Markets often spend weeks building support and only days losing it. The China Polycarbonate market offered a textbook example during May and June 2026 as a supply-driven recovery collided with a seasonal slowdown in demand, reshaping the Polycarbonate price trend in China.

Polycarbonate Prices in China Reverse Sharply

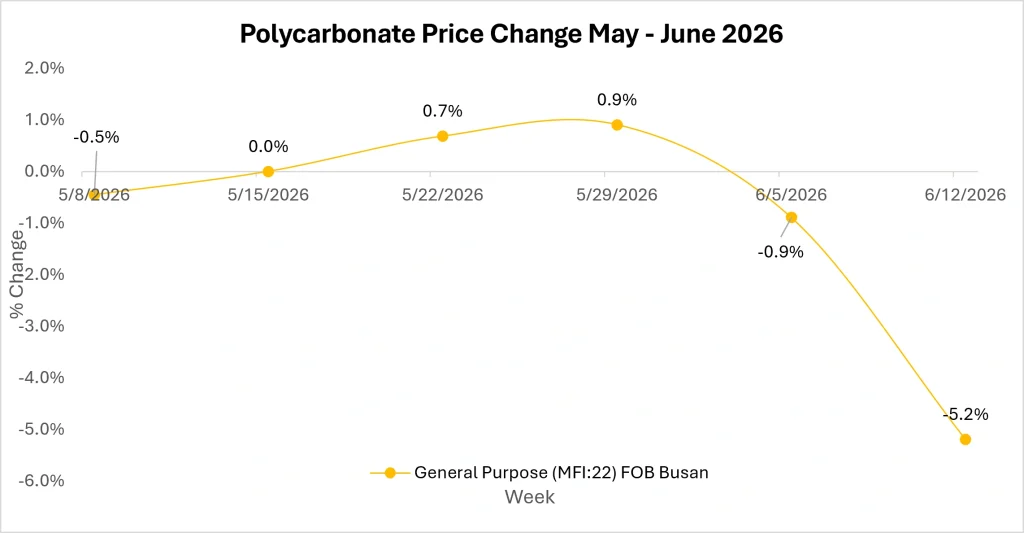

In May 2026, Polycarbonate prices in China managed to hold relatively steady despite sluggish trading activity. Production losses widened as maintenance shutdowns at major facilities reduced industry operating rates to their lowest level of the year.

With weekly output falling below key thresholds, suppliers faced little pressure to clear inventories and maintained firm pricing strategies. The market appeared balanced, even as downstream buyers remained cautious.

Source: Price Watch™ Polycarbonate Prices

As June began, several polymerization plants resumed operations. Keenchuang restarted production while Luxi Chemical increased operating rates across multiple lines, pushing industry utilization above 65 percent. Additional restart plans further improved material availability, narrowing earlier production losses and gradually rebuilding supply across the domestic market.

At the same time, Bisphenol A values slipped toward cyclical lows, removing an important layer of cost support that had previously helped stabilize Polycarbonate pricing.

The result was a sharp shift in market direction. The Polycarbonate price trend in China moved from consolidation to decline as suppliers became increasingly willing to negotiate while buyers continued purchasing only for immediate requirements.

How China’s Polycarbonate Supply Chain Is Responding

The pressure is now spreading through the value chain.

- Traders are adjusting offers more aggressively as low-priced inventories continue competing for market share.

- Downstream manufacturers of sheets, electronic casings, and consumer products are delaying replenishment purchases, expecting improved buying opportunities ahead.

Two developments stand out.

Operating rates are rising at a time when seasonal demand is weakening.

Cost support from Bisphenol A has weakened just as additional supply is entering the market.

China’s Polycarbonate Market Faces a New Supply Demand Equation

Over the next one to three months, the key question for China’s Polycarbonate market is whether demand can absorb the wave of material returning to the market. Operating rates have begun recovering following recent plant restarts, while expectations for additional supply continue to build.

At the same time, downstream buyers remain cautious, limiting purchases to immediate requirements rather than rebuilding inventories.

While Bisphenol A prices appear to have stabilized after recent declines, cost support remains relatively weak. This leaves market direction increasingly dependent on the balance between rising availability and actual consumption.

If supply continues to improve faster than demand recovers, competitive pressure across the market could intensify.

Here is a question worth considering; if buyers remain reluctant to build inventories despite lower Polycarbonate prices, what catalyst will be strong enough to restore market balance?

Stay connected with Price Watch™ for continued insights and weekly updates on Polycarbonate prices in China and the evolving Polycarbonate price trend in China.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.