Price-Watch™ provides real-time price assessments and price forecasts for Stainless-Steel CR Coil across top trading regions:

| Stainless-Steel CR Coil Regional Coverage | Stainless-Steel CR Coil Grade and Country Coverage | Stainless-Steel CR Coil Pricing Data Coverage Explanation |

| Asia Stainless-Steel CR Coil Pricing Analysis | Stainless-Steel CR Coil 304/2B-1mm FOB at Shanghai port, China | Weekly Price Update on Stainless-Steel CR Coil Real-Time Export Prices from Shanghai port, China to Global Markets |

| Stainless-Steel CR Coil 304/2B-1mm Ex-Mumbai Domestic Prices, India | Real-Time Weekly Price Update of Stainless-Steel CR Coil Domestic Prices in Mumbai, India | |

| Europe Stainless-Steel CR Coil Pricing Analysis | Stainless-Steel CR Coil 304/2B-2mm FD Prices at Willich, Germany | Weekly Price Update Stainless-Steel CR Coil Real-Time Export Prices at Willich, Germany to European Markets |

| North America Stainless-Steel CR Coil Pricing Analysis | Stainless-Steel CR Coil 304/2B-2mm Prices Del Alabama, USA | Real-Time Weekly Price Update of Stainless-Steel CR Coil Domestic Prices in Alabama, USA |

Note: In assessments structured as CIF [Importing Port] (Exporting Country), the country mentioned in brackets indicates the primary origin of supply (exporting country), while the named port refers to the destination port in the importing country. Other Incoterms (FOB, FD, EXW, etc.) should be interpreted in accordance with standard international trade definitions.

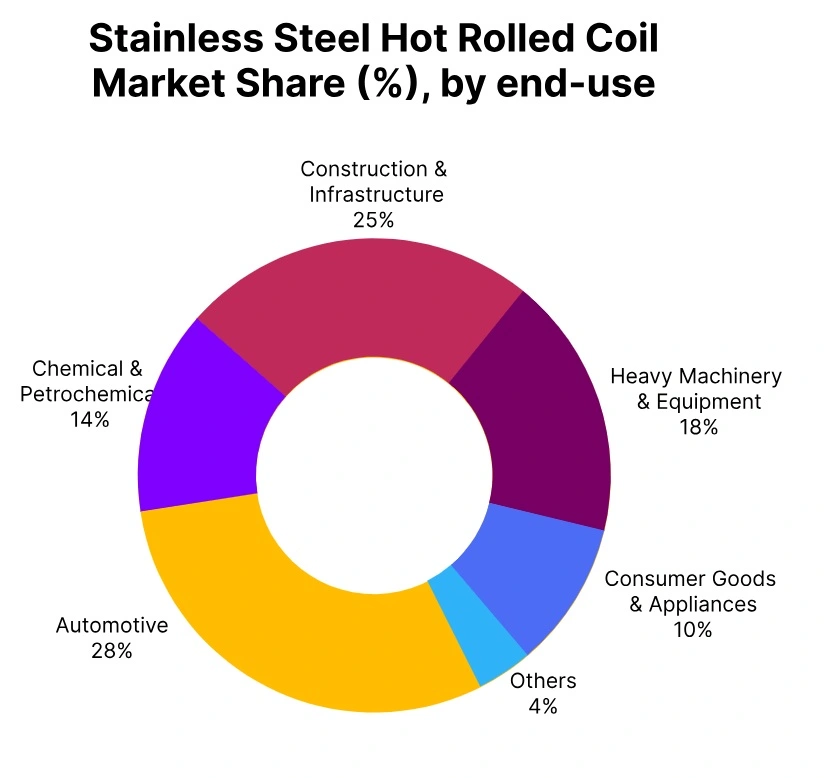

SS HR Coil Price Trend Q1 2026

In Q1 2026, the global stainless steel hot rolled coil (HR Coil) market edged modestly higher overall, propelled by steady demand from construction, automotive, and appliances, coupled with nickel and chrome cost firmness amid supply chain recoveries.

India and the USA led regional gains on infrastructure and reshoring, Germany saw mild support from European auto restocking, while China dipped slightly on excess capacity and export hurdles, underscoring a balanced yet regionally varied sentiment.

Stainless Steel, 304-3mm, FOB Shanghai, China

According to Price-Watch™ , the price trend of Stainless Steel HR Coil in China rose by 0.32% in Q1 2026, though tempered by ample inventories at coastal bases, controlled austenitic 304 production restarts, and cautious orders from construction and white goods sectors amid economic moderation. Nickel premiums eased marginally but ferrochrome costs provided some floor, while exports faced anti-dumping scrutiny from India and the West, limiting upside.

Downstream fabricators optimized with 430 grades, paring 300-series needs. Spot discounts persisted in spot markets. In March 2026, Stainless Steel HR Coil prices in China declined 0.74% as seasonal destocking paused. Mill allocations favored contracts over spot. Subdued inquiries sealed the quarterly mildness.

Stainless Steel, 304-3mm,, Ex-Mumbai, India

The price trend of Stainless Steel HR Coil in India advanced 2.77% in Q1 2026, fueled by railway and metro projects demanding 304/316 coils, plus appliance and dairy equipment surges. Jindal and local mills gained from import duties curbing Chinese 200-series, with ferrochrome self-sufficiency aiding costs. Construction roofing in 430 added volumes.

Spot premiums built in western hubs. In March 2026, Stainless Steel HR Coil prices in India surged 6.16% as infrastructure tenders peaked. Processor buying tightened supply. Strong domestic steel momentum capped the quarter strongly.

Stainless Steel 304/2B-2mm, Del Alabama, USA

The price trend of Stainless Steel HR Coil in the USA climbed 1.12% in Q1 2026, driven by robust infrastructure tubing, railcar fabrications, and food processing needs, with North American mills like Acerinox benefiting from tariff shields. Chromium and nickel ore costs firmed conversion margins amid stable slab feeds. EAF stainless output ramped selectively. In March 2026, Stainless Steel HR Coil prices in the USA rose 0.23% on balanced restocking. Foundry and OEM demand held firm. Protective measures sustained the gradual quarterly ascent.

Stainless Steel 304/2B-2mm, Del Alabama, Germany

The price trend of Stainless Steel HR Coil in Germany increased 0.98% in Q1 2026, supported by European automotive restocking for exhausts and trims, alongside construction cladding demands amid green building pushes. Outokumpu and Aperam mills held discipline on 304/316 slabs, with nickel uptrends lifting base costs. Import competition from Asia waned on logistics costs, favoring ThyssenKrupp processing lines.

Appliance makers added steady 430/409 pulls. In March 2026, Stainless Steel HR Coil prices in Germany gained 1.31% with OEM spring campaigns. Lean service center stocks firmed offers. Eurozone recovery cues bolstered the quarterly progress.