Three forces. One structural break. The Iran conflict has spiked fossil fuel prices, compressing the SAF (Sustainable Aviation Fuel) cost premium almost overnight. Southeast Asian blending mandates are escalating faster than domestic production chains can absorb.

And a new wave of non-food feedstock alliances, from camelina in North America to forestry biomass in China, is quietly repositioning who controls supply into the 2030s. The result is not a uniform move in biofuel prices. It is a divergence and buyers positioned for a single-direction trade are already misread.

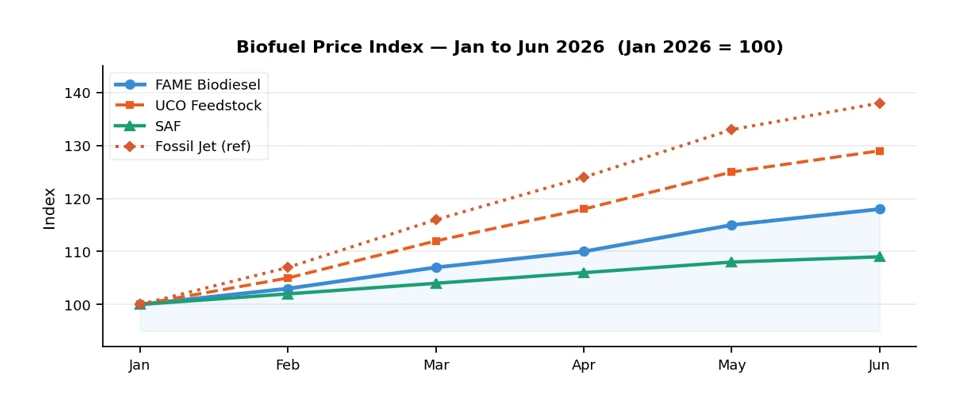

Biodiesel & SAF Prices – Mandate Floors vs. Open-Market Pressure

Fig. 1 – Biofuel price index Jan–Jun 2026 (Jan = 100). UCO feedstock outpaces FAME finished product.

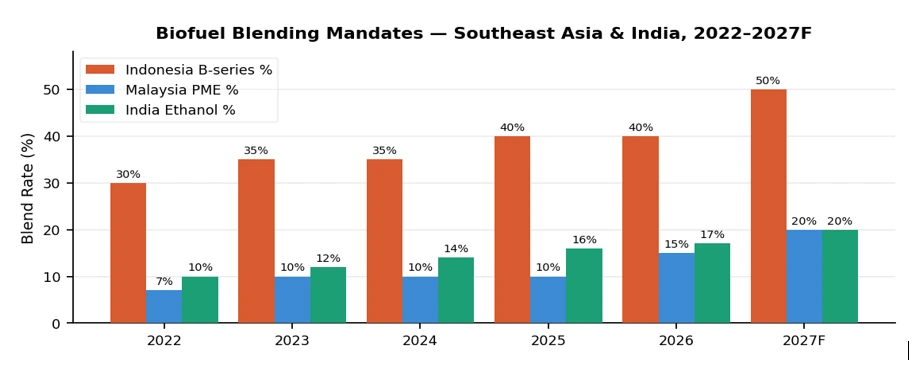

Blending Mandates – Southeast Asia & India Trajectory

Fig. 2 – Blending mandate escalation: Indonesia B-series, Malaysia PME, India ethanol (2022–2027F).

Indonesia requires an estimated 26 billion litres/year of biodiesel capacity to reach B50 – nearly double current installed capacity. Malaysia at B15 absorbs palm methyl ester (PME) supply that was previously available for European spot buyers. India at 16.9% ethanol blending (targeting 20% ahead of schedule) has already documented ₹91,000 crore in cumulative import savings – a volume signal that tightens regional molasses and sugar feedstock markets globally.

