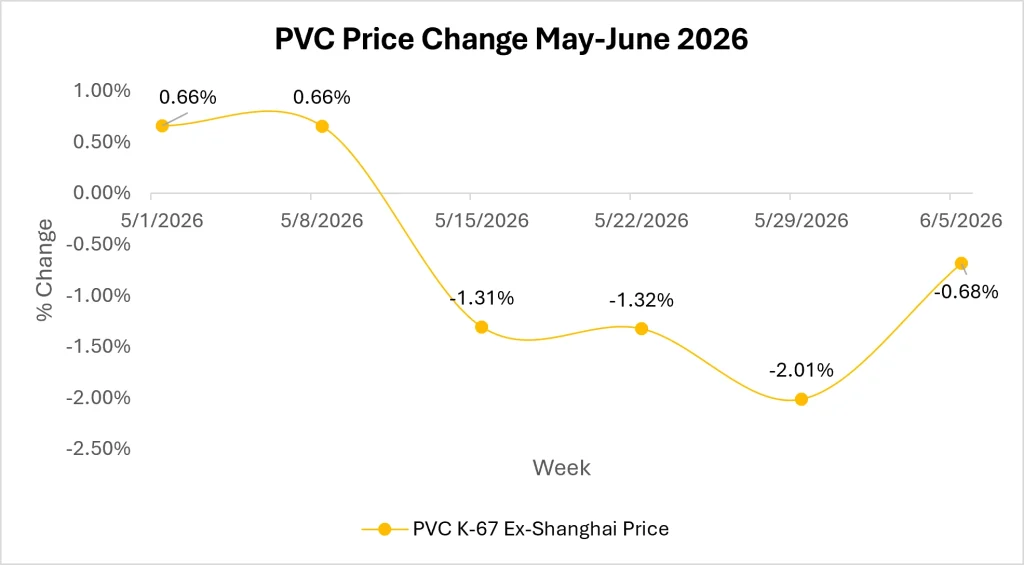

In June 2026, China PVC prices moved lower after an earlier supply-driven rally lost momentum, with downstream buyers reducing fresh procurement and focusing on inventory management. The correction followed weeks of strong purchasing activity that had been supported by feedstock concerns and geopolitical uncertainty surrounding the ongoing U.S.-Iran conflict.

China PVC Prices Soften as Supply-Driven Rally Loses Momentum in June 2026

Earlier in the cycle, supply concerns across the regional ethylene chain supported China PVC prices. Shutdowns at major South Korean crackers, including YNCC, tightened feedstock availability, while disruptions linked to the Strait of Hormuz raised concerns over naphtha imports and regional raw material supply.

In addition, Zhejiang Petroleum & Chemical (ZPC) reportedly reduced ethylene production due to lower crude availability from the Middle East, further supporting production costs for ethylene-based PVC manufacturers.

Source: Price Watch™ PVC Prices

China’s carbide-based PVC sector remained relatively insulated from ethylene supply disruptions, as stable domestic calcium carbide availability continued to support production. However, the broader market still benefited from stronger sentiment generated by feedstock uncertainty and higher manufacturing costs.

Stocked-Up Buyers Reduce Fresh Procurement

The market failed to maintain its upward trajectory as many downstream processors had already secured sufficient inventories during the earlier rally. As a result, buyers became increasingly resistant to higher offers, particularly amid moderate demand from construction and infrastructure-related sectors.

Market participants also noted that despite ongoing geopolitical tensions, no major physical supply shortages emerged in the PVC market. This reduced urgency among traders and converters, leading to weaker spot buying activity and softer negotiations.

PVC Market Sentiment Softens Despite Persistent Geopolitical Risks

Although tensions in the Middle East continue to create uncertainty for energy and feedstock markets, buyers have adopted a more cautious approach. With inventories at comfortable levels and immediate supply concerns easing, purchasing activity slowed across the PVC value chain.

The decline in speculative buying, combined with subdued downstream demand, contributed to softer market sentiment and weighed on overall trading activity.

PVC Market Outlook: Temporary Pause or Start of a Broader Correction?

China PVC price trend is expected to remain cautious in the near term as market participants continue monitoring developments in Middle Eastern energy markets, feedstock availability, and downstream demand. While geopolitical risks could still create periodic cost support, demand fundamentals are likely to remain the key driver of market direction.

The key question remains whether the current decline represents temporary buyer caution after earlier stock-building activity or the beginning of a more sustained demand slowdown across China’s PVC value chain.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.