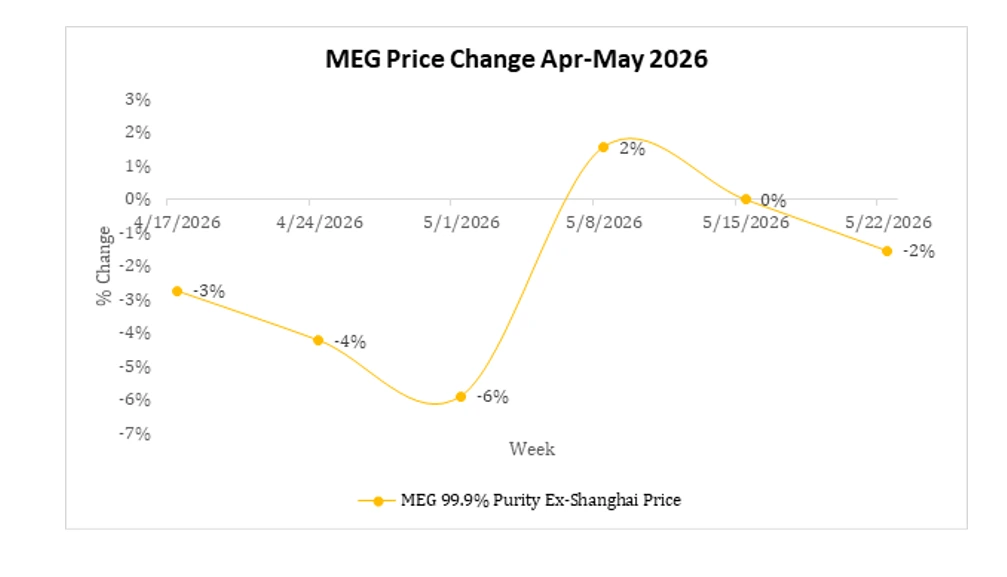

The global MTBE market is witnessing uneven regional movement as Asian prices weaken sharply while the United States and Europe continue holding comparatively firm levels. Singapore benchmark values corrected aggressively during the second half of May after earlier gains, reflecting softer downstream gasoline demand and improving supply availability. At the same time, the US market maintained upward momentum across April and May, while the Netherlands recorded steady monthly gains. The widening spread between Western and Asian markets is now beginning to influence export competitiveness, cargo negotiations, and short-term buying strategies.

The MTBE market in China moved from temporary recovery into renewed weakness during May. Early support came from export purchasing and elevated feedstock costs linked to crude oil volatility and Middle East geopolitical tensions. However, the market lost direction once downstream demand slowed and several manufacturing facilities resumed operations, increasing product availability.

Singapore FOB values declined sharply after May Mid, placing additional pressure on Asian import discussions because Singapore remains the key benchmark for regional trade. Chinese buyers shifted toward cautious short-term purchasing while traders monitored inventory movement more closely. Although high energy and methanol related costs continue offering some support, softer gasoline blending demand is limiting stronger upward movement across the market.

Source: Price-Watch™ MTBE Prices

The US MTBE market showed a stronger trend compared with Asia during the last three months. April registered a major increase followed by another rise in May, supported by relatively tighter domestic availability and firm gasoline blending demand. Meanwhile, the Netherlands market continued recording gradual gains due to elevated energy costs and balanced regional supply conditions. European sentiment, however, remains sensitive to weaker Asian pricing because lower Singapore offers may eventually affect import economics and regional negotiations.

The MTBE market may remain uneven in the coming months. Supply recovery in Asia and cautious downstream demand could continue weighing on sentiment, while elevated energy costs and refinery operating rates may keep Western markets relatively supported.

If Asian prices continue softening while US and European levels stay firm, could global buyers begin shifting sourcing strategies toward lower cost Asian cargoes during the next quarter?

Follow Price-Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.