The global Phosphorus market is undergoing a structural shift. In 2026, Phosphorus has become one of the most strategically important chemicals in the global supply chain.

Rising prices for both Yellow and Red Phosphorus are increasing costs across fertilizers, lithium-ion batteries, electronics, and specialty chemicals.

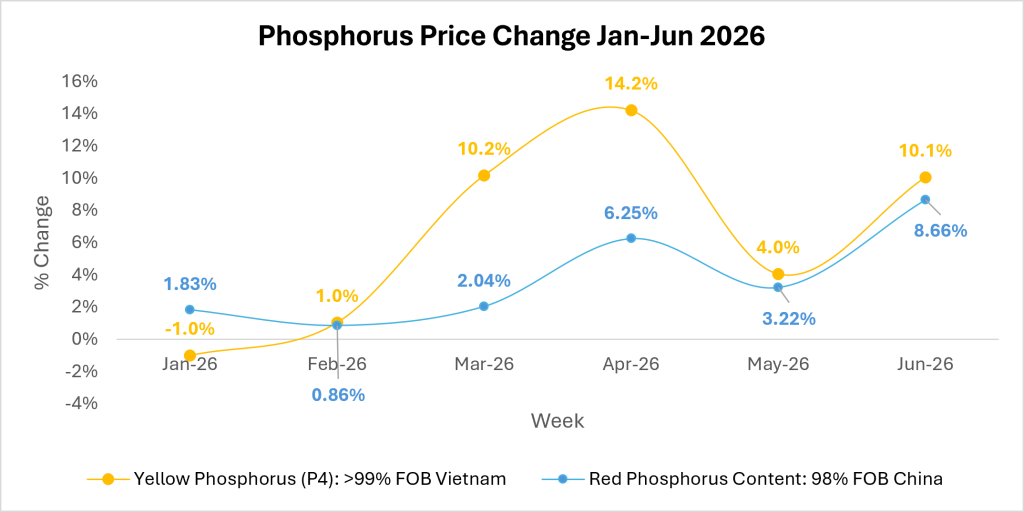

Recent imports into India have reflected this trend, with Vietnam-origin Yellow Phosphorus delivered on a CIF Nhava Sheva basis recording a price increase, forcing downstream manufacturers to reassess procurement strategies.

Unlike previous price cycles, today’s market is being driven by structural changes in both supply and demand.

Source: Price Watch™ Yellow Phosphorus Prices & Red Phosphorus Prices

Yellow Phosphorus Demand Strengthens

Yellow Phosphorus has emerged as one of the most critical raw materials for the energy transition. It is the primary feedstock for phosphoric acid, an essential input for Lithium Iron Phosphate (LFP) batteries that continue to gain market share in electric vehicles and stationary energy storage.

At the same time, agrochemical producers continue to consume large volumes for phosphate-based fertilizers and glyphosate production.

Red Phosphorus Market Remains Firm

Red Phosphorus serves a different but equally important market. Demand from flame retardants, semiconductors, electronic components, and specialty chemicals remains resilient, supported by increasing safety standards and electronics manufacturing.

Supply Constraints Continue to Tighten the Market

The tightening market is largely the result of four converging factors.

First, Vietnam has become an increasingly important supplier for India, but tighter FOB availability, combined with higher freight costs and continued shipping disruptions across major trade routes, has lifted import prices.

Second, although China remains the world’s largest phosphorus producer, exports have become increasingly controlled.

Authorities continue to prioritize domestic industries, particularly battery materials and fertilizer production, while closely managing export volumes.

Production has improved during 2026, but export availability has not expanded at the same pace, limiting material available to international buyers.

Third, geopolitical competition is reshaping procurement strategies. Western economies are actively reducing dependence on Chinese critical materials, encouraging diversified sourcing and strategic inventory building. This has supported buying interest even during periods of improving production.

Finally, production costs remain elevated. Petroleum coke and silica, two essential raw materials for Yellow Phosphorus manufacturing, have remained expensive, while electricity continues to represent one of the largest cost components in phosphorus production.

The downstream impact is becoming increasingly visible. Agrochemical manufacturers face higher raw material costs, while battery producers are placing greater emphasis on long-term supply security rather than simply securing the lowest price.

Electronics manufacturers are also experiencing rising costs for phosphorus-based flame retardants.

Phosphorus Market Outlook

Looking ahead, the market appears unlikely to return to the pricing environment seen several years ago.

Even if logistics improve and short-term supply pressures ease, the combination of battery demand, fertilizer consumption, controlled Chinese exports, and higher production costs suggests that phosphorus prices are likely to remain structurally stronger than in previous market cycles.

The question for buyers is no longer whether supply will improve, but whether enough new capacity can be developed to keep pace with demand from both agriculture and the global energy transition.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.