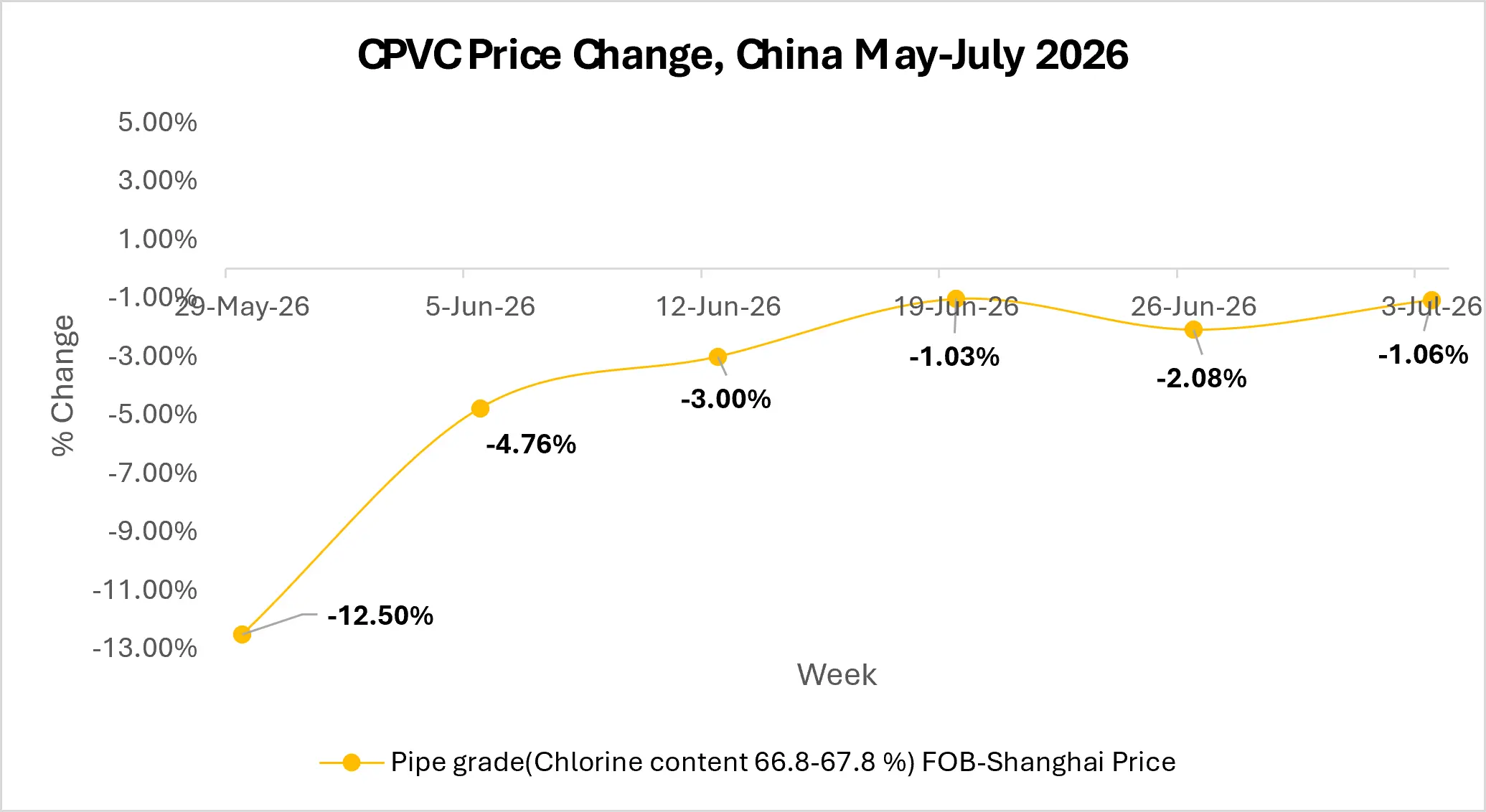

In June 2026, CPVC prices in China remained under sustained pressure, with Pipe Grade CPVC (Chlorine Content: 66.8–67.8%) continuing their downward trend after a sharp correction in late May 2026.

Crude oil prices declined as ceasefire developments between the United States and Iran eased concerns over disruptions to Middle Eastern oil supplies.

Source: Price Watch™ Chlorinated Polyvinyl Chloride Prices

The reopening of the Strait of Hormuz restored confidence in regional energy exports, while OPEC+ continued increasing production by gradually unwinding its voluntary output cuts, improving expectations of ample global Crude availability.

The decline in Crude oil prices reduced production costs across the petrochemical value chain, weakening cost support for CPVC producers and reinforcing the softer pricing environment.

Softer Feedstock Costs Pressure Producers

Lower Crude oil values filtered through the chlor-alkali chain as softer PVC resin and chlorine prices reduced manufacturing costs for CPVC producers. Lower energy costs also eased operating expenses, making it increasingly difficult for suppliers to justify higher offers.

Adequate domestic PVC resin availability ensured sufficient raw material supply, preventing any meaningful cost-driven recovery. As feedstock costs softened, producers increasingly relied on competitive pricing to protect sales volumes amid cautious market sentiment.

Construction Demand Continues to Weigh on CPVC Market

Despite improved production economics, CPVC prices in China continued moving lower as demand from construction, infrastructure, and pipe manufacturing sectors remained subdued.

Pipe manufacturers purchased material only for immediate production requirements instead of rebuilding inventories, while distributors delayed fresh purchases in anticipation of further price corrections.

Weak construction activity, slower project execution, and comfortable inventories across the supply chain reduced consumption in the pipe and fittings segment, limiting opportunities for suppliers to stabilize prices. Moderate export demand also failed to provide meaningful support to the domestic market.

CPVC Buyers Prioritize Inventory Management

As feedstock concerns faded, buyers shifted their focus toward inventory management rather than aggressive procurement. Comfortable stock levels reduced urgency for fresh purchases, weakening spot trading activity and intensifying competition among suppliers.

Consequently, the CPVC price trend in China remained bearish through June and into early July as sellers continued adjusting offers to improve order volumes and reduce inventory pressure.

CPVC Market Outlook

The near-term outlook remains cautious as market participants continue monitoring construction activity, infrastructure spending, PVC resin and chlorine feedstock costs, and Crude oil movements.

While geopolitical developments may continue influencing energy markets, downstream demand is expected to remain the primary driver of pricing.

The bigger question is this: Is the recent decline simply the result of cautious buying and inventory adjustments, or does it indicate a more prolonged slowdown across China’s construction and pipe manufacturing sectors?

Price Watch™ continues tracking weekly movements across the CPVC value chain.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.