A significant shift is emerging across the global plasticizer value chain, with pricing trends increasingly shaped by prolonged demand weakness and structural inventory imbalances rather than cost-driven shocks.

The stark contrast between the rally observed in March 2026 and the correction seen during May–June 2026 underscores a transition from geopolitically induced inflationary pressures to a more enduring downturn driven by underlying market fundamentals.

The March 2026 surge was triggered by escalating tensions involving Iran, Israel, and the United States, which disrupted logistics expectations and pushed crude oil higher. This immediately lifted upstream petrochemical costs, including DOP and DEG, tightening supply sentiment across Asia and Europe.

However, as geopolitical risk premiums faded and crude oil retreated through May and June, cost support eroded rapidly. The result has been a synchronized price decline across plasticizers, driven less by supply shocks and more by weakening consumption.

Asia-Pacific: From Cost Shock to Demand Compression

In Asia-Pacific, particularly China, the Dioctyl Phthalate (DOP) market has shifted decisively from cost-push inflation to demand-driven decline. Earlier gains supported by elevated propylene costs and energy volatility reversed sharply as feedstock prices fell.

Although periodic tightening in operating rates was observed, it was insufficient to offset weak downstream consumption. Buyers largely restricted procurement to immediate requirements, while surplus availability from earlier contract positions continued to weigh on spot sentiment.

A key structural issue is that DOP pricing is now increasingly decoupled from production cost support, with transaction levels being dictated more by liquidity conditions and inventory overhang than marginal cost economics.

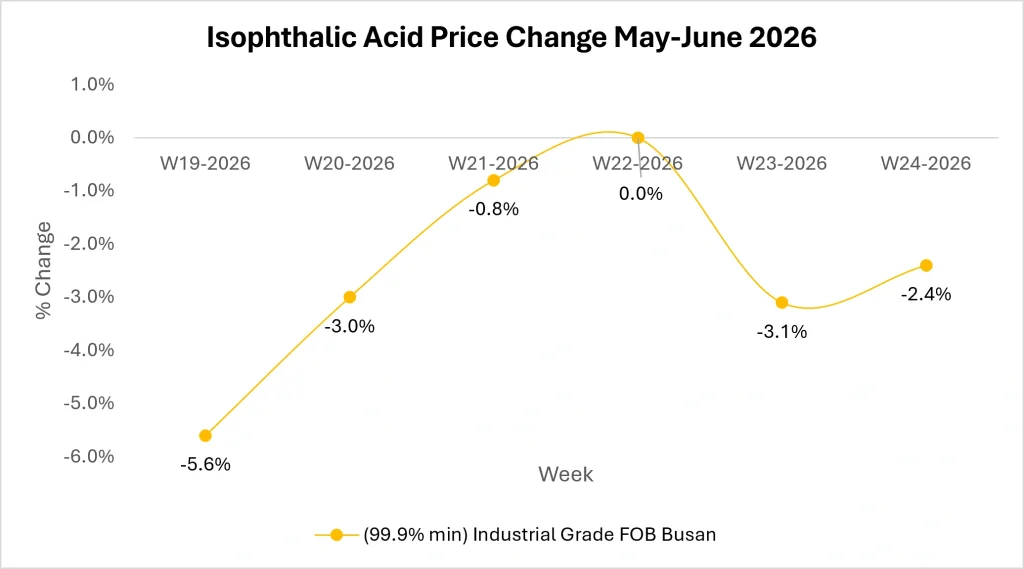

Isophthalic Acid markets in the South Korea have also softened with weak trading environment. Unlike DOP, where feedstock-driven volatility was primary, Isophthalic Acid weakness is being driven by downstream consumption fatigue.

Demand from resin and coatings applications remains subdued, limiting any ability for producers to pass through costs. Even with moderated operating rates, inventory levels remain sufficient, reducing the urgency for spot procurement and reinforcing a buyer-favored environment.

Source: Price Watch™ Isophthalic Acid Prices

Europe: Inventory Cushion Delays Real Demand Recovery

European plasticizer markets are showing a similar but structurally distinct pattern. MEG and DEG demand remain subdued, but the deeper issue is not just weak consumption it is delayed restocking cycles. Many buyers are still working through inventories accumulated during the earlier rally phase.

Despite falling feedstock costs, buying interest has yet to recover. As a result, sellers are cutting prices more aggressively, suggesting that market pricing is being driven more by liquidity pressure than by actual consumption.

Plasticizers Market Outlook

By end-May into June 2026, the plasticizer market has clearly transitioned from a cost-push environment to a demand-constrained cycle.

Lower crude oil and feedstock costs have not translated into margin recovery; instead, they have intensified price competition in a weak consumption backdrop. Across Asia and Europe, sentiment is increasingly shaped by inventory positioning rather than production economics.

Consensus across market participants suggests that short-term recovery potential remains limited unless downstream sectors particularly DOP-related applications show sustained restocking demand.

If crude oil remains weak through Q3 2026, will producers be forced into sustained low-rate operations, risking long-term margin compression across DOP and DEG chains? For more updates stay tuned with Price Watch™.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.