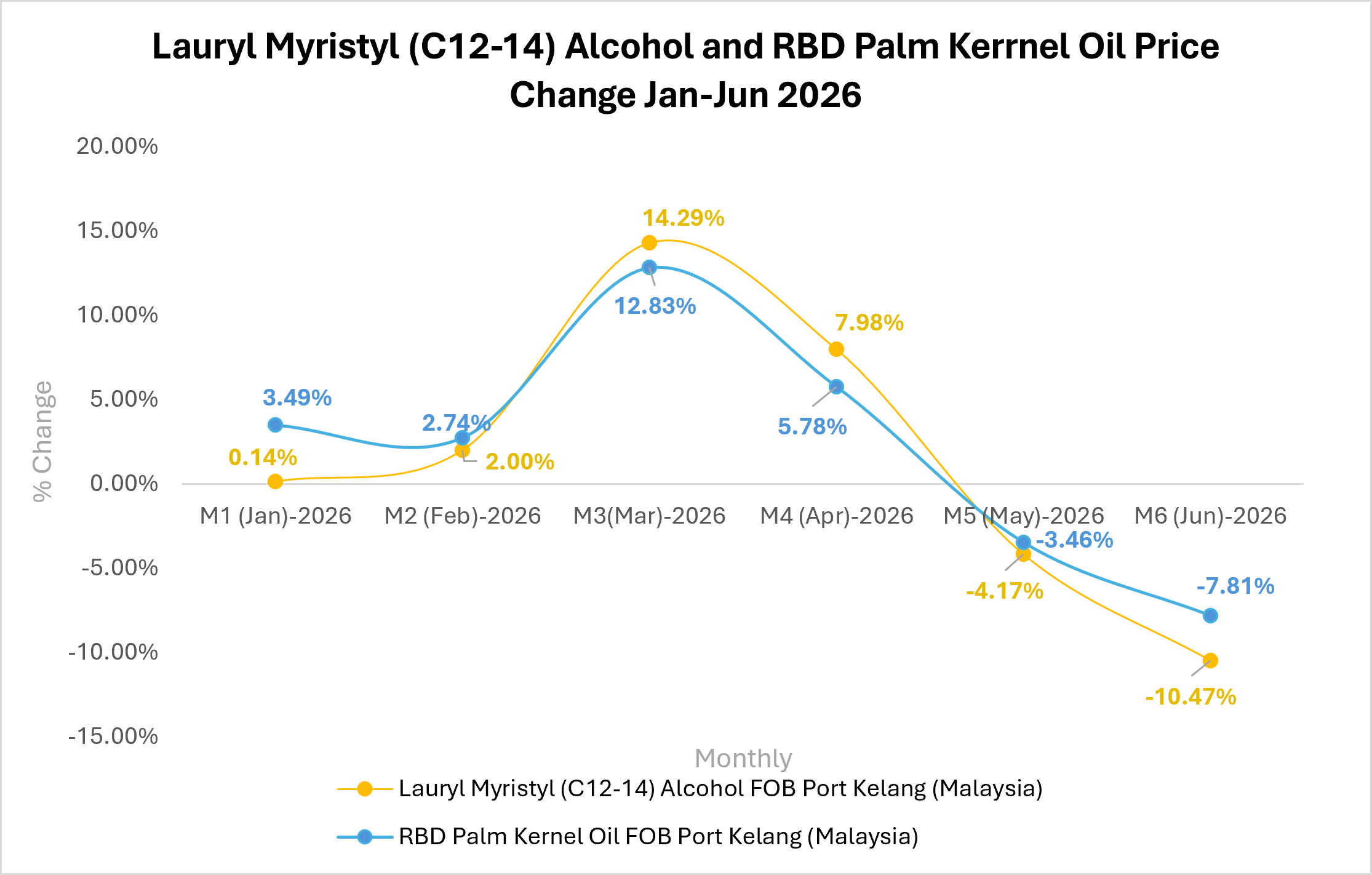

Every tonne of Lauryl Myristyl Alcohol carries a hidden multiplier. Producers need roughly 1.7 tonnes of palm kernel oil to make a single tonne of C12-14, which is why Malaysia, holder of about 20% of global oleochemical capacity, feels every tremor in the kernel market three times over.

