Here is something worth paying attention to. While the broader chemical market was still reacting to the Hormuz shock in April 2026, Benzoic Acid FOB China prices barely moved.

They came off their March peak quietly, almost reluctantly, week by week. That kind of slow grinding lower is not weakness. It is a market where sellers are not panicking and buyers are not rushing either.

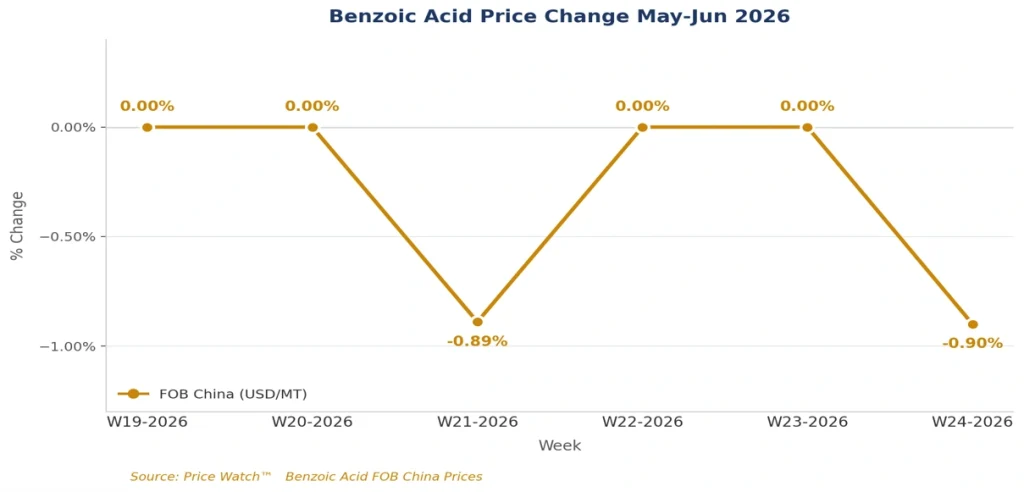

Benzoic Acid China Price Trend

China is the world’s dominant Benzoic Acid producer and exporter, supplying markets across Brazil, Vietnam, Indonesia, Mexico, Philippines, Turkey, and India.

The feedstock story here runs through toluene, which is produced from naphtha refining. When the Iran conflict pushed crude oil and naphtha higher in February and March 2026, toluene costs followed.

Chinese producers passed those costs through in March, lifting FOB offers. That is when prices peaked. Since then, as the ceasefire took hold and crude oil pulled back from its highs, toluene has decreased.

The cost pressure has eased, and FOB China values have followed, falling just under 0.90% in both W21 and W24 2026, with three flat weeks in between.

Source: Price Watch™ Benzoic Acid Prices

Key Development in the last 6 weeks in Benzoic Acid Prices

- FOB China Benzoic Acid prices fell approximately 1.8% from W19 to W24 2026, a slow and controlled descent driven by softer toluene feedstock costs and cautious downstream buying.

- CIF destinations in Latin America continue to carry a residual freight premium from the Hormuz disruption, keeping landed costs above year-ago levels despite the FOB softness.

Benzoic Value Chain Impact and Supply Chain Update

Two value-chain dynamics are shaping at this moment. First, with freight rates off their April peak but still above pre-war levels, the Hormuz risk premium has not fully exited CIF prices in Latin America and Southeast Asia. Shipping from China to Brazil still carries a residual surcharge.

Second, Chinese producers are running at high utilization rates; Shandong province, home to several large Benzoic Acid plants, has seen full operations resume after brief maintenance in early 2026. That supply pressure keeps exporters competitive on price.

The demand side is not adding any urgency. Food preservative buyers, who account for roughly 37% of global Benzoic Acid consumption, are in a seasonal lull between summer beverage production peaks.

Pharmaceutical and alkyd resin sectors are buying on need, not building inventory. Brazil and Mexico, two of the largest CIF destinations, have adequate local stock.

Vietnam and Philippines are booking selectively. India is an interesting outlier; its domestic market showed stronger demand through Q1 2026 on the back of food processing and pharma sector growth, and Ex-Kandla prices reflected that with a premium over CIF import parity.

Benzoic Acid Short-Term Outlook

The near-term direction for Benzoic Acid FOB China is mildly lower, with limited downside risk given toluene’s floor around current crude oil levels.

If Brent crude holds above 75 dollars per barrel and Chinese producer utilization remains high, prices are likely to drift in a narrow range through July 2026.

A meaningful demand recovery would need food and beverage sector restocking to kick in, which typically happens closer to Q3. Latin American markets may see slight CIF price relief if freight rates continue to ease toward pre-Hormuz levels.

If downstream buyers keep stretching procurement cycles, will Chinese exporters cut offers to move volume before Q3 demand arrives?

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.