Price Watch™ provides real-time price assessments and price forecasts for Hot Rolled Sheet across top trading regions:

| Hot Rolled Sheet Regional Coverage | Hot Rolled Sheet Grade and Country Coverage | Hot Rolled Sheet Pricing Data Coverage Explanation |

| Asia-Pacific Hot Rolled Sheet Pricing Analysis | HR Sheet SS400 2mm FOB Prices at Shanghai Port, China | Weekly Price Update on HR Sheet SS400 2mm Real-Time Export Prices from Shanghai Port, China to Global Markets |

| HR Sheet IS2062 2mm EX Mumbai Domestic Prices, West India | Weekly Price Update on HR Sheet IS2062 2mm Real-Time Domestic Prices in Mumbai, West India |

|

| North America Hot Rolled Sheet Pricing Analysis | HR Sheet A1011-2mm EX Alabama Domestic Prices, USA | Weekly Price Update on HR Sheet A1011-2mm Real-Time Domestic Prices in Alabama, USA |

| Europe Hot Rolled Sheet Pricing Analysis | HR Sheet S235JR 2mm FD Sheffield Domestic Prices, United Kingdom |

Weekly Price Update on HR Sheet S235JR 2mm Real-Time Domestic Prices in Sheffield, United Kingdom |

| HR Sheet S235JR 2mm EX Ruhr Domestic Prices, Germany | Weekly Price Update on HR Sheet S235JR 2mm Real-Time Domestic Prices in Ruhr, Germany |

Note: In assessments structured as CIF [Importing Port] (Exporting Country), the country mentioned in brackets indicates the primary origin of supply (exporting country), while the named port refers to the destination port in the importing country. Other Incoterms (FOB, FD, EXW, etc.) should be interpreted in accordance with standard international trade definitions.

Hot Rolled (HR) Sheet Price Trend Q1 2026

Between January and March 2026, hr sheet price trend of hot rolled steel in the world generally moved up because of higher production costs (coking coal, iron ore, scrap, and energy) as well as a limited amount of available hot rolled steel in some domestic markets due to reduced import competition.

In addition, increasing geopolitical tensions from the current Iran-Israel conflict and the closure of a major shipping lane (the Strait of Hormuz) have caused an increase in transportation (including freight and insurance) and energy costs, which has contributed to higher prices of hot rolled steel.

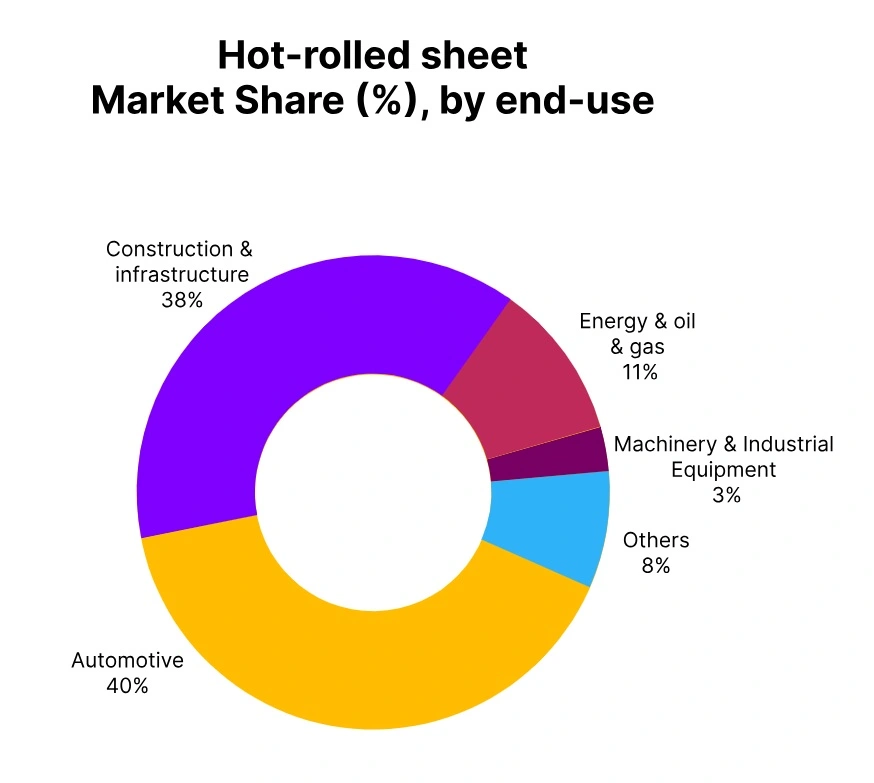

Lastly, an increase in the amount of new building construction and demand for new vehicles and machinery from the construction, automotive, and manufacturing industries has caused an increase in the demand for hot rolled steel, and therefore has contributed to higher prices.

In contrast to other large markets that production and cost pressures outweighed the softness of demand for hot rolled, modest increases in hr sheet price trend occurred because of the tremendous oversupply of hot rolled sheet and poor level of domestic demand within the People’s Republic of China.

China: Hot Rolled (HR) Sheet Export prices FOB Shanghai, China; Grade- SS400 2mm

According to Price-Watch™ , in Q1 2026, Hot Rolled (HR) Sheet prices in China increased marginally by approximately 0.50% compared with Q4 2025, supported mainly by firmer upstream raw material costs, particularly iron ore and coking coal.