Through May and June 2026 those tremors pointed downward. Market experts reported in mid-May that Asian demand for mid cut C12-14 was fading as palm kernel oil costs declined and Indonesian supply lengthened. Buyers who chased cargoes through 2025 suddenly found sellers calling them first.

Source: Price Watch™ Fatty alcohol Prices

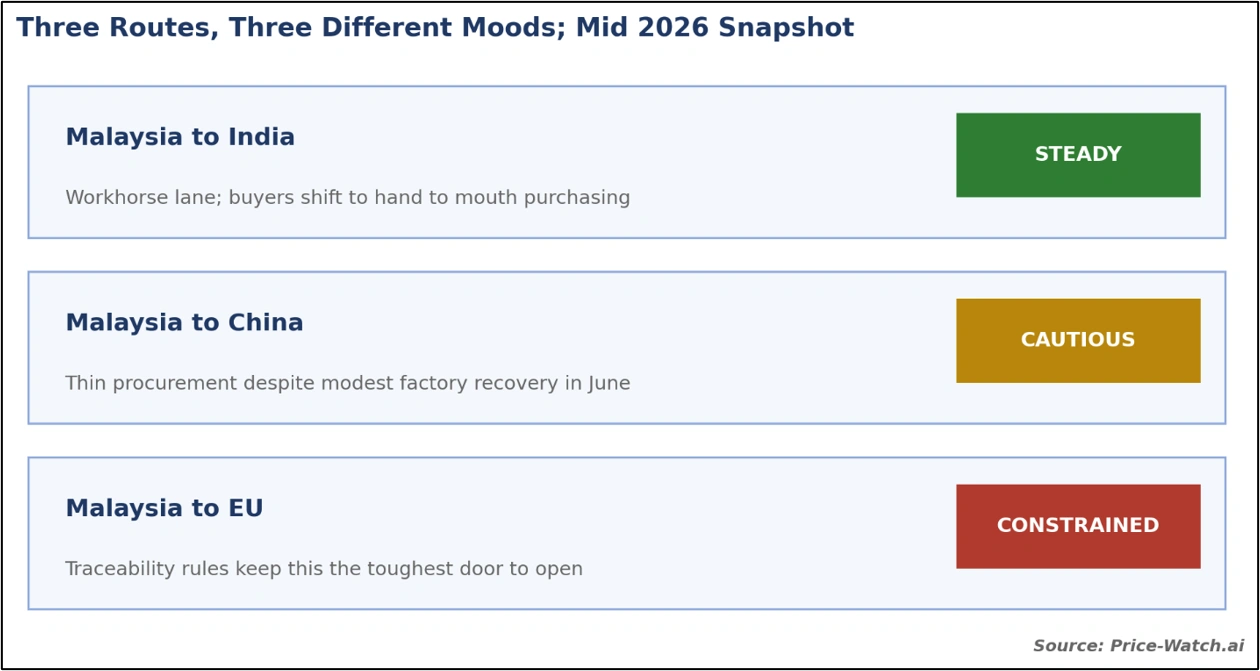

Three Routes, Three Different Moods

The Malaysia to India lane stayed the workhorse, though buyers there shifted to hand to mouth purchasing once softer kernel values appeared. China stayed the quiet giant; procurement remained thin even as its manufacturing activity returned to modest growth in June.

The Europe route stayed the most expensive door to open.

Since the EU Deforestation Regulation took force on December 30, 2025, only fully traceable MSPO and RSPO backed cargoes clear without friction, and EU bound palm derivative volumes had already dropped about 12% in 2025.

