infrastructure tenders and automotive restocking amid improving economic sentiment. Upstream scrap costs firmed notably, supporting higher mill offers as processors passed on elevated input expenses.

Import competition eased due to ongoing logistics challenges in Europe and a stronger pound, which made overseas tonnage less competitive. Distributors built inventories selectively ahead of spring campaigns, helping absorb available volumes without significant discounts emerging in the spot market.

Downstream fabricators in machinery and general engineering showed improved order flows, adding to the bullish undertone. Mills maintained production discipline post-winter maintenance, which helped stabilize supply chains.

In March 2026, Hot Rolled Coil prices in the UK climbed 5.0% as spring infrastructure tenders accelerated across regions. Lean service center stocks prompted aggressive buying from end-users. Firm raw material values, steady auto sector intakes, and selective import arrivals drove the strong monthly close without reversal signals.