The hr sheet price trend in China remained relatively balanced throughout the quarter, as mills maintained disciplined pricing strategies despite subdued downstream demand conditions. Controlled production levels and a slight improvement in global steel market sentiment also contributed to mild upward support.

Seasonal restocking activity following the Lunar New Year strengthened procurement momentum during March, while firmer international hr sheet price trend provided additional market confidence. Geopolitical tensions in the Middle East further influenced the market indirectly through higher freight and insurance costs, which increased overall transaction expenses and supported domestic pricing.

However, disruptions to certain export flows also increased local supply availability, preventing sharper price gains. In March 2026, hr sheet price trend in China rose by around 0.54% month-on-month, reflecting cautious restocking and stable market fundamentals despite ongoing oversupply concerns.

India: Hot Rolled (HR) Sheet Domestic traded prices EX-Mumbai, India; Grade- IS2062 2mm

In the first quarter of 2026, the price of Hot Rolled Sheets in India rose by about 5.37% from the fourth quarter of 2025 due to higher upstream costs and a more favorable domestic market environment. The hr sheet price trend in India remained positive throughout the quarter, primarily due to increasing coking coal and energy prices, which caused steel manufacturers to incur greater production costs.

Further amplifying pressure on costs have been the results of the ongoing Iran – Israel conflict that has caused global oil prices to continue moving higher, as well as all manufacturers’ overall manufacturing costs to increase.

Safeguard duties on steel imports reduced the quantity of lower-priced foreign material entering the market and positively influenced domestic pricing abilities while helping local mills. Demand has been strong for Hot Rolled Sheets from both infrastructure and automotive sectors, contributing to a healthy level of procurement activity during the quarter.

Also adding pressure to the costs associated with Hot Rolled Sheet prices have been the disruptions to key shipping channels such as the Strait of Hormuz that had the variable effect of increasing freight and insurance charges as well as total transaction costs.

In March 2026, the Hot Rolled Sheet price trend in India increased by about 3.17% month over month, continuing to be buoyed by strong demand, limited imports, and significant restrictions on supply.

USA: Hot Rolled (HR) Sheet Domestic traded prices EX Alabama, USA; Grade- A1011-2mm

In Q1 2026, Hot Rolled Sheet prices in the USA increased sharply by approximately 12.13% compared with Q4 2025, supported by tight domestic supply conditions and rising production costs. The hr sheet price trend in the USA remained strongly upward throughout the quarter, as production curtailments and scheduled mill maintenance reduced available supply and strengthened producers’ pricing power.

Higher coking coal and energy prices further intensified cost pressure, while the ongoing Iran–Israel conflict disrupted major shipping routes such as the Strait of Hormuz, driving up crude oil, freight, insurance, and logistics costs across the steel supply chain.

Stringent import tariffs also limited the inflow of lower-priced foreign steel, reinforcing domestic market firmness. Demand from construction and automotive sectors remained stable, supporting continued procurement activity despite elevated prices.

In March 2026, Hot Rolled Sheet prices in the USA rose by around 3.72% month-on-month, reflecting sustained cost-side pressure, controlled imports, and ongoing supply chain disruptions.

Germany: Hot Rolled (HR) Sheet Domestic traded prices EX Ruhr, Germany; Grade- S235JR 2 mm

In Q1 2026, Hot Rolled Sheet prices in Germany increased by approximately 7.18% compared with Q4 2025, supported by rising energy, freight, and raw material costs across the European steel sector. The hr sheet price trend in Germany remained firmly upward throughout the quarter, as disruptions around the Strait of Hormuz and the ongoing Iran–Israel conflict pushed global oil and gas prices higher, increasing both production and logistics expenses.

Freight and insurance costs also rose significantly, adding further pressure to transaction pricing. Tight European supply conditions strengthened market fundamentals, particularly as operational delays at mills in France and Spain reduced regional availability and enhanced domestic pricing power. Higher scrap and iron ore prices further reinforced cost-side pressure during the quarter.

Demand from automotive, machinery, and construction sectors remained steady, while reduced import competition under EU trade measures supported firmer local pricing. In March 2026, Hot Rolled Sheet prices in Germany rose sharply by around 5.18% month-on-month, reflecting tighter supply conditions and sustained industrial demand.

UK: Hot Rolled (HR) Sheet Domestic traded prices FD Sheffield, UK; Grade- S235JR 2 mm

In Q1 2026, hr sheet price trend in the UK increased by approximately 6.01% compared with Q4 2025, supported by elevated upstream costs and tighter domestic supply conditions. The Hot Rolled Sheet price trend in the UK remained firmly upward throughout the quarter, as steelmakers faced rising coking coal, scrap, and energy costs.

These pressures were further intensified by the ongoing Middle East conflict, which disrupted shipping activity around the Strait of Hormuz and pushed global oil and LNG prices higher, increasing freight and insurance expenses across the supply chain.

Import quotas and reduced inflows of lower-priced foreign steel strengthened the pricing power of domestic producers, while steady demand from construction, automotive, and manufacturing sectors supported consistent procurement activity.

Broader inflationary pressure across the UK economy also contributed to higher production and operating costs for mills. In March 2026, Hot Rolled Sheet prices in the UK rose sharply by around 3.77% month-on-month, reflecting continued supply tightness and persistent cost-side pressure.