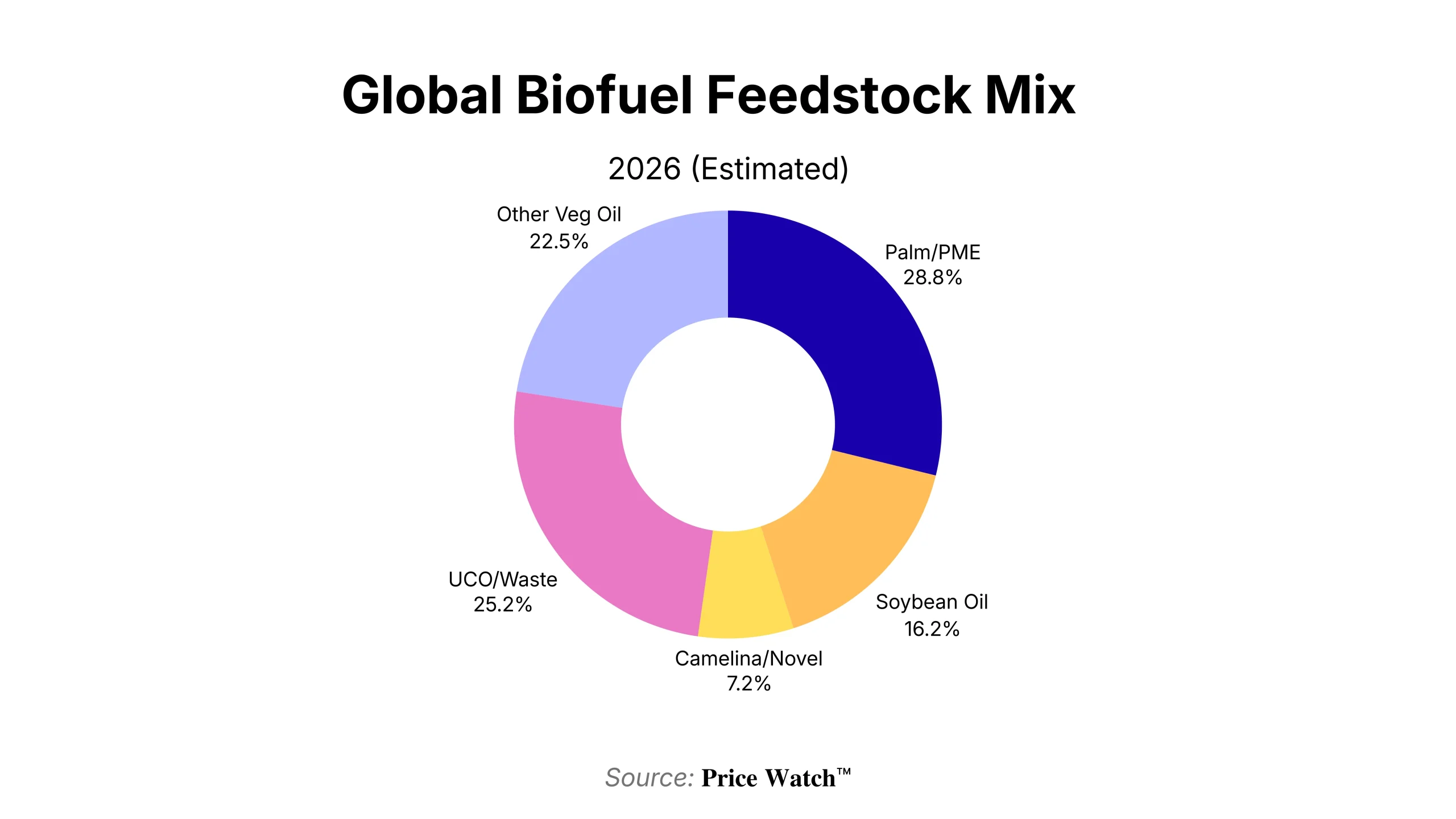

Feedstock Mix & the Camelina Acceleration

Fig. 3 – Estimated global biofuel feedstock split 2026. Camelina/novel feedstocks remain sub-10% but are the fastest-growing share.

