India used to be one of the world’s biggest sugar suppliers. For at least the next three seasons, that role looks largely gone.

India’s Ethanol Policy Continues to Reshape Sugar Availability

El Nino driven weak monsoon rains have already cut cane planting and trimmed output forecasts. In some estimates, production is now running below domestic consumption needs. That gap alone would be enough to keep exports off the table. But the more structural shift is happening inside India’s own policy framework.

India’s ethanol blending programme is pulling more sugarcane away from sugar mills and toward biofuel production. Distilleries are filling contracts the government actively supports, and that diversion is not a short-term adjustment. It is a deliberate reallocation getting larger every season. Acreage is also shifting toward less water intensive crops, which only tightens the cane base further.

US Ethanol Market Gains Support from Seasonal Demand

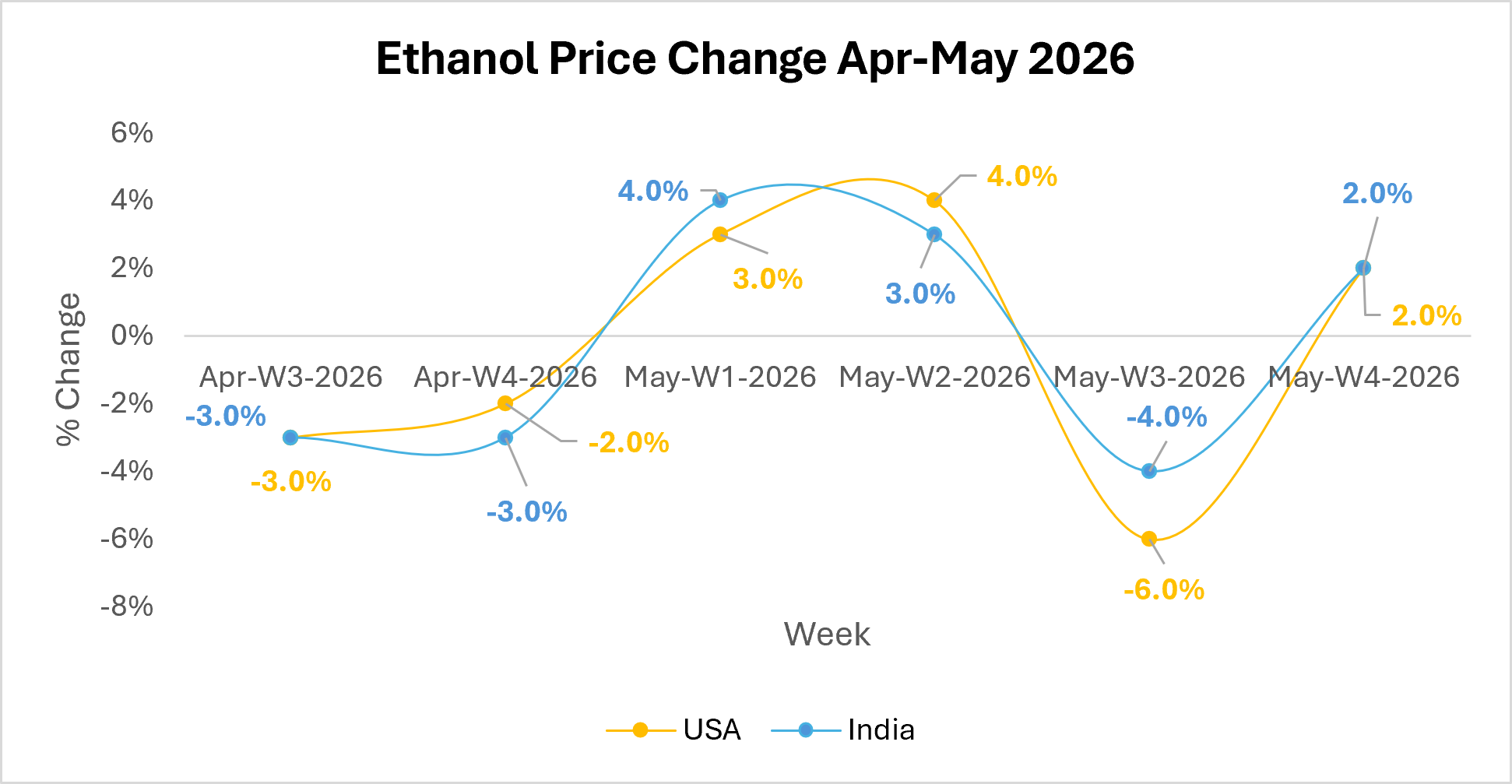

This is where the story shifts. US ethanol pricing was soft for most of the first half of the year, held down by strong domestic production and weak early season blending demand. That softness is now turning.

Summer driving activity is building, blending volumes are picking up week on week, and a proposed farm bill amendment could lift the summer blend cap from 10 to 15 percent, pulling more ethanol into the fuel supply on a structural basis. Prices have already started responding, moving off recent lows as demand catches up.

Source: Price Watch™ Ethanol Prices

Global Ethanol Trade Dynamics Continue to Evolve

- Whether the US blend cap amendment passes, since that alone could tighten domestic supply and sustain the price recovery

- Indian monsoon delivery over the next six weeks, since any shortfall keeps sugar tight and pushes more cane toward ethanol

Ethanol Market Outlook

Over the next three months, US ethanol prices look more likely to keep rising than to slip back, supported by seasonal demand and potential policy tailwinds. India stays absent from sugar export markets unless monsoon rains surprise to the upside.

So here is the real question. If the US blend cap rises while India stays out of sugar markets for multiple seasons, does that put a floor under global ethanol values the market hasn’t priced in yet? For pricing trends, keep an eye on Price Watch.

Follow Price Watch™ on LinkedIn for real-time raw material insights, pricing trends, supply chain intelligence, and market updates shaping global commodity markets.