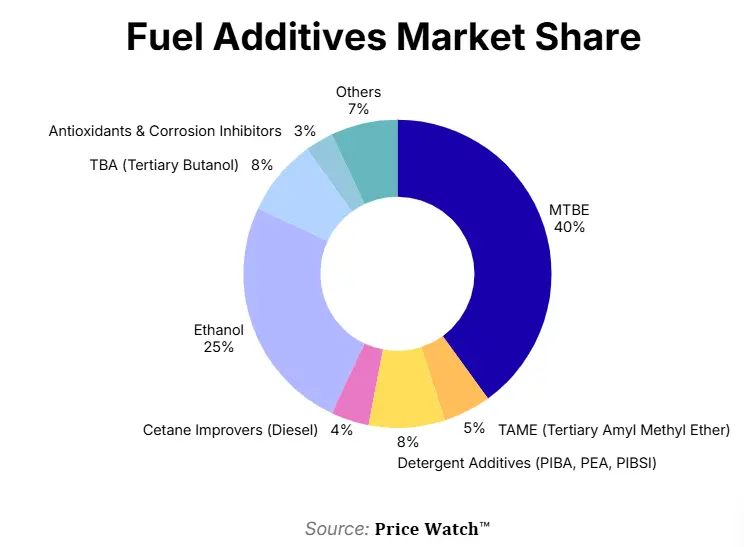

The global fuel additives market is entering a new phase as the geopolitical premium that drove prices higher during March and April 2026 gradually unwinds. MTBE (Methyl Tertiary Butyl Ether) and Tertiary Butanol (TBA), two key raw materials used in gasoline blending and oxygenated fuel additives, experienced significant price increases earlier this year as escalating tensions involving Iran, Israel, and the United States raised concerns over potential disruptions to crude oil supply and Middle Eastern shipping routes.

However, the recent talks of Iran-U.S. and growing expectations of stable energy flows have reversed much of this sentiment. As international crude oil prices moved lower, fuel additive markets across China, the United States, and Europe began correcting from their elevated levels.

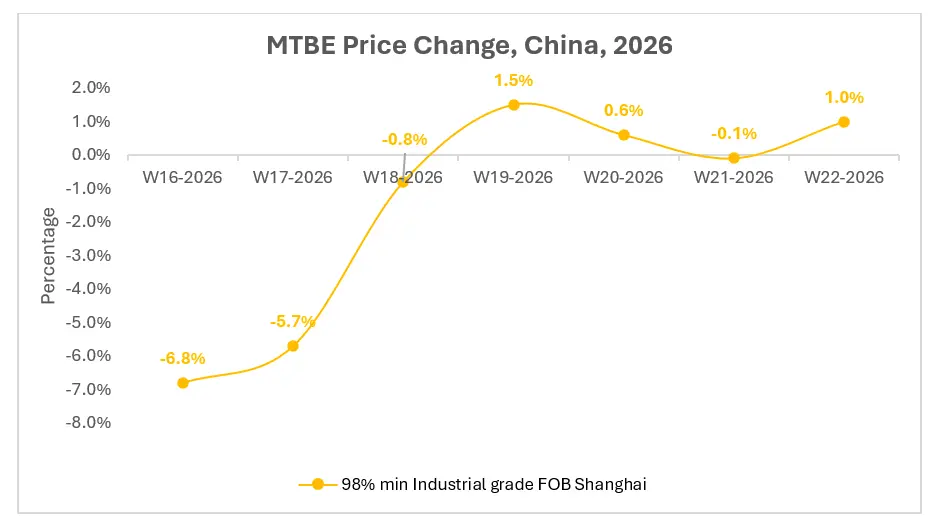

China: MTBE Rally Loses Momentum After April Peak

As the leading MTBE producer globally, China recorded one of the strongest price increases across fuel additive markets between January and April 2026. Supported by rising crude oil prices, geopolitical concerns, and strong gasoline blending demand, MTBE prices increased sharply through April, reaching elevated levels compared to historical norms.

The market began to reverse course after April as international crude oil prices weakened and concerns over Middle Eastern supply disruptions eased. While operational shutdowns at Zhonghaojian, Dongying Shenchi, and Oriental Hongye limited MTBE production, these supply-side constraints were insufficient to offset the bearish impact of falling feedstock costs. The restart of production at Huayi Chemical further eased supply concerns. Consequently, MTBE prices moved lower as downstream fuel blenders adopted a cautious procurement strategy and maintained lean inventories.

A notable shift was also observed in the Tertiary Butanol (TBA) market. Following the price surge triggered by the escalation of the Iran–U.S. conflict, TBA prices underwent a downward correction this week due to subdued buying interest and weaker demand from oxygenated fuel additive manufacturers. This suggests that the correction is expanding across the broader fuel additives value chain rather than being confined solely to MTBE.

Source: Price-Watch™ | MTBE Prices

United States MTBE Market Tracks Crude Oil Weakness

In the United States, the downward shift in MTBE prices became evident from the beginning of May 2026. The decline closely mirrored movements in crude oil markets, which softened as diplomatic signals indicated improving prospects for regional stability and uninterrupted energy shipments.

Despite strong refinery operations, the fuel additives market remained under pressure. U.S. refiners continued operating at high utilization rates, while gasoline and distillate fuel production increased. However, declining feedstock costs and expectations of further price corrections discouraged aggressive purchasing activity among fuel blenders and traders. As a result, MTBE prices moved lower even as downstream fuel production remained healthy.

European MTBE Market Faces Similar Challenges

The European fuel additives market followed a similar trajectory, with MTBE prices beginning to decline from early May 2026. The primary catalyst was the fall in international crude oil prices, which reduced production costs for gasoline additives and encouraged expectations of additional price adjustments.

At the same time, buyers became increasingly hesitant to secure volumes at previously elevated levels, preferring to delay purchases in anticipation of further market weakness. Although gasoline blending requirements remained relatively stable, the decline in feedstock costs outweighed demand support, resulting in a broad-based correction across the MTBE market. This trend reflects the growing influence of crude oil movements on regional fuel additive pricing dynamics.

Fuel Additives Market Outlook Hinges on Crude Oil and Inventory Rebuilding

The outlook for the fuel additives market over the coming months will depend largely on the direction of crude oil prices and the sustainability of improving geopolitical conditions. If Iran-U.S. relations continue to improve and global energy supply concerns remain limited, additional downward pressure may emerge.

Three factors warrant close monitoring:

- Crude oil price movements and Middle East geopolitical developments

- Refinery operating rates and gasoline blending margins across major regions

- Inventory replenishment behaviour among fuel blenders and distributors

If crude oil prices stabilize at current levels, MTBE and TBA markets may find support as buyers begin replenishing inventories after months of cautious purchasing.

Any renewed escalation involving Middle Eastern energy infrastructure or shipping routes could quickly restore risk premiums across crude oil, gasoline, and fuel additive markets, reversing recent price declines.

Market participants are closely assessing whether the ongoing downturn is merely the final phase of a post-conflict adjustment or the start of a sustained period of weaker pricing amid declining crude oil costs. Attention is also focused on whether fuel blenders will continue postponing purchases or return to the market to rebuild inventories if prices fall further in H2 2026.

Follow Price-Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.