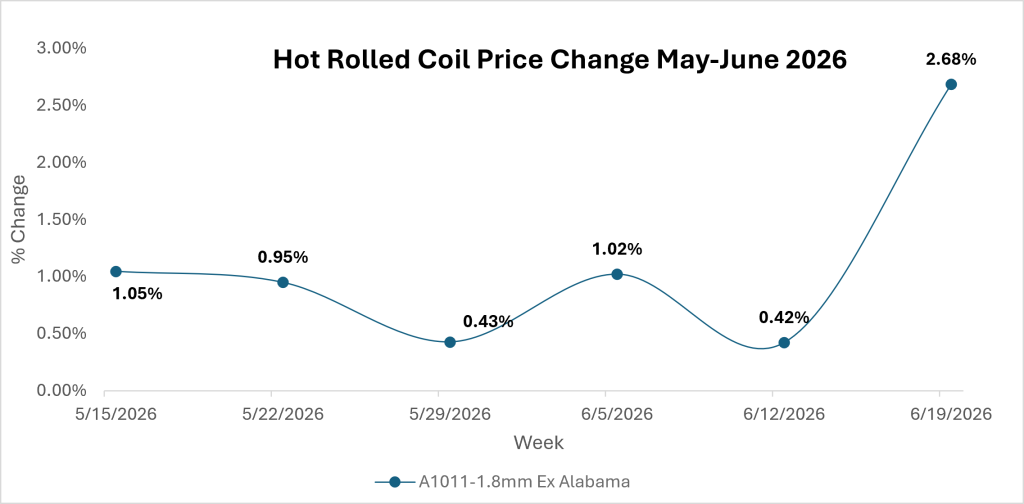

The Hot Rolled Coil (HRC) market exhibited a mixed trend last week, with prices registering both gains and declines across major global regions.

Upward momentum was supported by tighter supply availability, stable-to-firm raw material costs, and improved buying activity in select markets.

At the same time, subdued demand from end-use sectors, cautious purchasing strategies, and competitive import offers continued to exert downward pressure on prices.

Market participants remained vigilant as regional disparities in supply-demand dynamics became increasingly evident.

While some producers attempted price increases to protect margins, buyers largely adopted a wait-and-see approach amid uncertain consumption prospects.

The week’s mixed performance underscores the delicate balance between supply-side support and demand-side challenges, leaving the HRC market in a state of cautious equilibrium as it heads into the coming weeks.

Source: Price Watch™ HRC Prices

Reasons for HRC Price Decline

- Pre-monsoon and monsoon-led slowdown in construction and infrastructure activity: The arrival of the monsoon season is expected to temporarily slow construction and project execution activities across several regions of India, resulting in reduced short-term demand for flat steel products. With execution on infrastructure, roofing, and industrial fabrication projects pausing or slowing due to rains and waterlogging, fresh order placement from converters and OEMs turned cautious in the first two weeks of June, directly weighing on mill realizations.

- Need-based, low-volume buying by traders and processors: Steel demand remained largely need-based across both project and retail segments, as pre-monsoon slowdown, extreme weather conditions, and cautious procurement strategies restricted fresh buying activity. Distributors avoided building inventory ahead of the monsoon, preferring to work down existing stock rather than commit to fresh purchases.

- Correction in Chinese/regional export benchmarks: Ex-China HRC prices fell as supportive fundamentals weakened and softer factors disappeared through the second week of June, which pulled down the broader Asian price reference that Indian domestic offers are benchmarked against.

- Easing input cost momentum gave mills less reason to defend prices aggressively: With iron ore and scrap costs relatively range-bound through this period and no acute raw-material shock, mills had limited cost-side justification to resist the downward pull from soft demand and competitive export markets.

HRC Market Outlook

The Hot Rolled Coil (HRC) market is expected to remain cautiously balanced in the coming weeks, with regional price movements likely to be influenced by evolving supply-demand fundamentals.

Support from controlled mill production, firm raw material costs, and selective restocking activity could help sustain prices in some markets.

However, persistent uncertainty surrounding downstream demand, competitive import offers, and cautious buyer sentiment may limit significant upward momentum.

Market participants will closely monitor inventory levels, industrial activity, and trade developments for clearer direction.

Overall, HRC prices are expected to trade within a narrow range, with localized fluctuations reflecting differing regional market conditions and purchasing trends.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.