Global aniline markets remained increasingly fragmented through Q2 2026 as producers across Europe, Asia, and North America struggled to balance rising Benzene and Nitric Acid feedstock costs against uneven downstream demand recovery.

While upstream aromatic volatility intensified globally, several regions avoided aggressive aniline price increases to protect long-term polyurethane contracts and preserve downstream customer retention.

Instead of fully transferring feedstock inflation into the spot market, many producers absorbed rising conversion costs internally, resulting in severe cash margin compression across the Benzene → Nitrobenzene → Aniline value chain.

What Was the Most Unusual Aniline Market Movement?

The biggest anomaly was the divergence between regions:

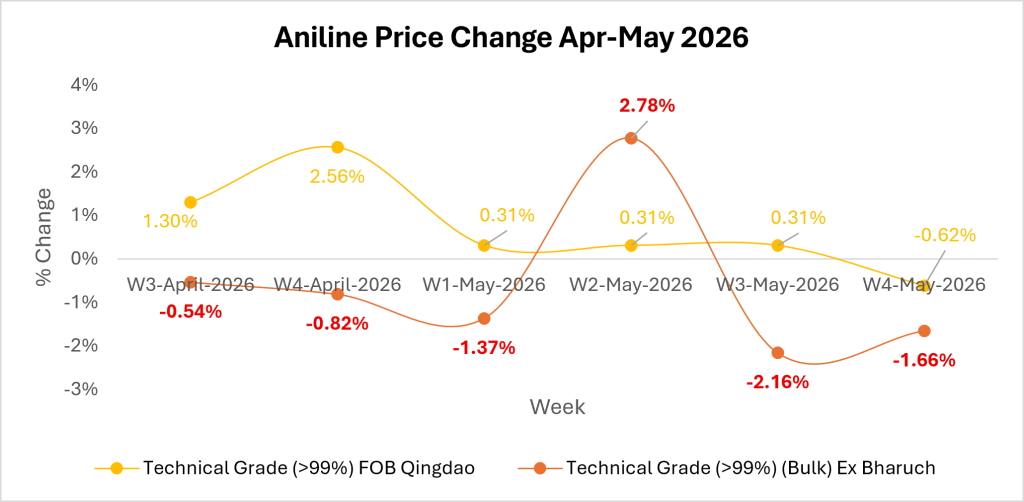

- FOB Qingdao strengthened intermittently due to tighter domestic Benzene availability, improving export inquiries, and stronger integrated operating rates across Chinese chemical complexes.

- Ex Bharuch witnessed repeated fluctuations driven by inventory corrections, import competition, and cautious procurement activity from domestic downstream buyers.

- FD Antwerp remained comparatively stable despite worsening European production economics and elevated feedstock pressure.

Source: Price Watch™ Aniline Prices

How Did the Benzene-to-Aniline Chain React?

The Benzene → Nitrobenzene → Aniline chain became increasingly imbalanced:

- Elevated aromatic feedstock costs increased conversion pressure.

- Weak construction-linked MDI demand reduced pricing power.

- Automotive polyurethane demand provided only partial support.

As a result, standalone aniline producers faced greater vulnerability compared to integrated MDI manufacturers.

Why Does Hydrochloric Acid (HCl) Matter in the Aniline Market?

A lesser-known pressure point emerged from the product HCl management. Weak regional demand for hydrochloric acid across Europe reduced disposal flexibility, indirectly affecting MDI operating rates. This created operational constraints even when downstream demand remained stable.

Short Term Aniline Market Outlook

European producers may reduce operating rates further if:

- Benzene prices remain elevated

- Housing and insulation demand stays weak

- Chinese exports continue increasing into Western markets.

The market now appears driven more by integration efficiency than pure demand recovery.

Are stable aniline prices reflecting genuine balance or are producers temporarily sacrificing margins to defend market share before a larger correction emerges?

For deeper chemical spread analysis and procurement intelligence, follow Price Watch™.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.