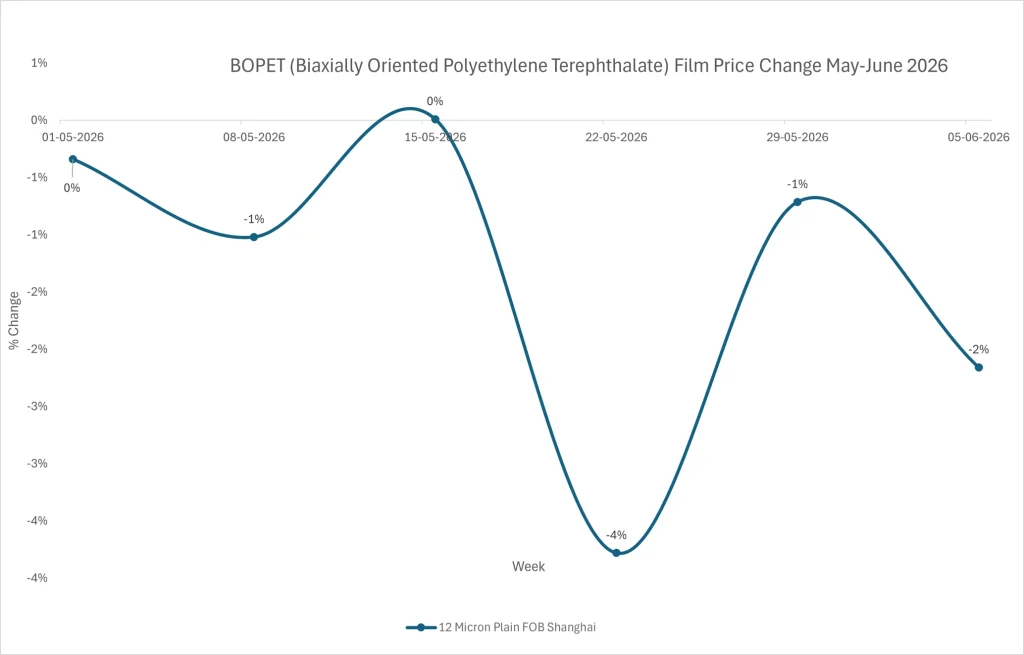

The global BOPET market is witnessing an unusual shift as falling crude oil prices are reducing production costs across the polyester value chain while simultaneously intensifying competition among suppliers.

Although lower raw material costs would typically support producer margins, abundant supply and aggressive export activity are causing manufacturers to pass cost savings directly to buyers through more competitive offers.

How lower crude oil prices are reducing BOPET production costs

Recent weakness in crude oil markets has softened prices of key polyester feedstocks, including naphtha, paraxylene (PX), purified terephthalic acid (PTA), and monoethylene glycol (MEG). These materials form the backbone of PET resin production, the primary raw material used in BOPET film manufacturing.

According to Price Watch™ analysis, declining PTA and MEG costs have improved production economics for BOPET manufacturers across Asia, allowing producers to lower replacement costs and maintain healthy operating rates. As feedstock affordability improves, suppliers are increasingly focusing on securing market share rather than defending margins.

Why global BOPET suppliers are facing stronger competitive pressure

The reduction in polyester feedstock costs comes at a time when regional BOPET availability remains sufficient across major production hubs in China, India, Thailand, and other Asian markets. With raw material supply remaining comfortable and production continuity largely unaffected, manufacturers are actively competing for export orders.

According to Price Watch™ intelligence, suppliers are adjusting offers to reflect lower production costs, creating additional pricing pressure in key importing markets. Buyers are also adopting a cautious purchasing approach, expecting further feedstock-driven softness in the coming weeks.

What lower feedstock costs mean for the BOPET value chain

Falling crude oil and polyester feedstock prices are influencing the entire BOPET value chain.

- Lower PTA and MEG costs are reducing PET resin and BOPET manufacturing expenses.

- Competitive export offers are increasing pricing pressure for packaging converters and regional film suppliers.

Food packaging, labeling, industrial laminates, and consumer goods sectors continue to provide stable demand support. However, supply growth remains stronger than consumption growth across several regions, limiting the market’s ability to absorb additional material availability.

Source: Price Watch™ BOPET (Biaxially Oriented Polyethylene Terephthalate)

BOPET Market Outlook

The global BOPET market is expected to remain highly sensitive to developments in crude oil, PTA, and MEG markets over the coming months. If energy prices continue to soften and feedstock availability remains comfortable, suppliers may continue offering competitive export prices to maintain operating rates and secure downstream demand.

According to Price Watch™ analysis, market participants should closely monitor feedstock movements, operating rates, and export activity as these factors are likely to determine the next direction of BOPET pricing. The key question remains: will improving demand be sufficient to offset growing competitive pressure from lower-cost production and abundant supply?

To track exact price direction, regional spot prices, and procurement activity, subscribe to Price Watch™ today.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.