The Illusion of Equilibrium

For decades, the global energy market operated like a finely tuned machine. Supertankers crossed the oceans with predictable regularity, balancing supply and demand across the globe. Underneath the ground, advanced drilling technology unlocked vast new reserves of petroleum, pushing global production potential to historic highs. The world was awash in oil, and energy security was largely taken for granted.

To the casual observer, this smooth flow of global trade seemed permanent. Energy was treated as a flexible commodity that could easily be routed to any corner of the map to fix local shortages. However, this stability was an illusion.

The entire system relied on two fragile conditions: global political trust and completely safe, open ocean shipping lanes. Beneath the surface, the foundation was cracking, setting the stage for a strange paradox: a world that has more than enough oil, but is suddenly panicking over a lack of it.

The Cracks in the Core

The systemic cracks began spreading simultaneously across every continent, transforming a well-supplied world into a deeply fragmented landscape.

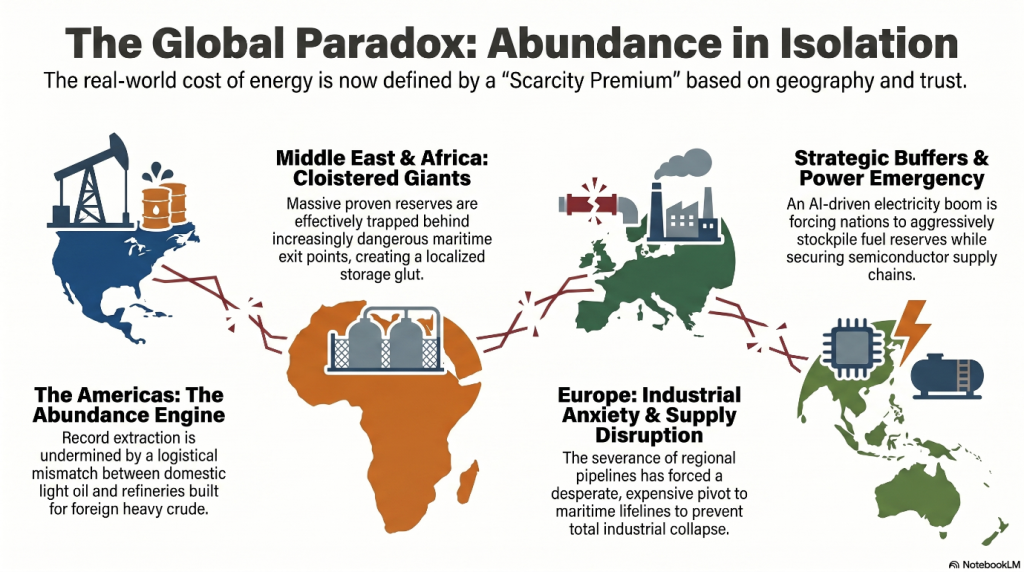

- North America’s Refinery Disconnect: In the United States, a deep mismatch began to complicate the supply chain. The shale revolution was churning out record volumes of “light, sweet” crude oil-which is thin and easy to refine. However, the multi-billion-dollar refineries along the US Gulf Coast were engineered decades ago to process “heavy, sour” crude traditionally sourced from the Middle East. Because of this structural mismatch, American refineries cannot easily absorb domestic oil. The US is caught in an inefficient logistical loop: it must export its excess light oil while continuing to import heavy crude from foreign producers to keep its factories running. When global shipping lanes face friction, this mismatch leaves even the world’s biggest producer exposed to price shocks.

- South America’s Scramble to Fill the Void: Seeing the traditional giants stumble, South America rapidly stepped up as the world’s new marginal supplier. Brazil’s deepwater fields pumped record volumes, and Guyana expanded its offshore developments at an unprecedented pace. Concurrently, the global crunch for heavy crude placed Venezuela-holder of the world’s largest reserves-back into the absolute center of commercial attention. Superpowers frantically began working to clear legal and sanctions barriers to get Venezuelan heavy molecules moving, turning South America into a critical, un-bottlenecked economic corridor.

- Europe’s Industrial Anxiety: Across the Atlantic, Europe entered a state of acute crisis. Forced to abruptly cut off nearby pipeline oil from the East, European buyers fell into a state of chronic anxiety. Refiners were forced into expensive, highly inefficient bidding wars for alternative crude from West Africa and the US Gulf Coast. Germany, the industrial heart of Europe, had to execute a total pivot, anchoring its economic survival to a transatlantic lifeline of expensive American Liquefied Natural Gas (LNG) and light crude just to prevent widespread factory shutdowns and structural decline.

- The Middle East and Africa (MEA) Bottleneck: In the MEA region-the traditional heart of global oil-the crisis manifested as a strange logistical trap. While the region sits on more than half of the world’s proven reserves, its primary maritime exit points became highly dangerous. Millions of barrels of daily output capacity were effectively locked away inside the region. This created a jarring local reality: storage tanks inside the Middle East were overflowing with oil that could not leave, while the rest of the world was starved for those exact barrels.

- The Asia-Pacific (APAC) Power Emergency: In the APAC region, the largest net-importing zone on earth, the shortage of oil was met by a secondary emergency: the exponential boom of Artificial Intelligence, which triggered a massive, sudden demand for electricity to power data centers. Net-importing economies faced a double crisis: they needed fuel to protect their growing economies from inflation, and advanced technology to secure their digital future.

This triggered a wave of rapid, high-stakes diplomacy. India launched a series of strategic manoeuvres to insulate its economy. First, flying to Abu Dhabi, New Delhi locked down a major agreement where the UAE’s ADNOC will store up to 30 million barrels of crude oil directly within India’s underground Strategic Petroleum Reserves. This buffer protected India’s domestic economy from Middle Eastern maritime disruptions.

