USA reopened the door to Iranian urea through August 21. Egypt rewrote its nitrogen export tax twice in seven weeks. Neither move erases the shipping risk still keeping global nitrogen prices elevated.

Policy Changes Improve Supply Outlook

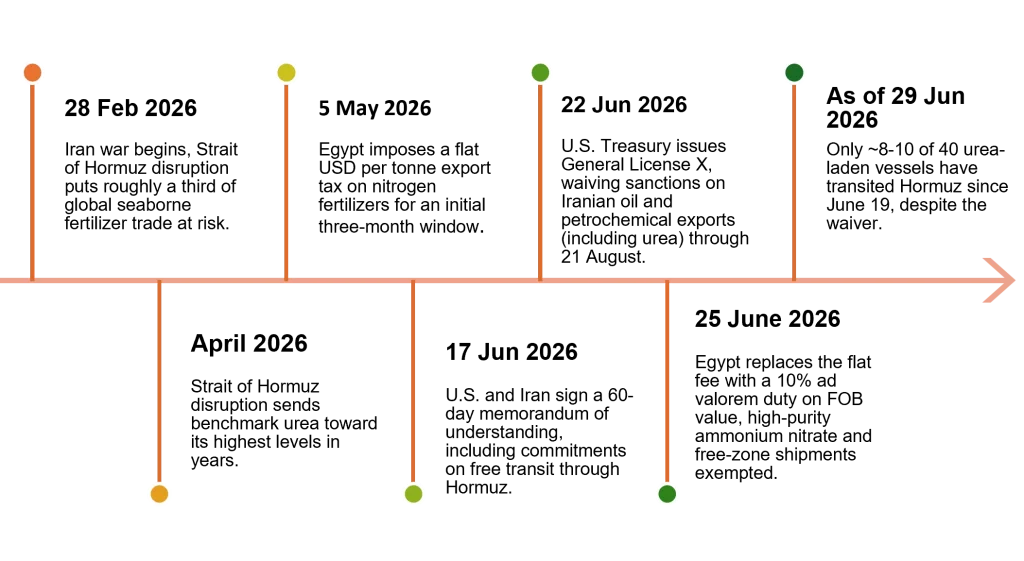

Two policy moves landed within days of each other and reshaped the conversation in nitrogen fertilizer markets. On 22 June, the U.S. Treasury issued a sweeping sanctions waiver General License X authorizing the production, delivery, and sale of Iranian-origin crude oil, petrochemical products, and petroleum products, urea among them, through 21 August.

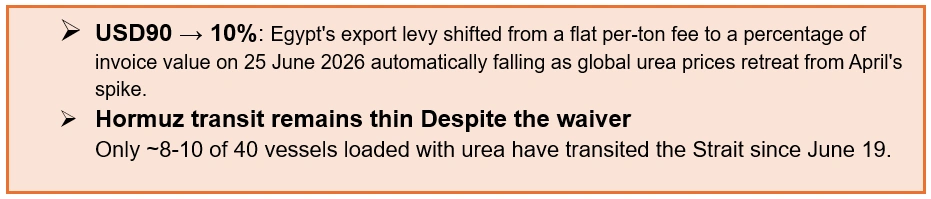

Three days later, Egypt replaced its flat 90 USD/MT nitrogen export tax with a 10% duty on invoice value. Both are downstream effects of the same shock.

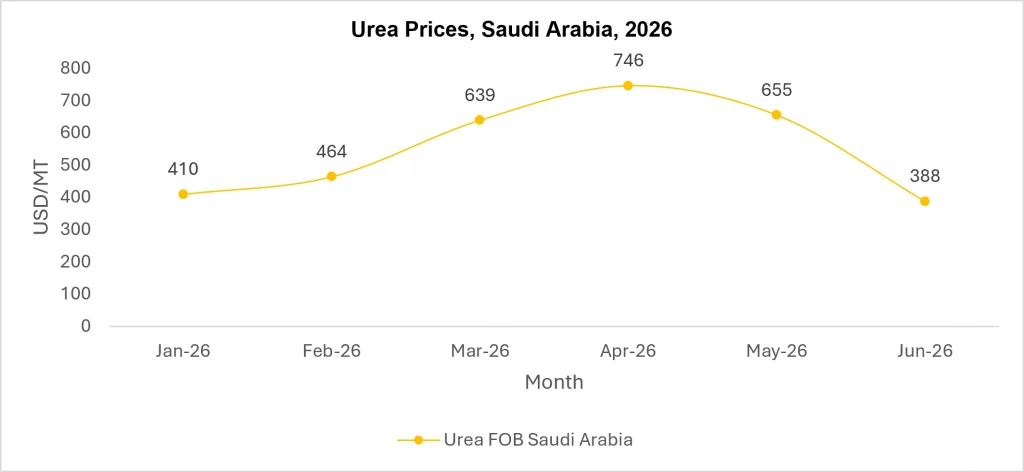

The Strait of Hormuz disruption that followed the February 2026 Iran war, which removed roughly a third of global seaborne fertilizer trade from the market overnight and sent benchmark urea spiking above USD 800/MT by April globally.

