Over the past week, the stainless-steel market has shown a mild but noticeable upward movement. Prices haven’t surged dramatically, but there’s been a steady, gradual increase reflecting slightly firmer costs and consistent buying interest from downstream industries.

This gentle rise comes at a time when demand from sectors like construction, manufacturing, and the electric vehicle supply chain remains stable, helping to keep the market supported. At the same time, overall trading activity has stayed relatively cautious, suggesting that both buyers and sellers are still watching for clearer signals before making bigger moves.

For now, the trend points to a slow recovery rather than a breakout rally, leaving the market in a balanced but slightly firmer position compared to the previous week.

What Drove the Shift in Stainless Steel HRC prices?

-

Indonesia’s Nickel Quota Squeeze

A lot of the initial price jump came down to suppliers passing on massive raw material costs. To counter tighter regional mining quotas for nickel ore, smelters and mills were forced to pay heavy premiums for their feedstock.

The focus shifted entirely to protecting margins, which naturally pushed spot prices higher across the region.

-

Sulphur Bottlenecks & Geopolitical Strain

The market’s cost base was further pressured by sulfur shortages. Disruptions to trade flows through the Strait of Hormuz tied to broader Middle Eastern tensions sharply increased the cost of sulfur, an essential component for processing battery-grade nickel and smelting ores.

This logistical bottleneck forced production cuts at several key processing plants, keeping alloy supplies tight.

-

Weak Demand Elasticity

Even with the threat of looming shortages, end buyers did not really bite on the higher prices. Folks in the traditional construction and white goods sectors played it incredibly safe.

Instead of panic-buying to secure future inventory, they adopted a strict “wait-and-see” approach, only buying exactly what they needed to keep their daily operations running.

-

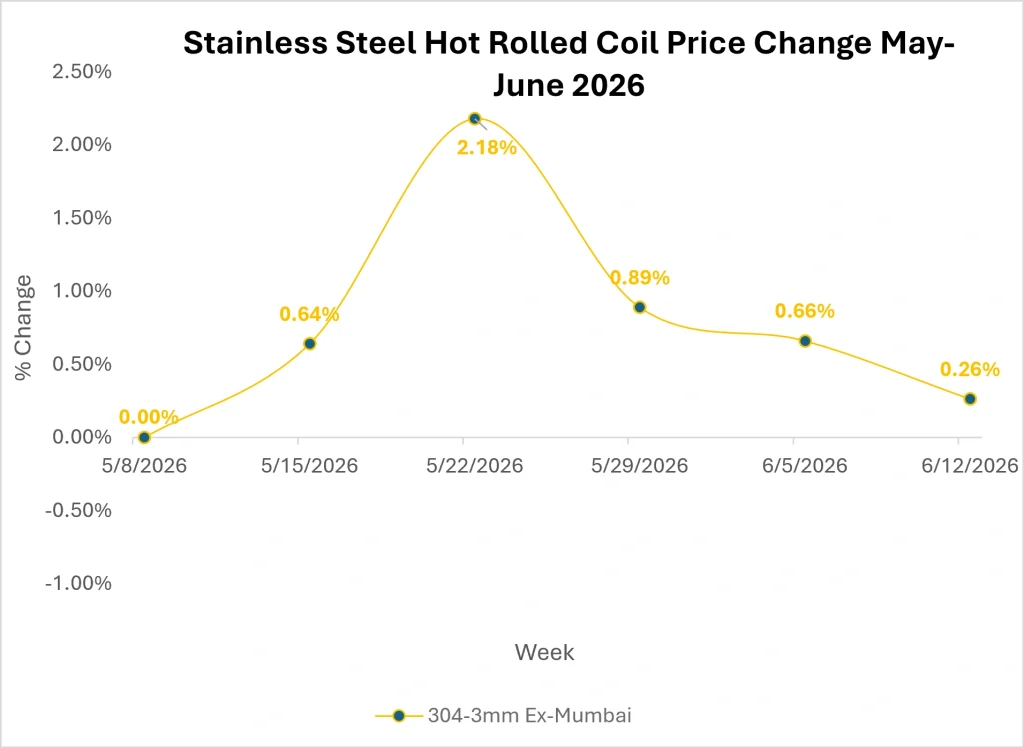

The Rally is Levelling Off

If we look at the week-by-week breakdown, the upward momentum seems to be stopping.

Source: Price Watch™ Stainless Steel HRC Prices

As seen in the data, the steep mid-period price hikes have decelerated sharply. The final 1% reading last week tells us the market is finally finding its new ceiling. That aggressive push from suppliers to hike prices largely dried up as they hit a wall of buyer resistance, meaning they could no longer force higher premiums without killing trade volume.

At the same time, regional mills successfully integrated more scrap into their supply chains over the recent period, helping to cap production costs. With fewer buyers willing to chase the rally last week, the aggressive upward momentum naturally levelled out, providing a solid resistance ceiling against further steep price jumps.

The Bottom Line for Investors & Industry

For investors and industry players, this looks like a classic period of cost absorption rather than a fundamental boom in demand. Yes, there is some near-term pressure as raw materials remain tight, but the underlying need for stainless steel ensures prices will not easily retreat back to old lows.

Stainless Steel Market Outlook

Looking ahead, expect Asian stainless steel prices to stay a bit elevated but mostly flat as the dust settles from the recent corrections. We are not going to see prices fall off a cliff because the baseline demand especially from infrastructure projects and robust industrial manufacturing is just too strong to ignore.

Right now, the market is simply trying to find a fair middle ground between hesitant buyers and suppliers who are battling high input costs. Buyers will likely keep their cards close to their chest this week, paying premiums only when they absolutely must.

Once the current cycle of scrap utilization maxes out and considering that regional raw material quotas remain incredibly tight, cost pressures could eventually trigger another upward phase.

If global energy costs spike again, or if downstream manufacturing hits a sudden seasonal boom, prices could easily break out of this flatline. But until we see buyers actively returning to restock in bulk, expect things to remain cautious and steady at these new, higher levels.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.