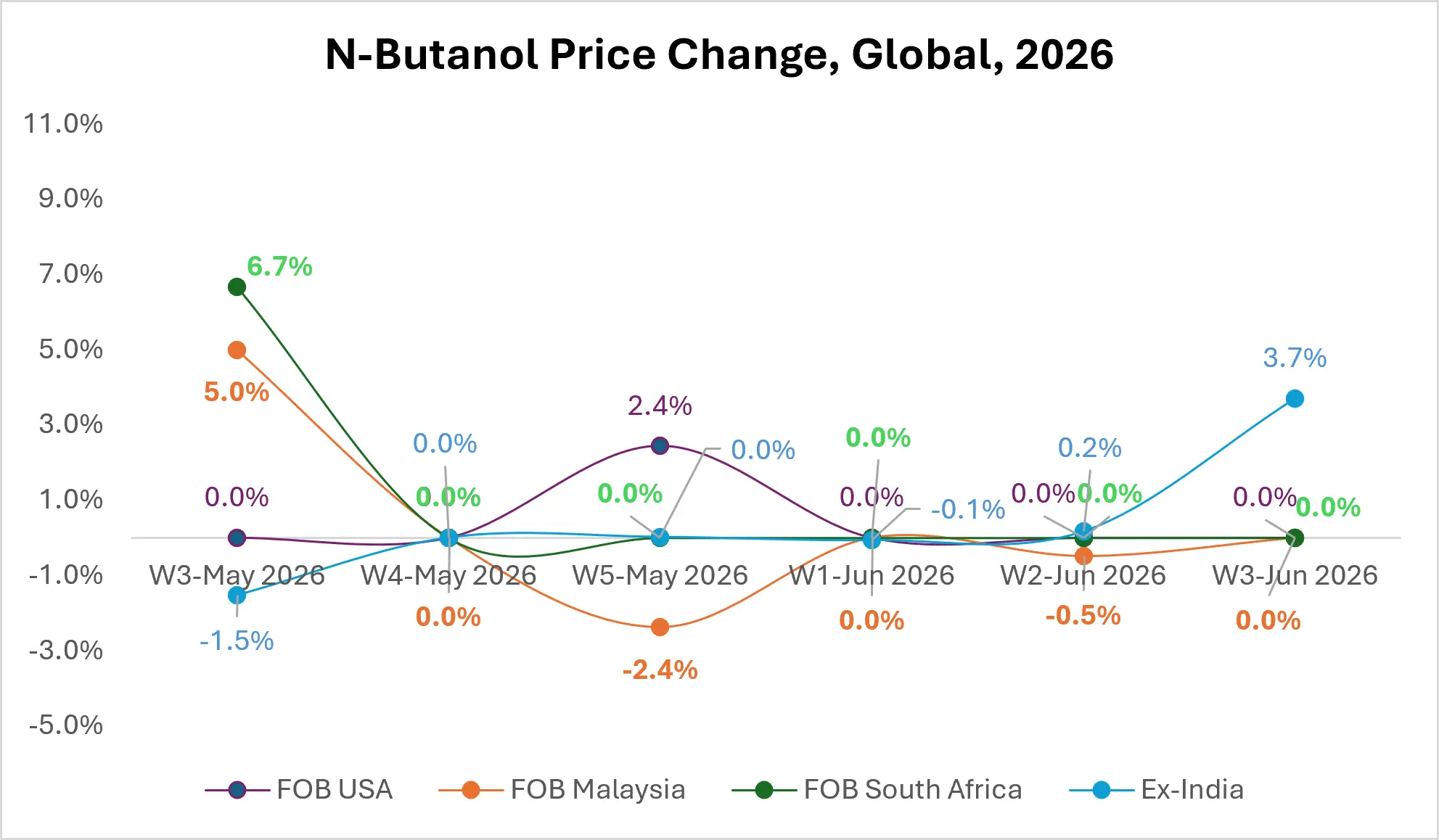

A synchronized chemical pricing cycle is quietly breaking apart. What once moved in near parallel across major FOB hubs for N-Butanol is now diverging into route-specific behavior, where logistics timing and contract rigidity matter as much as feedstock direction.

Between W3 May and W3 June 2026, pricing signals across FOB USA, Malaysia, South Africa, and Ex-India show not a uniform correction, but a fragmented rebalancing of global solvent trade flows.

The most important shift is not the magnitude of price change, but the asymmetry in timing across regions especially as Asia begins to decouple from Western contract inertia.

Fragmentation of a Previously Synchronized Market

N-Butanol pricing is typically anchored to propylene costs and downstream demand from acrylates, coatings, and plasticizers. However, the latest cycle shows that regional logistics, contract reset cycles, and inventory positioning are now overriding pure feedstock signals.

Source: Price-watch.ai

Regional & Route Dislocation

- Asia Export Chain (Malaysia & Ex-India Routes)

Asia is showing the highest volatility. Malaysia moved from early-month strength into gradual weakening as downstream buyers delayed restocking.In contrast, Ex-India pricing reversed sharply into positive territory by W3 June, reflecting tightening availability and faster domestic absorption of export-linked volumes. - USA FOB Stability Corridor

The USA market remains structurally frozen at 0.0% changes across the observed window. This is not a reflection of stability in fundamentals, but of rigid quarterly contracting in downstream solvent procurement, particularly in coatings and industrial adhesives. - South Africa Export Channel

South Africa initially showed strong upward movement (+6.7%) but flattened quickly, suggesting a temporary logistics or import-driven spike rather than sustained demand growth.The correction highlights dependence on imported cargo timing rather than structural consumption shifts.

Regional Credit Window Compression

A less visible but increasingly important factor is tightening credit availability for chemical distributors across Asia and Africa. Reduced working capital cycles are forcing smaller, more frequent purchases, amplifying price volatility even in the absence of major feedstock shifts.

N-Butanol Market Outlook

The N-Butanol market is entering a structurally fragmented phase. Instead of a unified global price direction, regional hubs will continue to move independently based on contract timing, freight normalization, and credit constraints.

Asia is likely to remain the most responsive region, while USA pricing stays lagging but stable until the next contract reset cycle.

To know the answer to these questions, will rising Ex-India N-Butanol prices while FOB USA remains flat eventually force a delayed correction through Western contract cycles, and could deeper credit tightening across Asia shift the market from contract-led stability to sustained spot-driven volatility in global N-Butanol trade flows?

These are precisely the structural divergences that continue to reshape regional pricing behavior across solvent markets.

For deeper insights, data-driven updates, and continuous tracking of these cross-regional price signals, visit Price-watch.ai

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.