The global Vinyl Chloride Monomer (VCM) market has shifted from a cost-driven rally to a correction phase as the factors that supported prices during March 2026 continue to fade.

Earlier in the year, escalating tensions between Iran, Israel, and the United States pushed crude oil prices higher, raising production costs across the petrochemical chain.

Simultaneously, Ethylene Dichloride (EDC) feedstock costs increased, logistics concerns intensified, and stronger PVC prices provided additional support to VCM markets.

However, with geopolitical tensions easing and peace negotiations reducing concerns over supply disruptions, the market has begun to reverse many of those gains. Falling crude oil prices, lower feedstock costs, and weakening downstream demand have collectively pressured VCM prices across major producing regions.

Vinyl Chloride Monomer Market in the United States

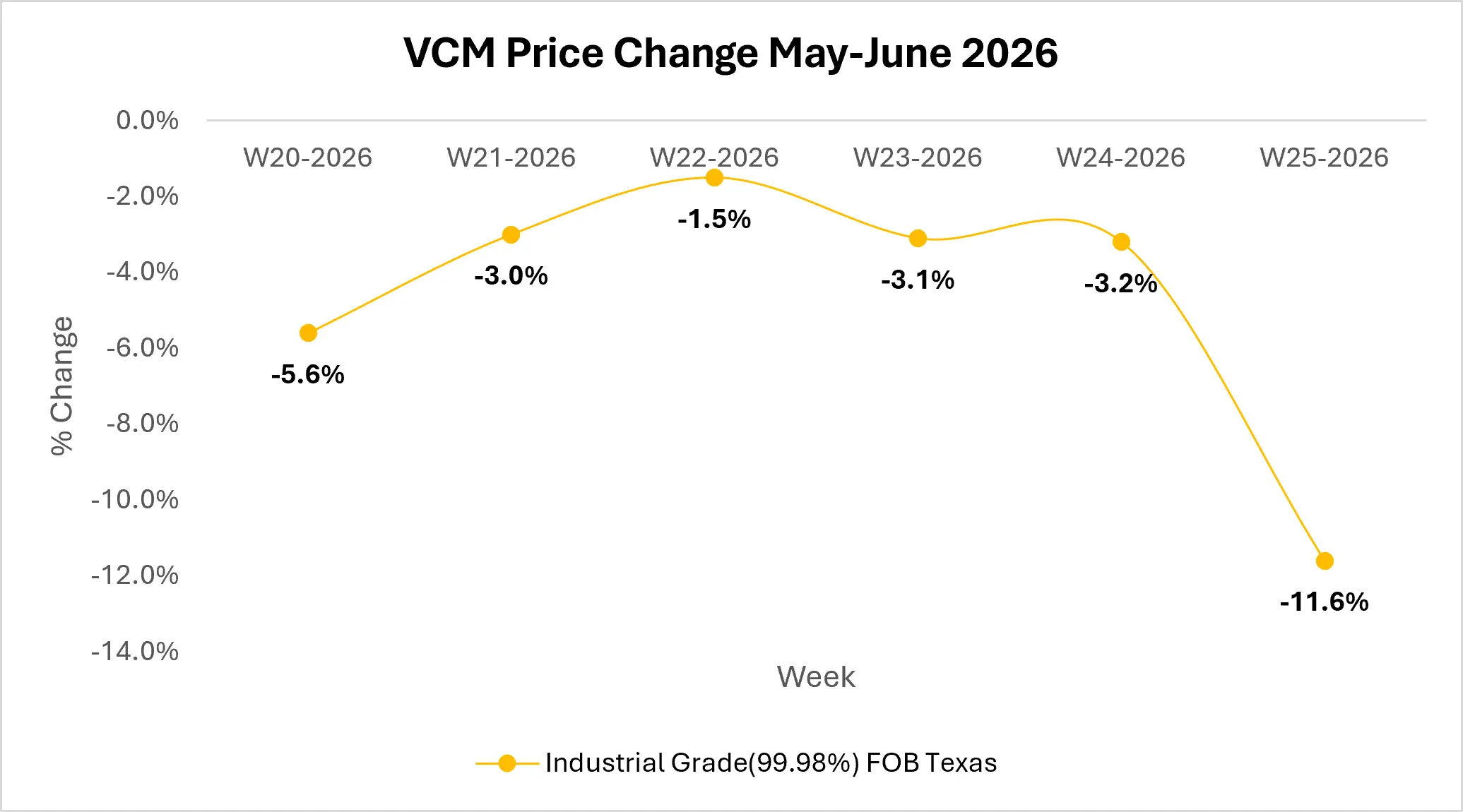

In the United States, VCM prices have declined as lower production costs coincided with weaker demand from the downstream PVC sector. During the March 2026 rally, U.S. producers benefited from rising PVC prices and elevated production economics, allowing them to maintain higher offer levels.

However, as crude oil and feedstock prices softened, that cost support gradually disappeared.

At the same time, U.S. PVC exporters faced increasing competition in international markets. Global buyers, particularly in Asia and Latin America, pushed for lower settlement levels as regional prices weakened.

This reduced the export premium that had previously supported U.S. PVC values, forcing producers to lower prices throughout the vinyl chain.

Consequently, VCM sellers faced growing pressure to reduce offers in order to maintain sales volumes and clear available supply.

Source: Price Watch™ VCM Prices

Vinyl Chloride Monomer Market in Europe

The European VCM market has followed a similar downward trajectory, although the key driver has been the rapid erosion of feedstock-based cost support. During March, higher crude oil prices and elevated ethylene values pushed production costs upward, supporting VCM prices despite relatively modest buying activity.

As energy markets stabilized and crude oil prices retreated, ethylene and EDC costs moved lower, reducing manufacturing expenses across the vinyl chain. The decline in feedstock costs weakened traditional pricing benchmarks and encouraged buyers to delay purchases in anticipation of further corrections.

Limited PVC demand and subdued spot trading activity amplified the downward pressure, with several low-priced transactions influencing broader market sentiment and accelerating the decline in VCM values.

One of the less visible developments in recent months has been the removal of the geopolitical risk premium that emerged during the height of the Middle East conflict.

In March, market participants were pricing VCM in the possibility of prolonged disruptions to energy supplies, feedstock availability, and logistics networks. These concerns encouraged precautionary buying and supported higher contract settlements throughout the VCM and PVC value chains.

Today, many of those concerns have eased. Shipping routes remain largely functional, feedstock availability has improved, and energy markets have become less volatile. As a result, buyers are no longer willing to pay premiums linked to potential disruptions, accelerating the market’s return to levels driven by underlying fundamentals.

The June VCM market has been characterized by falling production costs, easing geopolitical concerns, and weaker support from downstream PVC markets.

Across both the United States and Europe, the decline in crude oil and feedstock prices removed much of the cost pressure that had driven the March rally, resulting in a broad-based correction in VCM values.

Vinyl Chloride Monomer Market Outlook

Looking ahead, market participants will closely monitor whether crude oil and feedstock prices continue to soften or stabilize. The speed at which VCM prices approach pre-conflict levels will largely depend on the balance between production costs and the recovery potential of downstream PVC demand.

Could continued weakness in crude oil and EDC prices push VCM values back to pre-March levels by the third quarter of 2026? Or will any renewed disruption in Middle Eastern energy markets rebuild the geopolitical premium that temporarily reshaped global VCM pricing earlier this year?

Stay tuned with Price Watch™ for more updates.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.