𝐏𝐫𝐢𝐜𝐞 𝐖𝐚𝐭𝐜𝐡™ provides price assessments for Silicon metal across top trading regions:

Asia-Pacific

- Silicon Metal Grade 441 FOB Shanghai, China

- Silicon Metal Grade 553 FOB Shanghai, China

- Silicon Metal Grade 553 CIF Nhava Sheva (China), India

- Silicon Metal Grade 441 CIF Nhava Sheva (China), India

North America

- Silicon Metal Grade 441 CIF Houston (Brazil), USA

- Silicon Metal Grade 553 CIF Houston (Brazil)USA

Europe

- Silicon Metal Grade 441 CIF Southampton (China), United Kingdom

- Silicon Metal Grade 553 CIF Southampton (China), United Kingdom

Note: In assessments structured as CIF [Importing Port] (Exporting Country), the country mentioned in brackets indicates the primary origin of supply (exporting country), while the named port refers to the destination port in the importing country. Other Incoterms (FOB, FD, EXW, etc.) should be interpreted in accordance with standard international trade definitions.

Silicon Metal Price Trend Q4 2025

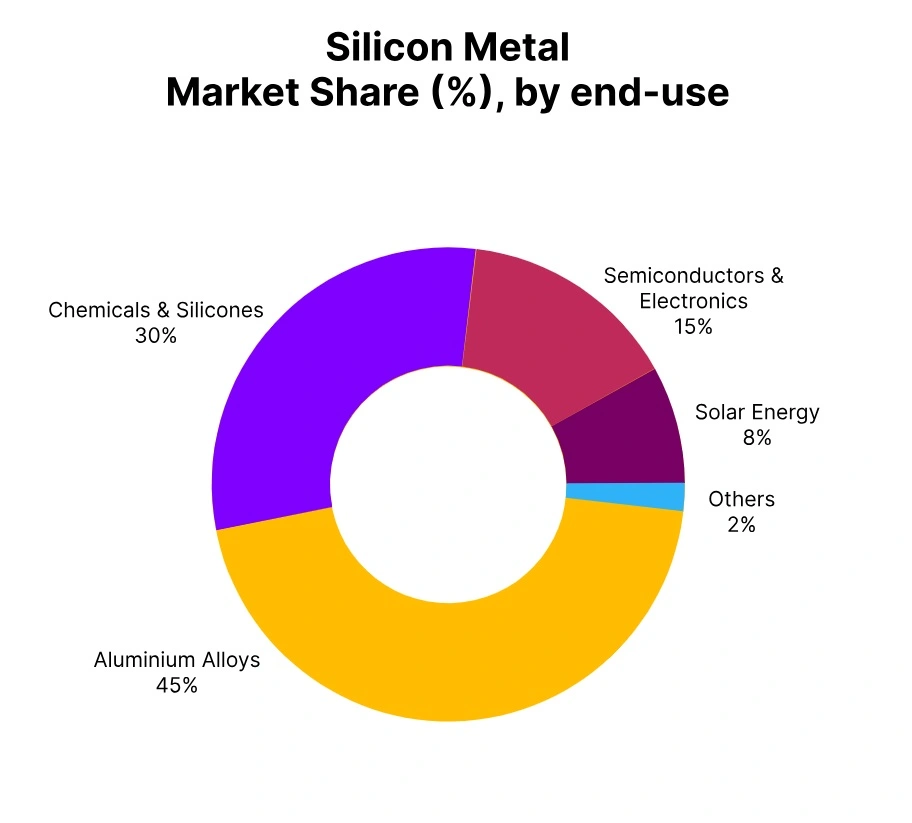

In Q4 2025, the global Silicon Metal market showed a mixed performance, with declines in major producing regions like China, the United Kingdom, and India, while the United States saw modest gains. The overall market remained cautious, weighed down by oversupply and moderate buying activity from key downstream industries, including aluminium alloy and chemical sectors. Despite some stabilization in certain regions, the global market maintained a generally subdued tone throughout the quarter.