Immediately after, India pivoted to the Netherlands to sign a 5-year Strategic Partnership Roadmap focusing on semiconductor supply chains and micro-lithography. This highlighted a new reality: a modern nation can no longer protect its economy just by buying fuel; it must simultaneously secure the technology and computing brains of tomorrow.

The Battle of Beijing

These regional tensions collided on the global stage when US President Donald Trump arrived in Beijing. Backdropped by a fierce tariff dispute and a massive trade deficit, Washington’s true, urgent motive was to break up a powerful non-Western alliance.

Trump arrived with a blunt demand for President Xi Jinping: China must immediately stop buying oil from Iran. For years, Iran had bypassed US sanctions by selling heavily discounted crude to China. In exchange, Beijing supplied Iran with advanced telecommunications, industrial machinery, and artificial intelligence infrastructure.

Washington wanted to use economic leverage to sever this technology-for-oil relationship, choke off Iran’s revenues, and reassert Western control over global energy trade.

The tension peaked as Beijing refused to back down. China fiercely guarded its strategic partnerships, offering only minor trade concessions while keeping its alternative economic network intact.

The ultimate proof of this broken global system came less than twenty-four hours after the American delegation left. In a calculated countermove, Russian President Vladimir Putin arrived in Beijing. The two leaders met to finalize long-term, guaranteed Russian oil and gas sales to China via secure, overland Siberian pipelines.

Because these land-based routes bypass the highly vulnerable ocean chokepoints, they created an energy corridor that Western sanctions and naval power cannot touch.

This was the exact moment the old, unified global trade system fractured. The mask of a single global market was ripped away, revealing a world divided between two competing economic blocs.

Falling Action: The New Energy Islands

The fallout from the Beijing showdown immediately forced a costly realignment across these newly formed energy islands. For Europe, the absolute break from Eastern pipelines meant that the era of cheap manufacturing was over, anchoring their entire industrial survival to a high-priced Western maritime lifeline.

Inevitably, this localized panic completely eroded decades of financial compliance. Historically, nations were deeply hesitant to cross Washington’s financial red lines due to their systemic dependency on the US dollar. But with raw economic survival on the line, the rush to find structural alternatives accelerated rapidly.

When the United States attempted to penalize or warn countries like India for absorbing discounted Russian oil, or threaten China for its Iranian technology trade, the warnings failed to work. Emerging economies were no longer willing to risk their own domestic stability to fight a Western economic war. They quickly turned to independent payment networks, local currency swaps, and sovereign clearinghouses to bypass the traditional Western financial gates entirely.

Denouement: The Global Game of Musical Chairs

Today, the global energy landscape has officially turned into a high-stakes, fast-paced game of musical chairs. The traditional rules of globalization have dissolved.

Instead, every major country is frantically flying its leaders around the world to lock down physical energy reserves and bleeding-edge technology before their competitors grab the last remaining seats.

The data confirms a profound structural truth: the modern energy crisis is entirely artificial. It is born from a deficit of political trust rather than a deficit of natural resources under the ground.

Because of this structural friction, the financial ledger has permanently changed. The real-world cost of a single barrel of crude oil is no longer dictated by simple production economics, but has split into two independent valuation layers:

Total Barrel Cost = Baseline Cost of the Molecule (Abundance) + Structural Premium for Geography & Trust (Scarcity)

The era of cheap, flawlessly optimized “just-in-time” global logistics is dead. In this newly polarized landscape, energy security is no longer defined by how much oil a nation has beneath its soil, but by its agility in navigating a treacherous global map.

As the final notes of the old, globalized economy fade away, the music is stopping-and the nations that fail to secure their physical corridors and independent technology pipelines risk being left standing alone in the cold.

| Region | Core Situation / Strategic Asset | Key Vulnerability / Risk | Strategic Manoeuvre / Outcome |

| North America | Churning out record volumes of “light, sweet” crude oil thanks to the shale revolution. | A structural mismatch: US Gulf Coast refineries were engineered for foreign “heavy, sour” crude, meaning they cannot easily absorb domestic oil. | Forced into an inefficient loop of exporting excess light oil while importing heavy crude, leaving the US exposed to global shipping shocks. |

| South America | Holding massive offshore developments in Guyana, record deepwater fields in Brazil, and the world’s largest heavy crude reserves in Venezuela. | Venezuela’s massive reserves have historically been trapped by legal and sanctions barriers. | Superpowers are frantically clearing barriers to get heavy molecules moving, turning the continent into the new marginal supplier. |

| Europe | Home to massive industrial manufacturing hubs, anchored by Germany. | The abrupt and total loss of nearby Eastern pipeline baseload. | Executing a total pivot to secure an expensive transatlantic lifeline of American LNG and light crude just to prevent factory shutdowns. |

| Middle East & Africa | Sitting on more than half of the world’s proven oil reserves. | Primary maritime exit points have become highly dangerous, effectively locking millions of barrels inside the region. | Local storage tanks are overflowing with trapped oil, while the rest of the world is starved for those exact barrels. |

| Asia-Pacific (India) | Expanding economy facing a double crisis: needing fuel to fight inflation and technology to power the AI boom. | Heavy reliance on the Middle East exposes the domestic economy to maritime disruptions. | Locking down 30 million barrels from the UAE in underground Strategic Petroleum Reserves and signing a semiconductor roadmap with the Netherlands. |

| Asia-Pacific (China) | Engaged in a powerful technology-for-oil relationship with Iran. | Facing aggressive US demands and tariffs aimed at severing its alternative economic networks and cutting Iran’s revenues. | Refusing to back down and finalizing secure, overland Siberian pipelines with Russia that completely bypass vulnerable ocean chokepoints. |

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.