Palm and UCO together account for roughly 60% of global biofuel feedstock. Both are now under supply-side pressure. Indonesia’s move to centralize palm oil exports under state-controlled pricing introduces new uncertainty around RPOME availability for European advanced quota buyers – a route disruption that can move ARA premiums independent of broader palm direction.

Meanwhile, Bayer’s accelerated camelina programme – targeting ~2 million North American acres in partnership with BP, with a crushing deal imminent – is the clearest signal that the feedstock mix is structurally shifting.

A timeline originally set for the mid-2030s has been pulled forward. Beijing Haixin Energy’s forestry-chemistry SAF collaboration with China’s ICIFP adds a second non-food pathway entering commercial development.

Geographic Routes: Barcelona-Shanghai and the India Corridor

Barcelona-Shanghai formalised a “sister port” agreement on June 11, covering alternative marine fuel development, green port infrastructure, and a sustainable corridor linking the Far East with the Mediterranean.

This builds on Repsol’s existing 8-year renewable marine fuel contract with Norwegian Cruise Line Holdings at Barcelona – a live commercial anchor on that corridor. Hong Kong bunkered 60,000 mt of green marine fuel in January through May alone, confirming Asia-Pacific marine biofuels are active, not aspirational.

The Indonesia-to-Europe RPOME route is the hidden risk. Jakarta’s export centralization – framed as anti-fraud by Danantara – has made pricing and volume opaque for European buyers relying on RPOME for advanced biofuel quota compliance. Buyers without alternative sourcing plans face a narrowing window.

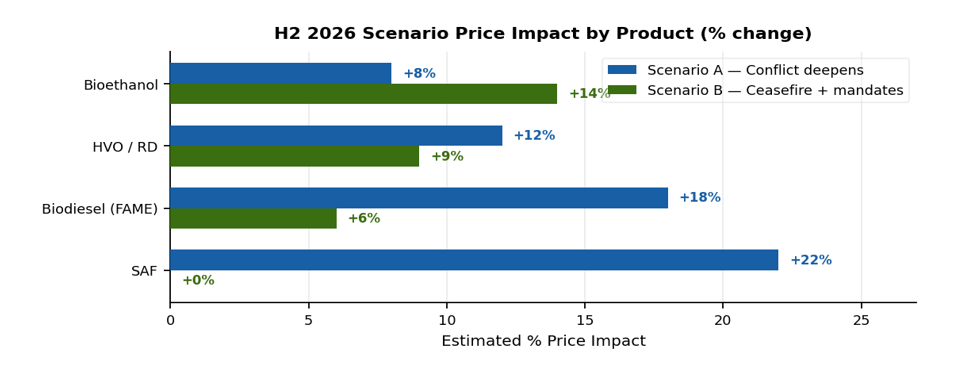

H2 2026 Scenario Outlook – Biofuels Price Impact

Fig. 4 – Two-scenario H2 2026 price impact by product. Scenario A: conflict deepens. Scenario B: ceasefire + mandate expansion.

- Scenario A – Conflict deepens: SAF faces +22% price pressure as fossil jet stays elevated but EU mandates hold SAF offtake. FAME gains +18% on mandate absorption and constrained RPOME supply. HVO softens relative to FAME as blenders optimise toward cheaper B7 blends.

- Scenario B – Ceasefire + mandate expansion: Fossil jet retreats, the SAF premium argument resumes, and deferred non-mandatory offtake returns. Bioethanol is the outperformer at +14% as EU cash prices continue firming on genuine structural tightness. FAME holds a +6% floor regardless – policy mandates do not reverse with the energy cycle.

Decision-Point Questions

- If your H2 SAF offtake model was built on a stable fossil-jet reference, has that assumption been rebuilt to reflect Hormuz-driven volatility?

- If significant FAME sourcing routes through Indonesian RPOME without an alternative supply plan, the window to diversify is narrowing – what is the contingency timeline?

Follow Price-Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.