China: Silicon Metal Export prices FOB Shanghai, China; Grade- 441,553

According to Price-Watch™ , In Q4 2025, the price trend of Silicon Metal in China declined by 3.97% compared to Q3, indicating continued bearish market conditions amid persistent supply-demand imbalance. The decline was largely attributed to subdued demand from the aluminium alloy, chemical, and solar photovoltaic sectors, as downstream producers maintained cautious procurement strategies and focused on inventory control amid moderate industrial activity.

The solar value chain, particularly polysilicon producers, operated at restrained rates, limiting fresh silicon metal consumption despite expectations of seasonal improvement. On the supply side, domestic production remained relatively stable, with only selective output adjustments in high-electricity-cost regions, while overall inventories stayed sufficient, reinforcing downward price pressure. Export activity remained moderate, constrained by global economic uncertainty and competitive pricing dynamics.

Although production costs such as electricity and raw materials showed limited fluctuation, weak downstream absorption outweighed cost support, sustaining the soft pricing environment. In December 2025, prices recorded a marginal 0.36% decrease, reflecting continued year-end destocking and cautious buying sentiment. Overall, the silicon metal market in China during Q4 2025 maintained a mild downward trajectory, with expectations of gradual stabilization in early 2026 contingent upon recovery in solar-related demand and broader industrial momentum.

India: Silicon Metal Import prices CIF Nhava Sheva, India; Grade- 441,553

In Q4 2025, silicon metal prices trend in India declined by 1.64% quarter-on-quarter compared to Q3, reflecting continued subdued demand from key downstream sectors such as aluminium alloys, chemicals, and solar photovoltaics amid slower industrial and construction activity.

Buyers maintained cautious procurement strategies with comfortable inventory levels, while adequate domestic supply and steady import inflows from Asian markets kept pricing under pressure. Stable raw material and energy costs prevented sharp volatility; however, the persistent mismatch between sufficient supply and muted consumption sustained a bearish market sentiment.

In December 2025, prices edged down by a further 0.32% month-on-month, driven by year-end demand softness and limited spot buying interest. Overall, the Indian silicon metal market in Q4 2025 continued its softening trend, though expectations remain for gradual stabilization in early 2026 as downstream industrial activity and renewable energy investments regain momentum.

USA: Silicon Metal Import prices CIF Houston, USA; Grade- 441,553

In Q4 2025, silicon metal prices trend in the USA increased by 1.26% compared to Q3, supported by steady demand from the aluminium alloy, silicone chemical, and solar photovoltaic sectors amid consistent industrial activity and pre-year-end procurement. Moderate restocking by downstream manufacturers, coupled with relatively balanced domestic supply conditions and disciplined production management, contributed to the quarterly uptick.

Stable but firm raw material and energy costs also provided mild upward pressure on offers. However, in December 2025, prices declined by 0.52% month-on-month, reflecting typical year-end destocking, slower procurement activity, and sufficient inventory availability at ports due to ongoing import flows. Despite the December dip, the overall Q4 market sentiment remained slightly positive, with expectations of stable demand and gradual price firmness moving into early 2026 as downstream consumption trends remain steady.

UK: Silicon Import Imoprt prices CIF Southampton, UK; Grade- 441,553

In Q4 2025, silicon metal prices trend in the United Kingdom declined by 3.30% quarter-on-quarter, continuing the softening trend from Q3 amid weak demand from the aluminium alloy, chemical, and solar photovoltaic industries. Slower downstream procurement, combined with competitive imports from Europe and Asia, exerted downward pressure on prices, while stable energy and raw material costs offered limited support.

By December 2025, prices fell marginally by 0.23% month-on-month, reflecting subdued year-end industrial activity and cautious inventory management by producers. Overall, the UK silicon metal market remained bearish throughout Q4, with expectations of gradual stabilization in early 2026 as downstream demand and renewable energy projects begin to recover.