Iran matters disproportionately here. Despite incomplete official reporting due to decades of sanctions, industry estimates place Iran as the largest single urea exporter in the Gulf region, with the broader Hormuz-constrained corridor accounting for roughly 30% of global urea trade.

A genuine reopening of that supply at the discount pricing sanctioned-but-desperate sellers typically offer would be one of the more consequential swing factors in nitrogen markets this year.

Shipping Constraints Continue Limiting Iranian Exports

But the legal waiver and the physical reality are two different things. Despite the License X authorization, only ~8-10 of 40 vessels loaded with urea have transited the Strait since June 19.

Insurers, shipowners, and traders are still pricing real risk to the corridor, regardless of what Washington’s paperwork now permits.

That gap between legal access and physical throughput is the central tension in the nitrogen market right now. The waiver removes a regulatory barrier, but it does not remove a tanker’s exposure to mines, missiles, or a naval incident in the strait. Egypt is sitting loaded and ready, it just isn’t moving at anything like the rate the waiver would suggest is possible.

Egypt has rewritten its nitrogen fertilizer export tax twice in seven weeks, and the second version tells you more about global prices than the first one did.

On 25 June, Cairo scrapped the flat $90-per-tonne export duty it had imposed in May and replaced it with a 10% ad valorem tax on the FOB invoice value, exempting high-purity ammonium nitrate and free-zone shipments.

It is a small bureaucratic change with a large signal embedded in it: the urgency that justified a flat fee in May has eased.

That urgency was real at the time. Urea, the benchmark nitrogen fertilizer, spiked toward its highest levels in years after the de facto disruption of the Strait of Hormuz, a corridor carrying roughly a third of global seaborne fertilizer trade and close to half of all urea exports.

A flat USD 90 tax made sense against that backdrop Egypt wanted a guaranteed revenue floor while global buyers were paying almost anything to secure cargoes.

What Means for Global Nitrogen Prices?

The implication for the broader nitrogen market runs in three parts.

First, the legal reopening of Iranian supply is necessary but not sufficient for price relief as long as only a fifth of urea-laden vessels are willing to run the strait, the bulk of Iran’s potential cargo stays off the water, and the discount pricing that a full reopening would bring stays theoretical rather than real.

Second, both Iran’s waiver and Egypt’s tax design are now pegged to expiring or moving targets the License X authorization runs out 21 August unless renewed, and Egypt’s percentage duty will rise automatically if prices climb again meaning the policy environment itself is a source of volatility, not just a backdrop to it.

Third, Egypt’s pivot to a market-linked tax, alongside Russia’s separate export caps for June through November, suggests major nitrogen exporters are positioning for continued swings rather than betting on a settled price floor, even as the headline trend points down from April’s peak.

Source: Price Watch™ Urea Prices

The picture has since shifted. The benchmark urea contract has pulled back sharply from its April highs, and regional spot prices have softened too Northeast Asia and Africa were both down double digits month-on-month through June, even as Middle East FOB levels held firmer on steady export demand.

A fixed-dollar tax in a falling market becomes a heavier relative burden over time, a percentage-based tax automatically lightens as prices ease.

That is precisely why Egypt switched, it keeps Egyptian urea price-competitive against Gulf, Russian, and Chinese supply without giving up the tax revenue altogether.

Egypt’s tax regime, modeled

A flat USD 90/tonne fee and a 10% ad valorem duty only cost an exporter the same amount at one price, USD 900/tonne. Below that breakeven which is where the market has traded for nearly all of 2026. The new regime costs Egyptian exporters less than the old one did.

The Takeaway for Buyers and Traders

Treat the April-to-June price retreat as a partial unwind, not a resolution. The paper authorization to trade Iranian urea exists, the ships willing to carry it largely don’t yet.

Until transit volumes through Hormuz rise meaningfully, the discount Iranian supply could theoretically offer the market stays mostly off the table and the 21 August waiver expiry is now a hard deadline worth watching, since a lapse without renewal would remove the legal pathway again just as abruptly as it appeared.

For more such details visit Price Watch™ Our platform delivers real-time data and expert analysis, offering deep insights into the key factors driving price fluctuations in the fertilizer (DAP, Ammonia, Sulphur, Ammonium Nitrate, SSP, Urea, TSP etc) market.

By tracking critical events such as geopolitical tensions, supply chain disruptions, and economic shifts, Price Watch™ keeps you fully informed of market dynamics.

Track Price Watch™ fertilizer price assessment on a weekly basis from 2015 onwards along with short term forecasts and get access to the detailed report in downloadable format.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.