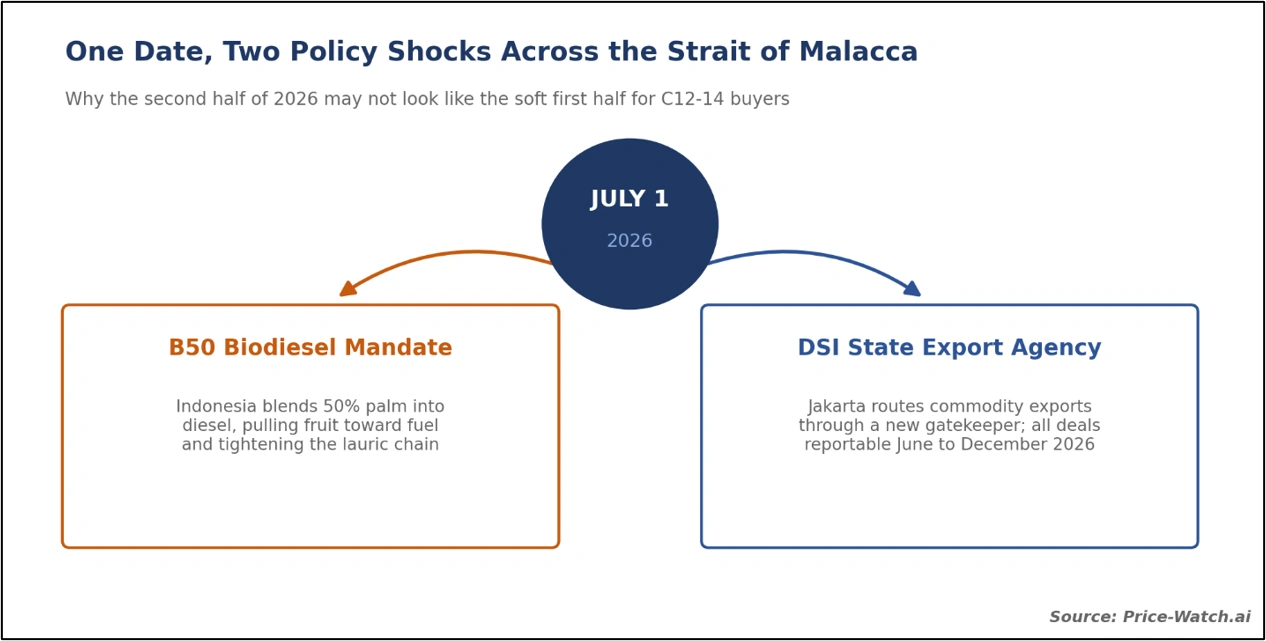

Indonesia Policy Changes Reshape Supply

Two policy shocks landed on July 1, 2026, both from across the Strait of Malacca. Indonesia switched on its B50 biodiesel mandate, pulling even more palm output into fuel tanks.

On the same calendar page, Jakarta began routing commodity exports through a new state agency, DSI, with all such export transactions reportable to it between June and December 2026. Meanwhile Malaysian crude palm oil held near $1065-1130 per tonne, and June 1 to 25 exports ran 10.6% to 11.1% above May.

Here is the factor few buyers price in. Palm kernels are a byproduct of palm oil milling, so kernel oil supply expands only when fruit crushing expands, never because C12-14 demand asks it to.

When B50 redirects fruit toward biodiesel economics, the lauric chain tightens silently.

Fatty Alcohol Market Outlook

Scenario one; Indonesian length keeps winning, kernel costs drift lower, and C12-14 stays soft into the fourth quarter. Scenario two; B50 absorption plus DSI export friction squeezes kernel availability, and the May softness proves to be the floor, not the trend.

So the real question for procurement desks is simple.

Are you reading the current dip as relief, or as the calm before Jakarta’s policies bite? Weekly tracking through Price Watch™ will show which scenario is winning long before the quarterly averages do.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.