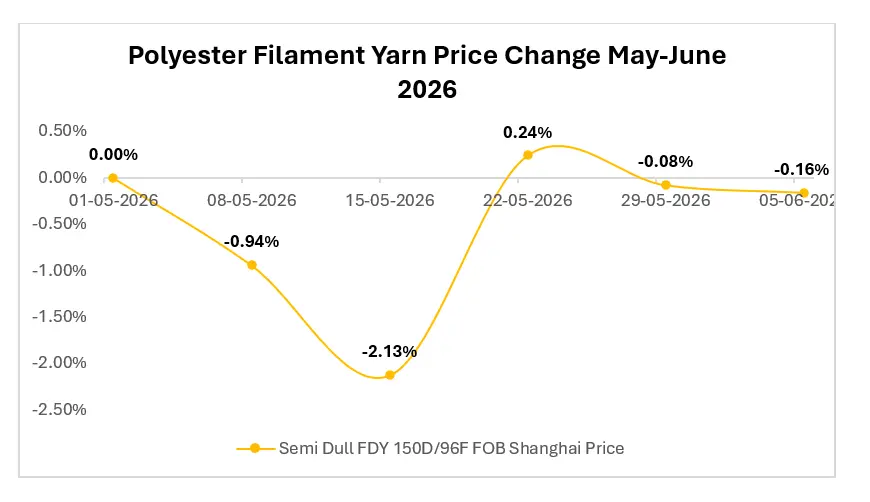

A market that falls for two straight weeks, briefly stabilizes, and then loses momentum again is usually telling you something important. The recent movement in Polyester Filament Yarn FDY 150D/96F FOB China was not a sharp collapse. It was a failed recovery.

What happened to PFY prices in China

The six-week trend shows a clear pattern. Prices declined through early May, with the sharpest correction occurring during the first week of the month. A brief rebound followed, but it failed to gain momentum as buying interest remained subdued.

Since mid-May, FDY 150D/96F prices have largely stabilized and moved within a narrow range into the first week of June, indicating a market waiting for stronger demand before establishing its next direction.

Source: Price-Watch™ | Polyester Filament Yarn Prices

What makes this movement interesting is what happened next.

The market managed a small rebound during the second week of May. Producers attempted to stabilize offers as polyester feedstock costs found temporary support and operating rates were adjusted. Yet buyers showed little urgency to rebuild inventories. The recovery lasted only one week before prices flattened again and gradually weakened.

The message from the market was clear. Sellers could slow the decline, but they could not create enough demand to reverse it.

PFY Value chain pressure points

Two developments shaped the move:

- PTA and polyester feedstock costs stopped falling aggressively, giving FDY producers room to lift sentiment briefly.

- Downstream weaving mills and fabric manufacturers remained cautious, limiting purchases to immediate requirements rather than building stock.

A fresh angle is emerging from this cycle. The issue is no longer production discipline alone. Chinese filament producers have become increasingly willing to manage operating rates, but downstream consumption is not responding with the same speed. That gap is preventing temporary rallies from becoming sustainable trends.

Short term outlook for Polyester Filament Yarn

Over the next one to three months, the key risk remains demand rather than supply. If textile orders continue to lag and fabric inventories stay elevated, any cost-driven support from PTA is likely to have only a limited impact on FDY pricing.

The recent rebound showed that producers can slow a decline. What remains uncertain is whether downstream buyers are ready to signal the beginning of a genuine restocking cycle.

Is the next move in Polyester FDY going to be decided by feedstock costs, or by the first signs of stronger textile demand returning to the market?

To see where that answer may lead prices next, keep tracking the market with Price-Watch™.

Follow Price-Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.