The global polyurethane (PU) industry entered Q2 2026 under mounting pressure as rising feedstock costs, geopolitical instability, and severe logistics disruption reshaped market dynamics across major regions.

While January and February initially reflected relatively stable conditions with signs of moderate volume recovery, market sentiment shifted dramatically by March, April, and May following the escalation of tensions in the Middle East.

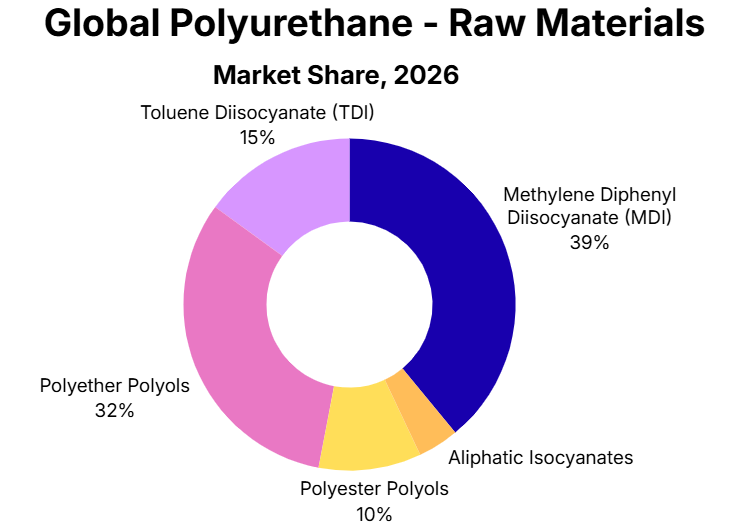

The resulting surge in crude oil prices, rising freight charges, and disruptions around critical maritime trade routes such as the Strait of Hormuz sharply increased production costs for key PU raw materials including MDI (Methylene Diphenyl Diisocyanate), TDI (Toluene Diisocyanate), and polyols.

Major global producers such as Covestro, Wanhua Chemical, Huntsman Corporation, and BASF responded with aggressive price hikes across multiple polyurethane grades in an effort to offset soaring upstream costs and tightening availability.

Middle East: Supply Critically Constrained

In Saudi Arabia and the broader Middle East region, the polyurethane market remains exceptionally tight amid ongoing geopolitical tensions and severe logistics disruptions.

Brief optimism emerged on April 17 when the Strait of Hormuz was temporarily declared open, raising expectations for improved material movement and supply recovery. However, renewed vessel incidents and escalating regional tensions quickly reversed the situation within 24 hours, once again disrupting normal shipping activity and undermining confidence in regional logistics networks.

Supply availability for key polyurethane feedstocks including MDI, TDI, and polyols remains critically constrained, particularly following operational disruptions at major regional production facilities with no confirmed restart timeline.

As a result, polyurethane market players in the Middle East are struggling to maintain stable production, secure raw materials, and manage heightened procurement risks.

China: Value Chain Disrupted Across Key End-Use Sectors

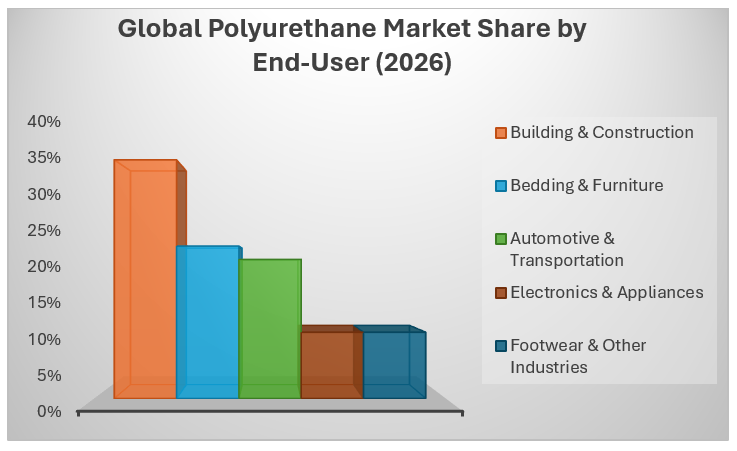

In China, the sharp rise in MDI and TDI prices has significantly disrupted the polyurethane value chain, particularly across the construction, furniture, appliance, and automotive sectors.

MDI, which is heavily used in rigid and semi-rigid polyurethane foams for insulation panels, refrigerators, and freezers, witnessed stronger cost pressure due to elevated feedstock and energy prices.

Meanwhile, TDI prices surged sharply, severely impacting the flexible foam industry where the material is widely used in mattresses, sofa cushions, and automotive seating applications.

The polyurethane industry has struggled to absorb the rapid increase in raw material costs, forcing enterprises to reduce operating rates or temporarily cut production.

Although the beginning of May 2026 brought a slight correction in TDI and MDI prices, market confidence remains fragile as uncertainty surrounding energy prices, export demand, and supply stability continues to dominate the outlook for China’s polyurethane industry.

Europe: Squeezed Between Cost Inflation and Weak Demand

In Europe, the polyurethane sector has also come under substantial pressure from rising feedstock and energy costs linked to the Middle East conflict.

TDI feedstock toluene prices have continued to climb in response to strengthening Eurobob gasoline and crude oil markets, both of which have remained highly volatile since the escalation of geopolitical tensions.

Increasing energy prices have amplified production costs for isocyanates, further squeezing already weak downstream demand conditions across Europe.

Buyers in key consuming sectors such as furniture, bedding, insulation, coatings, and automotive interiors have adopted cautious purchasing strategies amid broader economic uncertainty.

Meanwhile, intensive maintenance shutdowns at several major TDI facilities have tightened regional supply further, while high energy costs continue to threaten the long-term competitiveness of multiple European chemical plants.

As Q2 2026 begins, the European polyurethane market remains trapped between persistent cost elevation from the key raw material market, logistical instability, and fragile downstream consumption, leaving the industry highly vulnerable to further geopolitical developments.

Outlook: Stabilization Hinges on Geopolitical Resolution

If the geopolitical situation stabilizes and crude oil prices decline, the cost pressure on the global polyurethane (PU) market is expected to ease.

Major producers, including Covestro, Wanhua Chemical, Huntsman Corporation, and BASF, may respond by lowering prices for key raw materials such as TDI, MDI, and polyols.

Reduced feedstock costs would help alleviate some of the financial strain on downstream industries, including flexible and rigid foam, furniture, coatings, adhesives, and automotive sectors, potentially restoring margin stability and improving market confidence across the PU value chain.

In today’s polyurethane market, feedstock volatility, freight disruptions, and geopolitical uncertainty can reshape pricing dynamics within days. At Price Watch™, we deliver real-time polyurethane pricing intelligence, feedstock tracking, freight monitoring, and supply chain analysis across global markets.

From MDI and TDI movements to Chinese operating rates and regional trade flows, our platform helps procurement teams and manufacturers react faster and manage market exposure more effectively.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.