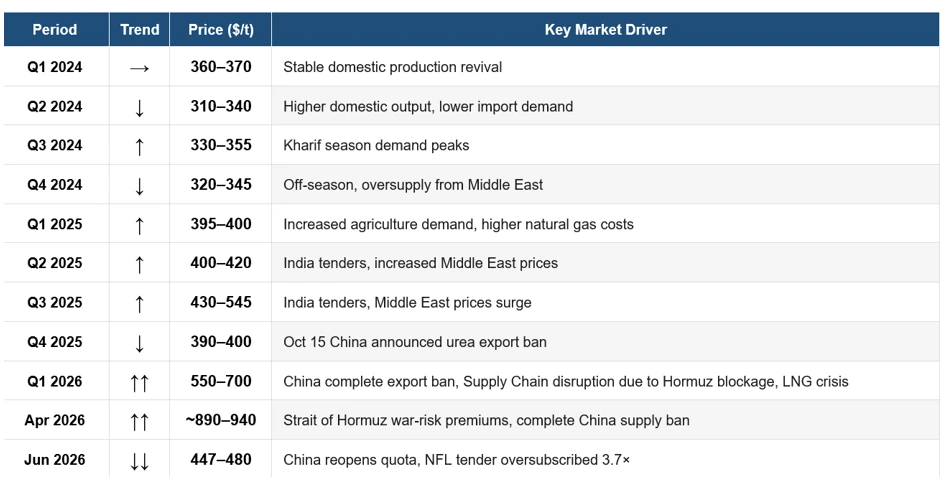

India’s NFL tender (Jun 8, 2026) revealed a ~50% price crash from the April 2026 peak, driven by China’s export quota resumption

India’s latest urea import tender, floated on June 8, 2026, by state-run National Fertilizers Limited (NFL), has sent shockwaves through the global fertilizer market. Bids came in at ~$445 per ton (CFR) a staggering fall of nearly ~50% compared to April 2026 prices of ~$890 per ton, when India was scrambling to secure supplies during the West Asia crisis.

China quietly reopened its urea export window after an 8-month near-total suspension. Beijing issued fresh export quotas to domestic producers for June-August 2026. This is the key driver behind the price decline.

India Urea Import Price Trend (2024–2026)

Source: Price-Watch™ Urea Prices

Why Did India’s Import Prices Crash?

Three Key Reasons for India Urea Price Crash in June 2026

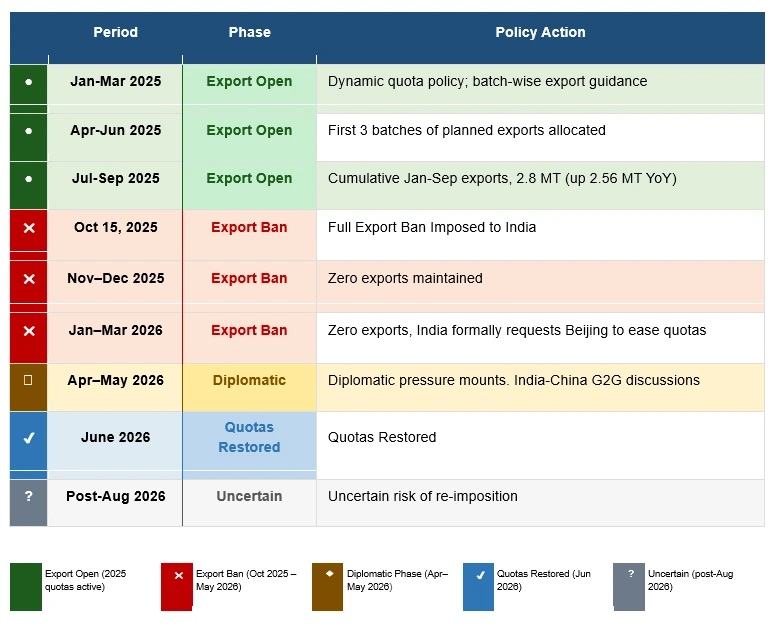

China’s Urea Export Strategy: The Swing Supplier

China occupies a structurally unique position in global urea markets. Its ~70% coal-based production capacity makes it largely insulated from global LNG price swings allowing China to produce cheaply even when natural gas-based producers in the Middle East, Europe, and South Asia are squeezed.

China’s Export Policy Timeline (2025–2026)

China uses export quotas to maintain domestic price restricting outflows when Chinese domestic prices fall below producer viability thresholds and opening them when domestic surplus builds. The current USD 670/t FOB price is ~2x China’s domestic price equivalent (~USD 300/t), ensuring producers capture a meaningful premium on each exported ton. If China re-imposes export restrictions after August 2026 (as it did in October 2025), the global market could lose 2-5 MT of supply, potentially may push India’s import prices back.

Key Implications for Global Urea Markets

| If China Keeps Exporting (Jun–Dec 2026) | If China Re-Bans Post-Aug 2026 |

|---|---|

|

|

The global urea market is entering a phase of structural transition. In the near term (Q3 2026), market conditions appear relatively balanced, supported by the resumption of Chinese export quotas, a heavily oversubscribed Indian tender at prices nearly 50% below the recent peak, and easing freight premiums in the Strait of Hormuz. These developments have also reduced pressure on India’s fertilizer subsidy burden, which had been at risk of rising significantly above the budgeted INR 1.68 lakh crore.

However, the market is still highly dependent on two key factors:

- China’s export policies, which can quickly change market conditions within a few weeks, as seen after the October 2025 export ban.

- Geopolitical tensions in West Asia, which influence both natural gas costs and shipping routes for a significant share of global urea trade.

From 2027 onward, the wave of new capacity from Russia, India, Qatar, and Central Asia may shift the balance decisively toward buyers.

For more such details visit Price-Watch™. Our platform delivers real-time data and expert analysis, offering deep insights into the key factors driving price fluctuations in the fertilizer (DAP, Ammonia, Sulphur, Ammonium Nitrate, SSP, Urea, TSP etc) market. By tracking critical events such as geopolitical tensions, supply chain disruptions, and economic shifts, Price-Watch™ keeps you fully informed of market dynamics. Track Price-Watch™ fertilizer price assessment on a weekly basis from 2015 onwards along with short term forecasts and get access to the detailed report in downloadable format.

Follow Price-Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.