Asia’s carbon black market is entering the second half of 2026 on softer footing. After a turbulent first quarter in which the Strait of Hormuz crisis sent feedstock costs soaring, the sentiment across the region has flipped, crude oil is sliding back toward pre-conflict levels, Chinese and Indian suppliers are sitting on ample capacity, and buyers are once again in the driver’s seat.

The result is a carbon black landscape defined less by scarcity and more by a cautious, oversupplied calm.

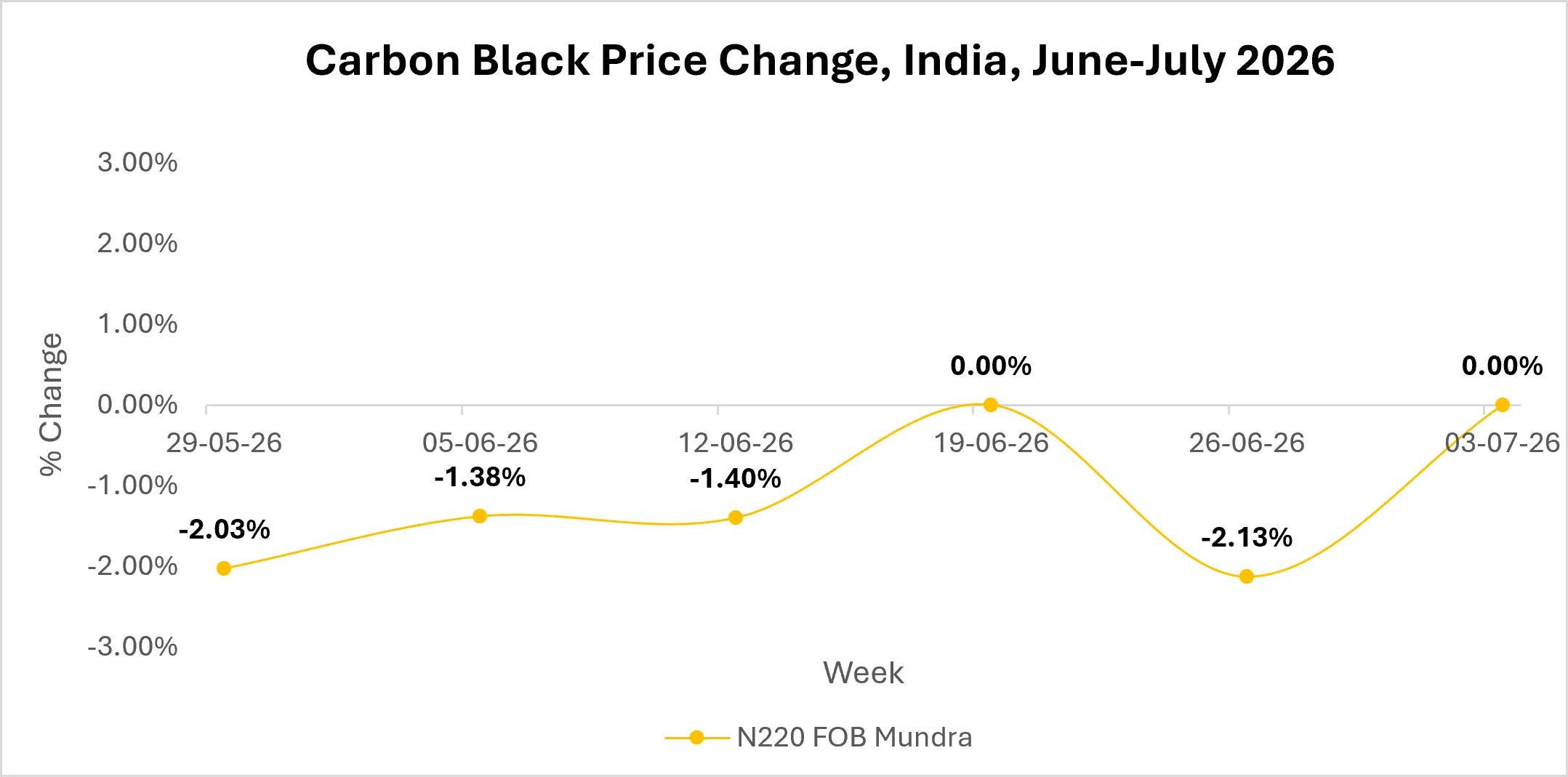

Carbon Black Feedstock Costs Ease as Crude Oil Retreats

The story of 2026 so far has been a wild one for oil, and carbon black has felt every twist. When Iran shut the Strait of Hormuz in early March following the outbreak of hostilities with Israel and the United States.

Since roughly a fifth of the world’s crude and LNG passes through that single chokepoint, the shock rippled straight into carbon black feedstocks such as coal tar oil and carbon black feedstock oil (CBFS), pushing Chinese and Indian carbon black prices up by double digits during the first quarter alone.

That picture has since changed. Following months of on-again, off-again ceasefires, USA and Iran signed a memorandum of understanding on 17 June aimed at ending the war and lifting the naval blockade on the strait, and by early July, tanker traffic and crude exports from Saudi Arabia and the UAE had climbed back to roughly 90 percent of pre-war levels.

Brent has since drifted down to around $70 a barrel, its lowest level since before the conflict began, even as negotiators continue fine-tuning the final terms in Doha. For Asian carbon black producers, that easing in upstream costs is beginning to remove one of the biggest cost pressures of the year, even if the geopolitical situation remains, as many analysts note, still tentative.

Source: Price Watch™ Carbon Black

Carbon Black Market Outlook

Northeast Asian prices had already fallen more than 10 percent between the first quarters of 2025 and 2026, while Indian prices slid nearly as much, even before the Hormuz crisis flared up.

The reason is structural: China’s carbon black capacity, led by producers such as Jiangxi Black Cat, Longxing Chemical, and Jiangsu Liyang Liancheng, has kept regional supply abundant, while softer domestic tire demand has pushed more Chinese material into export markets.

That steady stream of competitively priced Asian-origin material continues to outpace the region’s own consumption, keeping a lid on prices even as feedstock costs occasionally spike.

With crude now retreating and the Strait of Hormuz gradually reopening to normal traffic, the near-term outlook across Asia leans cautiously bearish to flat. Buyers appear content to sit on the sidelines and let Chinese and Indian supply absorb any strengthening in demand.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.